CENTERED With H.E.R.O. Issue 2: Resilient Amidst Trade War – Japan’s AS ONE AI X RPA, Exponential Innovators Highly Impervious to Trade War Risks | 27 May

May 25, 2019 Leave a comment

0% in OEM/ODM + 0% in component makers + 0% in semiconductor & related sector + 0% in capital equipment, tech hardware & big-ticket items + 100% singular focus in a portfolio of highly-profitable listed Asia SMID-cap tech-focused exponential innovators = Higher probability of resiliency in both fundamentals and investment returns that are highly impervious to the US-China trade war risk and market volatility which have escalated since 6 May 2019.

For instance, AS ONE (TSE: 7476), Japan’s #1 specialist B2B platform business model that carved out a profitable niche selling through catalogs and its ecommerce (EC) site AXEL a vast array of over 3 million items of laboratory & healthcare instruments and consumables & disposables, is up 7.6% since 6 May 2019 to a market value of over US$1.69 billion, extending its YTD gains to 23%. AS ONE had announced on 13 May 2019 a strong set of FY03/2019 results with earnings at a record high and 10 consecutive years of sales increase.

Contributing to EC sales were increased customers of the EC single-source purchasing system (158 companies compared with 135 at end–FY03/2018), where products and services are sold through an electronic catalog directly incorporated into the customer’s purchasing system, and increased sales to online retailers, such as MonotaRO, Misumi, Askul and Amazon, whose end users are small companies. Its new state-of-the-art automated Kanto Distribution Center (DC), more than twice as large as the current largest base, the Osaka DC, will start operation in May 2020, a strategic expansion that will lead to the achievement of their goal of 100bn yen in sales from the current 66.7bn yen.

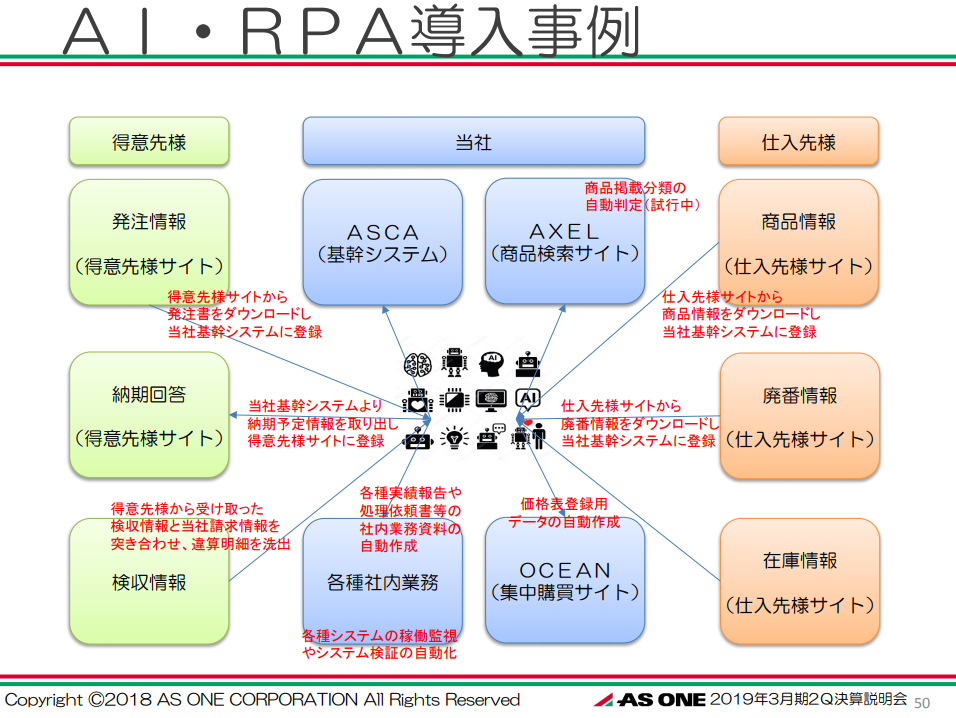

AS ONE has also adopted artificial intelligence X robotic process automation (AI x RPA) to increase its efficiency and margins as it scales up. Medical institutions, hospitals and researchers “have various specialized needs, such as they want a tool and equipment that can make the experiment in a vacuum state or under zero gravity. Our strength is to deliver these products seamlessly and speedily”, commented CEO Takuji Iuchi, the third-generation business leader. Because the product is low volume-high-mix in nature, or small in quantity and many types, customer interface, inventory & logistics management and business process integration are the critical backbone systems of the company. The intelligent automation of this backbone through AI X RPA has given AS ONE an exponential edge to improve the quality and speed in responsiveness to their customers.

Including AS ONE, the portfolio of 40 H.E.R.O. innovators, which has an average market cap of US$1.41bn (median market cap of US$810m), delivered strong interim results growth amidst the US-China trade tensions: overall weighted sales rose 30.5% YoY and operating profit grew faster with increasing returns to scale at 58.7% YoY, supporting the portfolio returns.

An overwhelming majority (82.5%) of the 40 HERO portfolio stocks are highly profitable “SaaS (software-as-a-service), information & data analytics/AI” companies and “platform business models”, a group which we believe is highly impervious to trade war risks. 10% are indispensable medtech innovators with high recurring-revenue high-profitability business models. EC, cybersecurity and IoT highly-profitable companies account for the remainder 7.5%.

The recurring and predictability nature of the revenue model in growing monthly or annual paying subscribers have made SaaS companies a bedrock of investment resilience in a volatile market environment with growing regulatory and trade-war risks rattling across industries. SaaS recurring-revenue business model with high profitability, positive free cashflow and low customer churn rate account for 55% of portfolio stocks.

And unlike many of the SaaS companies in the US or China or most of everywhere else that are still loss-making and cash-burning, a selected group of Japan’s listed under-the-radar exponential innovators have quietly built highly profitable business models generating positive free cashflow.

John Somorjai, EVP of Corporate Development and Salesforce Venture at CRM giant Salesforce.com (NYSE: CRM) commented on 4 Dec 2018 that having investing in over 280 SaaS companies in 18 countries since 2009, “Our highest returns to date have been from the U.S. and Japan markets.” Long overlooked by investors, Japan is still regarded by the superficial macro investors as the land of the aging dinosaur-like companies such as Toshiba with weak population demographics. Farsighted investors are now seeing strong growth of Japan’s tech industry as Japan’s public cloud services market, the fourth biggest in the world, is projected to more than double from the 2017 level to $13 billion in 2022, according to IDC forecasts.

We are grateful to have the investment interest and positive feedback about the quality of our research ideas by farsighted professional investors. These include the super investor in Singapore who’s the former managing director at one of the world’s largest sovereign wealth fund and the founder of a successful billion-dollar boutique hedge fund in Asia ex-Japan equities, who commented that most Asian funds invest in the typical “old-tech” companies who are component makers or OEM/Apple-suppliers exposed to unpredictable capex spending cycles, and that he likes that no other funds are like us in having a pure and singular focus on exponential innovators with recurring-revenue business models who are forging their own categories of growth to solve high-value problems for their customers.

One of our focused portfolio stocks, a Korean-listed SMID-cap tech innovator with dominant 80% domestic market leadership in recurring information & big data services, remains resiliently positive since 6 May 2019. Since we highlighted this Korean firm about three months ago to one of our advisory clients, a business owner/CIO of an established Asia ex-Japan value fund management company in Singapore who manages sovereign wealth and pension/endowment money, the stock is up over 40% to a market value of over US$750m. We are grateful to be able to deliver our recently operationalized bespoke investment solution for family offices, UNHW, corporates and long-term institutional investors with satisfactory results to this wise business owner/CIO client whom we like and respect and care for.

Farsighted investors are experiencing first-hand and benefitting from the flight-to-quality effect in the market to quality listed innovators that are most relevant in this exponential world, because each time the market corrects, the stronger hands of longer-term farsighted investors will accumulate more and more of these quality innovators, while the weaker short-term opportunistic hands sell out, creating a resiliency effect in these stocks. Listed profitable SMID-cap tech innovators with non-linear exponential growth potential are the most relevant and mispriced multi-year investment trend and opportunity.

Inspiration for CENTERED With H.E.R.O.: Our clients, just like our H.E.R.O. innovators and business owners, understood the profoundness that it’s not about a Maslow-type pyramid that they need to scale upwards in profits and returns; the H.E.R.O. journey is not upwards, but a deeper journey inwards and towards the center, about the kind of person you want to become through the work you build and invest in to serve those you care about.

CEO Takuji-san has a grander purpose to make AS ONE into “a company that employees can tell from your heart to your most important person, son, daughter, wife, husband, best friend that ‘It is such a nice company, there is no one else!’”

Deeper and inwards towards the center. As Einstein elucidates: “Strive not to be a success, but rather to be of value” – Amid all of life’s chaos and challenges, a restorative balm to all of us to be Centered in values with focus and purpose to be of value in serving an idea larger than ourselves and the people we care deeply for.

Thus far, of the 72 entrepreneurs and CEOs whom we had highlighted in our previous weekly research brief HeartWare, less than one-third are in our focused portfolio of 40 HERO Innovators, while the rest (50+) are in our broader watchlist of 200+ stocks.

If you are not moving forward in this exponential world, you are going backwards. If you want to join us at the leading edge of opportunity, if you identify yourself in the values and bigger sense of purpose in H.E.R.O., or you wish to tell from your heart to your most important person, son, daughter, wife, husband, or best friend that you are a farsighted and thoughtful explorer in the H.E.R.O.’s Journey participating in the long-term exponential growth of a selected group of outstanding entrepreneurs, standing up for the embracement of the human spirit, please contact us via email or WhatsApp at +65 9695 1860. Thank you very much for your patience and support and we look forward to growing exponentially with you as we explore the H.E.R.O.’s Journey together.

It started with rethinking a few questions. Question No. 1: Can the megacap tech elephants still dance? Or is this the better question: Is there an alternative and better way to capture long-term investment returns created by disruptive forces and innovation without chasing the highly popular megacap tech stocks, or falling for the “Next-Big-Thing” trap in overpaying for “growth”, or investing in the fads, me-too imitators, or even in seemingly cutting-edge technologies without the ability to monetize and generate recurring revenue with a sustainable and scalable business model? How can we distinguish between the true innovators and the swarming imitators?

Question No. 2: What if the “non-disruptive” group of reasonably decent quality companies with seemingly “cheap” valuations, a fertile hunting ground of value investors, all need to have their longer-term profitability and balance sheet asset value to be “reset” by deducting a substantial amount of deferred innovation-related expenses and investments every year, given that they are persistently behind the innovation cycle against the disruptors, just to stay “relevant” to survive and compete? Let’s say this invisible expense and deferred liability in the balance sheet that need to be charged amount to 20 to 30% of the revenue (or likely more), its inexactitude is hidden; its wildness lurks and lies in wait. Would you still think that they are still “cheap” in valuation?

Consider the déjà vu case of Kmart vs Walmart in 2000s and now Walmart vs Amazon. It is easy to forget that Kmart spent US$2 billion in 2000/01 in IT and uses the same supplier as Walmart – IBM. The tangible assets and investments are there in the balance sheet and valuations are “cheap”. Yet Kmart failed to replicate to compound value the way it did for Walmart. Now Walmart is investing billions to “catch up” and stay relevant. Key word is “relevancy” to garner valuation.

We now live in an exponential world, and as the Baupost chief and super value investor Seth Klarman warns, disruption is accelerating “exponentially” and value investing has evolved. The paradigm shift to avoid the cheap-gets-cheaper “value traps”, to keep staying curious & humble, and to keep learning & adapting, has never been more critical for value investors. We believe there is a structural break in data in the market’s multi-year appraisal (as opposed to “mean reversion” in valuation over a time period of 2-5 years) on the type of recurring-revenue profitable business models, the “exponential innovators”, that can survive, compete and thrive in this challenging exponential world we now live in. Tech-focused innovators with non-linear exponential growth potential are the most relevant multi-year investment trend and opportunity.

During our value investing journey in the Asian capital jungles over the decade plus, we have observed that many entrepreneurs were successful at the beginning in growing their companies to a certain size, then growth seems to suddenly stall or even reverse, and they become misguided or even corrupted along the way in what they want out of their business and life, which led to a deteriorating tailspin, defeating the buy-and-hold strategy and giving currency to the practice of trading-in-and-out of stocks. On the other hand, there exists an exclusive, under-the-radar, group of innovators who are exceptional market leaders in their respective fields with unique scalable business models run by high-integrity, honorable and far-sighted entrepreneurs with a higher purpose in solving high-value problems for their customers and society whom we call H.E.R.O. – “Honorable. Exponential. Resilient. Organization.”

The H.E.R.O. are governed by a greater purpose in their pursuit to contribute to the welfare of people and guided by an inner compass in choosing and focusing on what they are willing to struggle for and what pains they are willing to endure, in continuing to do their quiet inner innovation work, persevering day in and day out. There’s a tendency for us to think that to be a disruptive innovator or to do anything grand, you have to have a special gift, be someone called for. We think ultimately what really matters is the resolve — to want to do it, bring the future forward by throwing yourself into it, to give your life to that which you consider important. We aim to penetrate into the deeper order that whispers beneath the surface of tech innovations and to stand on the firmer ground of experience hard won through hearing and distilling the essence of the stories of our H.E.R.O. in overcoming their struggles and in understanding the origin of their quiet life of purpose, who opened their hearts to us that resilience and innovation is an art that can be learned, which can embolden all of us with more emotional courage and wisdom to go about our own value investing journey and daily life.

Warm regards,

KB | kb@heroinnovator.com | WhatsApp +65 9695 1860

www.heroinnovator.com