| Dear Friends,“A Community First, A Company Second”: Berkshire Hathaway’s Frugal Innovator DaVita and Are There Similar Wide-Moat Companies in Asia?CNBC’s Becky Quick: “Mark Blakely from Tulsa, Oklahoma, wrote in and said, ‘Would Ted Weschler explain what he likes about DaVita HealthCare Partners and why he finds this company such a great investment? Since Berkshire signed an agreement not to own more than 25% of DaVita, does Ted or Berkshire have any other intentions besides being a large shareholder?’”

Berkshire’s Ted Weschler: “Okay. I followed the dialysis industry for, mmmm 30 years now. Right outta college I started– studying. And so I know the space reasonably well. And I think the broad filters that I apply for healthcare investment in general is: Number one, ‘Does the healthcare company deliver better quality of care than somebody could get anywhere else?’ And DaVita falls into that. Number two, ‘Does it deliver a net savings to the healthcare system?’ In other words, is the total bill for U.S. healthcare cheaper because of the efficiency that the company provided? DaVita checks that box. And lastly, ‘Do you get a high return on capital, predictable growth– and, you know, shareholder-friendly management?’ Absolutely. And all three of those together– you know, you’ve got healthcare is whatever, 17%, 18% of GDP. You got an incredibly talented team running that company. I’m not sure what the stock will do over the next year or the next two years, but very comfortable at five years from now it’ll be a more valuable franchise.”

Does the healthcare company deliver better quality of care than somebody could get anywhere else?

Does it deliver a net savings to the healthcare system?

These are the two great questions asked by Ted Weschler, one of the two stock pickers Buffett hired as part of his succession plan, in assessing Berkshire Hathaway’s investment in Denver-based DaVita (NYSE: DVA, MV $17bn), the second largest operators of kidney dialysis centers with a network of 2,100 outpatient centers serving over 180,000 patients with around 34% market share in the United States, behind leader Fresenius (NYSE: FMS, MV$26.4bn). Berkshire Hathaway had accumulated 27.2m shares, or about 13% of DaVita in 4Q11, a stake increased to 38.5m shares worth $3.1bn, nearly doubling in value from its cost of investment while the S&P index was up around 50% during the same period.

These two questions are the hallmark characteristics of a frugal innovator, which encompasses the ability to do more with less, creating more business and social value because of the business model innovation in the way they operate, build and deliver sustainable solutions with cost-effectiveness, care, integrity and without putting strains on the broader societal system. Exploring further into the business model of Berkshire’s DaVita and frugal innovators will be useful for serious value investors to identify and assess sustainable wide-moat compounders in Asia.

Anyone who has seen a diabetes patient in a kidney dialysis center can immediately feel the morale and emotional commitment that is essential to the long-term health of the patient. Not only do they have to endure the pain of having two thick and long needles stuck in them as they sit hooked up to a machine, but also they had to come to the dialysis center for four hours or more three times a week. These scheduling left the patients feeling they have no control over their lives. Patients become depressed. Patients on dialysis often suffer other diseases such as cardiovascular disease. Patients missed their dialysis appointments because they found the treatment and its logistics unpleasant. And patients chose to end their treatment and therefore end their lives; about one out of five deaths of patients on dialysis was a deliberate decision by the patients.

What if dialysis patients are managed by a patient-centric “membership” plan that coordinates their total healthcare needs at a fixed fee – and the fee is potentially lowered over time as their overall health shows a consistent improvement? Thus, instead of paying for visits, procedures, and tests, patients pay for care per member. The nature of such contracts puts the provider “at-risk” for the costs required to care for each member, thereby creating an incentive to reduce costs through preventive care and improving overall health such that fewer and timely treatments are required. The mindset will be shifted to that of a frugal innovator to provide quality value-add solutions while sharing the benefits of the cost savings to get the best outcome for patients with the lowest consumption of high-cost, low-value inputs, such as unnecessary surgeries and treatment, duplicative tests, etc. For instance, the provider could arrange for the patient to use that four-hour time in dialysis chair on general needs, such as eye and foot exams. Physicians and care providers in the “at-risk” network are also rewarded with bonus based on clinical outcomes, patient satisfaction, and the performance of the larger group or region. This “at-risk” model is the alternative to the existing fee-for-service (FFS) which creates the distorted incentive to maximize the volume of services, as evident from the recent horrifying case of the Michigan cancer doctor who prescribed $35 million worth of unnecessary chemotherapy just so he could bill healthcare companies.

DaVita (NYSE: DVA) – Stock Price Performance 1995-2015 Vs S&P 500 Index

DaVita controls about $33,000 in Medicare spending for each dialysis patient, but those clients often are very sick with multiple illnesses and cost about $55,000 more each year in other health needs. Kent Thiry, chief executive of DaVita, says the company could manage the entire $88,000 healthcare needs per patient, saving the government money while improving quality at the same time. This coordinated managed care business model is a result of DaVita’s acquisition of HealthCare Partners (HCP), America’s largest operator of medical groups and physician networks with more than 150 medical clinic locations and more than 8,300 independent doctors, in May 2012 for $4.4 billion at the valuation of 8.4 times FY11 EBITDA.

HCP represents one of the few organizations that has actually demonstrated that ability for years via its strong primary care base, emphasis on prevention, integrated healthcare information technology infrastructure, chronic care management and care coordination efforts, performance measurement and reporting, and experience with taking “at-risk” patients. For instance, patient medical records are standardized and shared as part of a data-driven, team-based approach that coordinates the efforts of primary care physicians, specialists, hospitalists, nurses, care managers, and social workers. Patient data are analyzed to develop a best care plan for each patients; automatic intervention alerts help ensure patients take their medication and get proper preventive and follow-up care; home-care teams help keep patients stable in their home – all helping to avoid more costly ER (emergency room) visits and hospital admissions that also put further strains on the healthcare system. HCP’s integrated care management program for inpatient bed days per 1,000 among seniors was half the Medicaid fee-for-service average and the 30-day readmission rate was one-third lower – but with better quality measures. HCP is synergistic to DaVita’s existing VillageHealth which provides advanced care management services to government agencies with non-dialysis cost savings of 15% vs fee-for-service Medicare.

It was hard to imagine that when Kent Thiry took the helm in 1999 as CEO of Total Renal Care (TRC) with its 460 dialysis centers, the former name of DaVita, the company was near bankruptcy. It was losing more than $60m per year, was under investigation for fraud by the federal government, had a 40% staff turnover, exhibited poor clinical outcome measures relative to its peers, and had its bank covenants broken by this performance. Share price had plunged from $23 to $1.71 and was heading even lower. TRC was founded by Victor Chaltiel who tried to do financial engineering and M&A deals at the kidney dialysis centers based on his earlier success in flipping a former company for a good profit using such methods. Senior executives paid scant attention to the dialysis centers themselves, which were seen more as an avenue of corporate growth where patients and caregivers were economic units in a bigger financial structure. This headquarter-centric, financially-oriented operating culture did not win friends among the healthcare practitioners who worked hard in the field to deliver quality care.

Kent Thiry and his management team made a decision that was baffling at that time given that it was a crisis period: they emphasized the importance of the “softer issues” of values and principles, that the company should be a “A community first, a company second”: “Think of a small town where people have to pay taxes, this is OK if people feel they get value, a good police force, roads, parks. Similarly, there is no problem with shareholder profit in return for capital put into the business as long as the right things are done for the patients and teammates. But it must be fair and transparent.” The company was renamed DaVita, the name chosen by employees, meaning “giving life”. DaVita experienced a remarkable turnaround between 2000 and 2005, a transformation based on building a strong values-driven culture, with an emphasis on fact-based decision making (“no brag, just facts”) and the theme of “one for all, all for one” and an emphasis on company as community. From near-bankruptcy status, DaVita went on to become strong enough to acquire its Swiss rival Gambro, make its way onto Fortune’s World Most Admired Companies list, and market cap compounded from $200m to $17bn.

Kent Thiry, affectionately called KT many teammates in the company, reflected on the transformation:

“I realized that many corporations are lifeless, emotionally sterile, and culturally empty despite the fact that people spend a lot of their life in them. This was especially critical to address how decentralized our teammates are, how pressurized their work is helping patients with renal failure, and how easy it is to create a gap between management and the people at the front lines, and that was something I felt had to be addressed to have a sustainable strategy for DaVita. Equally important, it is just a better way to live. We call this the DaVita village, a place where we care for each other, sacrifice for each other, support each other, and together, create meaning in our work and in our lives, as we embarked on a quest to build the greatest dialysis company the world has ever seen.”

The organization was designed to be flatter and Kent Thiry began answering hundreds of emails from employees all over the company, compressing the distance from the CEO to the front line. A big part of the new philosophy was to recognize that the dialysis centers, where patient care was delivered and where most DaVita teammates worked, were key to the company’s success. To emphasize the importance of the centers, Thiry had all senior managers, himself included, “adopt” a center and drop by occasionally. The adopt-a-center program was adapted to “Reality 101” which entailed spending a week in a center helping to do the day-to-day work. Executives participated in activities such as machine set-up prior to dialysis, machine tear-down and disinfection post-treatment, helping with blood pressure monitoring, or whatever tasks they felt comfortable in performing. Thiry believed it was important not to push people to do things they felt uncomfortable or unskilled at doing, but it was important for people to experience what it was like to get up at 4 o’clock in the morning to get to the center at 5.am. so that it could be open for the first patients at 6 a.m. and to see what life in a center was about. Thiry understood that they needed the involvement, cooperation, energy and ideas of the clinic managers, the front-liners who make the centers work. A DaVita University and DaVita Academy were set up to provide training and build friendship and a feeling of team spirit among those who took the class together and to engage people fully in the DaVita spirit and way of relating to each other. The importance and role of DaVita’s values were embedded into the recruiting process.

From the case of Berkshire’s DaVita, value investors can draw a mental model of frugal innovators:

- Unique business model with a deep domain knowledge that solves a major problem, creates a sustainable, mass-customized personalized solution, and shares in the benefit from the customer’s improved experience

- Customer involvement throughout lifecycle, shaping customer behavior, using customers to motivate employees, and co-creating value with customers: With its unique total “managed care” business model for the customers, they are more engaged at every stage of the product or service life cycle, and this longer-term engagement can be capitalized into making the operational and innovation process frugal with more market-focused, cost-effective and agile R&D solutions, saving precious time and labor in the process. The business unlearns the insular and costly business practices that have been built on long and linear development cycles with little, or at best arm’s length, customer involvement.

- Flexing of organizational assets, sharing of resources, “distribution” and “delivery” to the last mile, integration of technology into the business model to bring about an informational advantage in the delivery of customer experience

- Emphasis that frontliners matter in the value creation process, engaging and empowering them with decision rights and accountability, transferring the deep domain knowledge to frontliners, acknowledging their efforts and potential as a whole person

- Fostering a unique aspirational culture with Focus, Purpose and bold Commitment

- NO COMPLEX FINANCIAL ENGINEERING SCHEMES TO GENERATE SHORT-TERM OPPORTUNISTIC PROFITS

In Asia, when we hear frugal innovation, perhaps one of the first images that come to mind could be Tata Motors Nano car, the lowest priced car in the world, which underperformed its massive expectations. Nobody wants to be seen driving the lowest-priced car! Frugality was not crafted into a higher purpose of values that customers aspire towards, akin to the case of Ryohin Keikaku (TSE: 7453 JP), the owner and operator of MUJI, the “no-brand” retailer whom we had written in the earlier article “Brand It Like Buffett in Asian Wide-Moat Consumer-Brand Innovators” in how they made “frugality” and simplicity an aspirational value for its loyal base of hardcore consumers to embrace. Another image that comes to mind is China’s Xiaomi, the low-cost smartphone that was first launched with basic features and then use suggestions from millions of consumers to add new and better functions to their products, which they bring to market within weeks and using their own online distribution platforms to cut out the middleman. Thus, there are astounding success stories in Asia about frugal innovators that value investors and entrepreneurs can learn from. We find that the most outstanding successes are usually organizational-wide business model innovations, like DaVita and MUJI, as opposed to product innovations. Unless of course these product innovators are like the Godrej Group who has fostered a culture of innovation over the decades to create continuous product innovations.

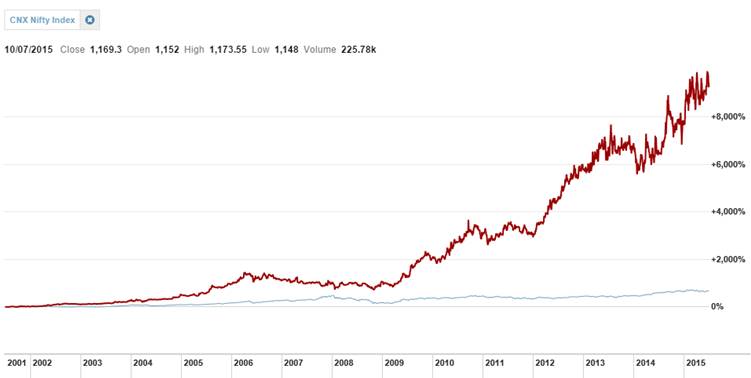

Godrej Consumer (NSI: GODREJCP) – Stock Price Performance 2001-2015 Vs Nifty Index

Godrej’s steel almirah was made in 1923 and built to last, one of Godrej’s guiding philosophies for all its products. It is also a timeless icon of a father’s love for his daughter as her wedding gift that says, Keep my love safe, You are my gold. G. Sunderraman and Sanjay Lonial with the ChotuKool, a low-cost refrigerator designed for India’s poorest households.

We wrote about the frugal innovator Godrej and its low-cost refrigerator ChotuKool targeted at the bottom-of-the-pyramid consumers in an earlier article “Keepers of the Flame: Revisiting the Origins of Compounders in India and Asia” when we visited leading companies in India (Mumbai, Delhi, Pune) in Dec 2013:

<ARTICLE SNIPPED>

********

Benjamin Franklin, one of the founding fathers of the United States and the archetypal Bamboo Innovator says it best about frugal innovators:

“The way to wealth is as plain as the way to market. It depends chiefly on two words, industry and frugality: that is, waste neither time nor money, but make the best use of both. Without industry and frugality nothing will do, and with them everything.”

Which are the other three frugal Bamboo Innovators in Asia mentioned in the article?

Read more at the Moat Report Asia: http://www.moatreport.com/updates/

PS: An Announcement…

We have shared our earlier plans to launch a series of innovative and transparent smart-beta indexing products based on the Bamboo Innovator methodology to systematically identify and invest in neglected, overlooked, misunderstood and underappreciated wide-moat resilient business models with a scalable fund capacity build-up.

In order to accelerate this collaborative plan, I will be joining a listed investment holding company, which has a market capitalization value of over S$300 million, with effective from 1 September 2015 as their Chief Investment Officer (CIO) to spearhead this business project, in addition to taking care of the sustainable outperformance of the listed equities investments, and to source for and add value to undervalued high quality private equity opportunities, together with a dedicated team of seven business analysts (including myself). I am very excited and grateful to be joining the team to create value for the supporters; over 200 shareholders turned up at the Annual General Meeting last week asking great questions.

Back in 1997, Dell CEO and founder Michael Dell had been quoted as saying that he would liquidate Apple and return all the cash to shareholders if he owned the company. This prompted Steve Jobs to get up in front of his team and say the following:

“The world doesn’t need another Dell or HP. It doesn’t need another manufacturer of plain, beige, boring PCs. If that’s all we’re going to do, then we should really pack up now. But we’re lucky, because Apple has a purpose. Unlike anyone in the industry, people want us to make products that they love. In fact, more than love. Our job is to make products that people lust for. That’s what Apple is meant to be.”

To paraphrase Jobs, perhaps the investment world does not need another star fund manager, as opposed to an asset management organization that is able to scale up sustainably because of its process-driven investment know-how. There seems to be something missing in the long hard chase for performance in the asset management and wealth management industry. Stage 1.0 is revolutionized by John Bogle’s passive low-cost index model introduced 40 years ago in 1975 as Vanguard. Stage 2.0 is disrupted by Robert Arnott’s Research Affiliates (RAFI) in 2002 and Jonathan Steinberg’s WisdomTree (WETF) in 2006 with their fundamentals-weighted indexing with quant-based criteria that include sales, earnings, book value, cashflow, dividend yield, and so on. Over $2 trillion in funds have shifted from the conventional fund management business to these indexes. However, fundamentals-indexing has become an overcrowded strategy with everyone copying and chasing the same quant factors generating diminishing marginal risk-adjusted returns and also made unnecessarily complicated with multi-factors thrown into the black box that is increasingly darker.

Importantly, the existing smart indexes are not necessarily adapted to the Asian capital jungles with (1) its distinctive potential accounting tunneling fraud and misgovernance risks with high-net-cash-in-balance-sheet stocks unravelling in accounting scandals, as well as (2) the type of business models that are competitive and increasingly valuable in the Asian business environment.

Imagine if there is a smart-index that can take away the fear factor of investing in Asian accounting fraudulent stocks with deceptive visual signals that include low price-to-book, low PE ratios, high profit margins and ROE, decent accounts receivables and inventory turnover period, and high net cash as percentage of market cap.

The index also goes one more step to eliminate the alluring value traps without a resilient and innovative business model.

This systematic process combines financial data with a wide array of contextual information – including the analysis of governance, group structure and ownership, suspicious related-party transactions, money-go-round off balance-sheet activities, textual/linguistic analysis of news about the company and management, the proprietary Bamboo Innovator business model analysis – and looking through this lens to reach fresh insights in assessing firm value and performance. More than 96% of companies are eliminated in the process – around 30% are those with a higher likelihood of fraud or governance breakdown, and around 60% are potential “value traps”. What’s left is a Watchlist of around 550 companies. This watchlist filters down to 230+ companies, or 1.5% of the original investment universe.

The Asian Bamboo Innovator Index fund will be scalable with a clear and scalable fund capacity buildup of at least $1 billion (an equal-weighted index of 200 stocks meeting liquidity requirements with up to $5 to $20 million in each stock), rebalanced every quarter and periodically in the event of major corporate actions such as spinoffs or corporate restructuring. Related funds using the same scalable know-how, including a concentrated fund that holds 20-30 stocks, will also be offered for investors.

This is what we wrote in our very first issue of the Bamboo Weekly Insight on 6 June 2013:

“Intuit’s former Chief Technology Officer and entrepreneur David Murray summed up his years of experience in remarking that we are great at solving problems but less adept in defining the right problems. LinkedIn’s founder Reid Hoffman expounded on this when he said that it’s really asking “How can I help?” and to “fulfill needs, solve problems”. The primary problem for value investors in Asia is that the beautiful macro Siren is alluring but dangerous at the micro or firm-level, leaving even experienced money managers shipwrecked before they reach their target destination for their clients. This Bamboo Innovator research product is meant to solve this problem.

A longer-term plan in the works will be to develop a Bamboo Innovator index product. The self-indexing trend to embed “smart-beta” investment strategies, such as weighting companies by low-volatility or by fundamentals such as dividends or “value” attributes, have proven to be a meaningful displacement to the active fund managers, private bankers and financial advisors who have thrived by shifting client’s assets around according to the “flavor of the month” or some hot popular themes to generate lucrative fees and expenses to the detriment of the investor. Gather assets via attractive middleman/intermediaries/deals and churn the assets. This “people-based” approach has been a contrast to the “know-how”-based management of assets by a resilient investment process to scale up funds to generate sustainable outperformance. The acid test to distinguish between the two approaches is simple: Just ask whether “Is there a larger idea and purpose than the people?” Such “people-based” fund managers and intermediaries have been hit during the global financial crisis as a significant number of Asian fund managers get their “long-term” track record numbers before Oct 2007 while the newer funds are benefiting from the general uptrend from the March 2009 bottom but may not last in the upcoming painful transition phase in Asia for the next five to ten years. Many of them have the mindset to just lure assets in, get the fees, get deals, and cash out.

There is a balance sheet constraint to earnings manipulation both at the country and company level and Asia is in the vortex of this transition phase. Coordinated macro-based and monetary policies – Let’s print and pump together! Let’s all build infrastructure and capacity! – that worked to temporarily overcome the 2007/08 crisis will need to diverge as a result of differences in balance sheet constraints. The pouring in of the thunderous credit growth has not translated into real growth with diminishing returns and even losses from malinvestments.

Interestingly, Rob Arnott’s Research Affiliates who pioneered weighting companies by their fundamentals and economic footprints rather than by market value has resulted in over $100 billion in assets invested or advised by them during the past five years in the aftermath of the crisis. However, perhaps there has been a crowding of assets and most end up pursuing similar quant-based “fundamentals” strategy, resulting in correlated performance and destructive destabilizing price impact in deleveraging crises situations.

Gaining a deeper insight about Asia through the eyes of the innovative resilient compounders and not through the myriad confusing macro, sector and thematic prognosis or even simplistic quant-based “fundamentals” is critical in the next decade as the innovators break apart to outperform in uncertain times. In other words, opportunities will be about identifying and weighting companies by their “moats” and business models, as Morningstar did for its Wide Moat ETF and hopefully the Bamboo Innovator index.

Investing has to be simple in complex times to outperform and compound value, staying clearheaded when we are guided by the Bamboo Innovator as the inner compass in the Asian jungle.

********

It is with great sadness that I am bidding farewell to my students in the Singapore Management University (SMU). I am fortunate to have the chance in helping the students to acquire the required technical accounting competencies and sharing with them the importance of sharpening their critical thinking skills and embracing the right values and ethics. Some kind feedback from the students includes:

- “I am writing to show my gratitude for Prof Kee Koon Boon for his outstanding teaching. As a graduating student in SMU and through my four years education in SMU, Prof Kee is one of the most passionate and knowledgeable lecturers/professors that SMU has.. I cannot emphasize how important is this module to accounting and finance professionals. There have been widespread media reports on accounting fraud scandals in China-based companies. To put it across bluntly, these reports are ex-post and the harm has been done. What the public needs is ex-ante reports to identify these potential accounting frauds. Despite me getting A+ for Financial Accounting module, Management Accounting module and Corporate Reporting & Financial Analysis module, it never occurred to me to judge the accounting numbers beyond their face value. This module has brought great insights to me through the various methods taught to detect accounting fraud. For SMU to continue producing excellent financial professionals, this module on Accounting Fraud should be expanded to take in a larger amount of students genuinely interested in this subject.”

- “I was moved into writing this letter of appreciation letter for Professor Kee Koon Boon for his work done for the module Accounting Fraud in Asia. This module.. will undeniably be one of the most useful course SMU undergraduates will find themselves taking.. his exemplary teaching quality and methods will continue to help nurture graduates with an edge who will be highly sought after by corporations. What Prof Kee is teaching is vitally important, because most accounting systems today are focused on post-mortem fraud, investors today are not equipped with the vital skill of fraud detection ex-ante.. His constant encouragement.. shows his deep concern for our core growth and maturity, not just in terms of academic development and technical skills, but also in terms of our character development and desire to do good for society. He is truly an educator and a teacher, in every sense.”

- “I am touched by your spirit and passion, so keep this teaching style spirit going and impact more students! With that, I would like to thank you for the sharing session from interview to fraud class lessons as well as thank you for leading me in finding the energy of myself.”

- “Besides the technical skills and knowledge, I think there are other aspects of my life that you “value add” to. For example, how to persevere and be positive, how to “hold on together” so that “our dreams will never die”. These are values which other professors will not share. You are one of the most dedicated, hardworking and “on the ball” professors that I have come across.“

- “I have thoroughly enjoyed your lessons so far. In fact your lessons are something that I look forward to during the week. After working in the hedge fund industry for 8 months last year, I find that it is really rare for someone like you to come out and share your insights and experiences with the world, or even to undergraduates like us without expecting anything in return. I truly admire your spirit and generosity that is similar to that of Benjamin Graham or Bruce Greenwald, reputable masters in their own rights. The learning goes beyond the classroom, and the website is a great tool for students and the general investing public to learn as well. At the end of the day, what really matters is how much value you have added in this world. For that, I believe your work has benefited many of the enthusiastic students in class and have educated investors who are keen to invest in Asia but are looking to arm themselves with background knowledge to finesse their way through the Asian capital jungle.”

- “Right on the cusp of entering the working world, we are thoroughly grateful to be on this journey with you. And I say this in a continual manner because I’m certain our journey doesn’t end here. Thank you for your generosity in sharing your knowledge with the class. Thank you for your passion in uncovering fraudulent activities for the good of investors and the quest for rightness. Thank you for your being the genuine spirit that you are, truly committing yourself to the noble cause of educating us and leading us along with you in the pursuit wisdom and character.”

- “There is no thread of doubt that we are learning highly proprietary and beneficial stuff from you and the goodness is beginning to take shape in us slowly. These seeds once sown will grow further with time and I must thank you for showing us to the gates of this new realm and equipping us with the necessary weapons to outlast if not conquer the Asian Capital Jungle eventually. Beyond these, having been through 7.5 semesters with just 5 weeks of SMU life remaining, I must tell you that I count myself really fortunate to have taken your class right before leaving school. I must honestly say that you are the most enthusiastic Prof I’ve met in school and just like the video of the Chinese singer you showed us in class, your great work shines through and has inspired me a lot. Beyond technicalities, it has taught me to be really really thorough in the pursuit for excellence, esp as a young entrant into the financial industry. Your class contains the most practical wisdom compared to other mods in SMU and all this are what ‘true value’ in education really mean.”

- “Thank you for your passion and guidance during the past 4 months. Through this course, I was able to see the various ways accounting fraud can be perpetuated in Asian society. I indeed have a greater awareness of my own shortcomings and have a clearer sense of direction on which career path I should choose in future – to avoid being swayed towards greed and worldly pleasures but instead lead a life of sufficiency, gratefulness and service.”

- “Thank you for the effort and dedication in the materials & speakers you have provided for us! I have learnt knowledge that have been picked up from valued experiences from yourself as well as speakers like Mr Hemant Amin, knowledge that I would not be able to amass unless through the course. I am thankful to have taken Accounting Fraud because you have taught us values together with knowledge. A compass that will continue to guide us in our journey.”

- “The instructor is very dedicated to his job… He also has great experience and insights into current issues and always tries to bring them into context with what we are learning.”

- “… willing to share his insights into different subject matters and let us think deeper into what is taught to us.”

- “… a very caring and understanding professor who takes the effort to encourage students – concepts learnt can be readily applicable to the working world”.

- “… a very responsible and helpful professor who is willing to share his insights to the class. He is also extremely knowledgeable in many aspects and there is a lot to learn from him.”

- “Prof is very approachable and I’m most impressed by his sincerity and passion in sharing valuable lessons with us.”

- “Patient, kind, caring and considerate of individual, special needs of students. Always warm and approachable.”

- “Prof Kee has inspired me with his enthusiasm in learning and the vast knowledge that he possessed. He was very willing to share his wisdom with us and is definitely a great teacher.”

- “Prof Kee is very friendly prof. He makes an effort to get to know each student and is genuinely interested in the conversations of us students. He is also very knowledgeable and passionate about learning. His sincerity is heartwarming and he is a good role model for students. Thank you Prof Kee!”

We will be continuing our course Accounting Fraud in Asia and Wide-Moat Analysis of Bamboo Innovators periodically for lifelong adult learners, professionals and serious value investors. We are grateful to have the economic crime prosecutors at AGC (Attorney’s General Chambers) and institutional fund houses who have expressed interest in these courses.

We are grateful to have your support all this while. Please rest assured that we will continue to pour forth our dedication and utmost effort to deliver more unique value-added solution to our Members.

Warm regards,

KB

The Moat Report Asia

www.moatreport.com

A new monthly issue of The Moat Report Asia is now available!

Access the in-depth idea presentation:

http://www.moatreport.com/members/

This month of July, we highlight Asia ex-Japan’s largest maker of a mission-critical automotive electronics part that is dubbed the “nervous system” in cars whose electronic content is rising due to the Green, Connected, and Autonomous automotive trends. Without this “nervous system”, the various auto parts cannot start and work. While it is considered a Tier-2 auto parts supplier, [Company’s name] directly participates in the design process of Tier-1 suppliers for most of its [Flagship product’s name] to be “designed-in” and as a result, enjoys sole supplier rights during the first 2-3 years following a new model launch. In addition, [Company’s name] has changed its sales model in China from a distributor model to direct selling, forging Tier-1 relationship with the major Chinese automakers, including accounting for over 50% of [Flagship product’s name] used in emerging electric vehicle maker BYD (1211 HK). Its top ten customers account for around 44-50% of sales. [Company’s name] has pursued the strategy of a diversified customer base to lower operating risk so that “no one “no one customer can seal the life and death of [Company’s name]”, and the rest of sales are contributed by hundreds of customers.

In the ruthless cut-throat automotive industry, the fact that [Company’s name]’s EBITDA margin at 33% is twice that of world-class Bosch India (BOS IN), arguably the best auto parts company listed in Asia, and [Company’s name]’s ROE of 20.5% is also higher than Bosch’s 14.5% speaks volume about [Company’s name]’s wide-moat advantage in securing long-term pricing power and earnings sustainability with the major OEM carmakers by winning their trust to strike long-term partnership. Bosch India trades at an expensive valuation premium of EV/EBITDA 42.9x compared to 12.2x for [Company’s name]. [Company’s name], with its technical superiority in developing low-cost innovative solutions and in generating higher profitability and growth, deserves to command comparable a higher valuation. Short-term downside is protected by a decent cash dividend yield of 4% and supported by a healthy net-cash balance sheet generated from internal free cashflow as opposed to external equity or debt funding.

Led by the highly inspiring Mr. C, [Company’s name] has toiled for more than 10 years since it entered China before bearing some of the fruits. [Company name]’s sales has climbed nearly 31% since FY11 while EBITDA growth is stronger at 78% with the impressive improvement in gross margin from 34.2% to 42.1% due to greater sales weight of higher value-add products that include [Flagship product’s name] for electric vehicles (EVs). Now the growth momentum has hit the tipping point for [Company’s name] to accelerate its profitability significantly in its visible long runway to supply the mission-critical automotive electronics part that is dubbed the “nervous system” in cars whose electronic content is rising due to the Green, Connected, Autonomous automotive trends. Net profit and EBITDA could potentially double in the next 5 years by FY2020, pointing towards a doubling in market value. |

nearly 30 years later when Buffett’s 1979 investment in Tom Murphy-Dan Burke’s Capital Cities-ABC was acquired for $19bn by Disney in 1995. Buffett got his payment in Disney shares. At the news conference announcing the deal, Buffett sat on the dais with Disney Chairman Michael Eisner and Cap Cities/ABC Chairman Thomas Murphy, and said: “This deal makes more sense than any other deal I have seen except for the [1986] Cap Cities and ABC deal. It is a merger of the No. 1 content company [Disney] with the No. 1 distribution company [ABC].” Buffett sold off his Disney shares which went on to compound over 500%.

nearly 30 years later when Buffett’s 1979 investment in Tom Murphy-Dan Burke’s Capital Cities-ABC was acquired for $19bn by Disney in 1995. Buffett got his payment in Disney shares. At the news conference announcing the deal, Buffett sat on the dais with Disney Chairman Michael Eisner and Cap Cities/ABC Chairman Thomas Murphy, and said: “This deal makes more sense than any other deal I have seen except for the [1986] Cap Cities and ABC deal. It is a merger of the No. 1 content company [Disney] with the No. 1 distribution company [ABC].” Buffett sold off his Disney shares which went on to compound over 500%.