|

Buffett’s Van Tuyl Auto Dealership: Starfish Vs Spider and Any Wide-Moat Asian Starfish?

“Well, Larry Van Tuyl talked to me six or seven years ago. I understand the business and I think that it is a decent business overall and I think the way Larry runs it is extraordinary. He has these partners in 78 dealerships and so he works on a partner basis. He’s got a terrific record over the years, and you know, it is something that we will own for 100 years. It really fits Berkshire – it’s the kind of business we can expand a lot because there are 17,000 dealers in the country and we are buying 78 of them through this means. So we will get a lot of opportunity to expand the business. This will be a big business for Berkshire. The Van Tuyl Group fits perfectly into Berkshire Hathaway from both a financial and cultural viewpoint. Larry Van Tuyl along with his father, Cecil, spent decades building outstanding dealerships operated by local partners. The Van Tuyl Group enjoys excellent relations with the major auto manufacturers and delivers unusually high volumes at its 78 locations.”

– Warren Buffett commenting on Berkshire Hathaway’s acquisition of Van Tuyl Group, the fifth largest auto dealership firm in the U.S. with $8 billion in sales, at an undisclosed price estimated at around $3 billion

“One thing that business, institutions, governments and key individuals will have to realize is spiders and starfish may look alike, but starfish have a miraculous quality to them. Cut off the leg of a spider, you have a seven-legged creature on your hands; cut off its head and you have a dead spider. But cut off the arm of a starfish and it will grow a new one. Not only that, but the severed arm can grow an entirely new body. Starfish can achieve this feat because, unlike spiders, they are decentralized; every major organ is replicated across each arm.”

– Rod Beckstrom and Ori Brafman in their 2008 book “The Starfish and the Spider: The Unstoppable Power of Leaderless Organizations”

Starfish and Spiders seem to have crawled over the phenomena from Hong Kong’s “leaderless” protests to Buffett’s purchase of Van Tuyl’s network of 78 auto dealers, most of them located in the Southwest and Midwest.

Using the metaphor of “Spider” to depict traditional, top-down organizations and the “Starfish” to represent groups that lack structure, leadership and formal organizations, authors Rod Beckstrom and Ori Brafman in their book “The Starfish and the Spider: The Unstoppable Power of Leaderless Organizations” presented a thought-provoking view on how “Spider” organizations are increasingly being challenged and defeated by the “starfish”. Decentralized organizations exploiting strong networks are creating a wide-moat competitive advantage over conventional, centralized operations and they are incredibly resilient. Power and knowledge is disseminated across the “starfish” organization, and individual units can respond quickly to the increasingly complex internal and external forces of today.

Van Tuyl has a unique operating structure in which general managers of the individual dealerships typically retain a stake in their local business. The Van Tuyls commented: “I believe in people, people, people. There is no substitute for good people who really care and do a good job. We cut all of our people in on ownership because we believe that’s the way to go. We’re waiting to get more guys ready for general manager and partner. If they’re part owner, they’re going to look after business a little bit better.” Thus, the starfish organizations like Van Tuyl recognize that in today’s fast-changing and competitive environment, it’s the folks on the ground who have the best real-time information on how the battle is shaping up. They build an environment that respects their opinion, which seeks to make sure they understand the mission, and simultaneously empowers them to take the fight to the enemy in a way that optimizes their chances of success in whatever conditions they might find themselves.

Because each of Van Tuyl’s 78 dealerships is itself a partnership, a separate legal entity, like a starfish, the details of Berkshire’s acquisition took many months. Buffett added: “I like the Van Tuyl people enormously. But if I had had to deal with the contract’s complications, I probably wouldn’t have lasted it out.” The accounting for partnerships and joint ventures is also complicated by the IFRS 11 Joint Arrangements accounting standard. Under the US GAAP, JVs are accounted for using the equity method. Before IFRS 11, JVs may be accounted for under either the equity method or proportional consolidation but now IASB requires the use of equity method to bring about comparability of financial statements on a global basis.

<Article snipped>

“It’s easy to mistake starfish organizations for spiders,” the authors warn. Both have the appearance of multiple “legs” or divisions/units. So what are the distinctive characteristics of these “starfish”? There are five legs to a decentralized organization that can help it take off: (1) circles, (2) the catalyst, (3) the pre-existing network, (4) an ideology, and (5) a champion. Circles are essentially independent, autonomous groups that function on the basis of some implicit norms. The catalyst is the person who initiates a circle and then cedes control to its members, developing the idea, sharing it with others, and leading by example. Ideology is the glue that holds people together within such circles. Without access to the culture of trust prevalent in a pre-existing network, it is almost quixotic to attempt to build a decentralized organization. There is a champion who promotes the idea relentlessly. Instead of command and control through rational, powerful, directive instruments to organize and bring about order, the catalyst is a peer connecting people, who show: a genuine interest in others, a desire to help, a tolerance for ambiguity, and the ability to map new connections, to meet people where they are, to inspire others, to let go.

So is the starfish really undefeatable? The starfish can disintegrate quickly once the indestructible intangible ideology or trust is weakening. For instance, if the HK student protesters start to be aware that their actions have caused tremendous distress to the livelihoods and rights of the ordinary citizens that they are fighting for, confusion strikes the starfish about the legitimacy of its ideology and the terrifying strength starts to fade away. Similarly, the introduction of wealth and tangible rules and rights into the starfish may disperse the power of the starfish. The U.S. government finally bested the Apaches, for instance, when it provided its leaders with cattle, a form of wealth that reshaped the amorphous, nomadic tribes into easily manageable hierarchies. As the authors put it, “The moment you introduce property rights into the equation [be they intellectual, physical, or otherwise], everything changes: The starfish organization turns into a spider.”

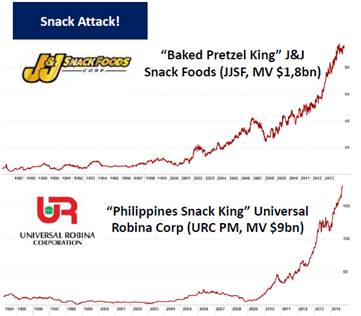

Having got a clearer understanding about starfish organizations, are there any Asian starfish? From our Bamboo Innovator Index of 200+ companies, we think … have qualities of the starfish just like Van Tuyl, Jim Pattinson Auto and O’Reilly Automotive.

Asian Wide-Moat Starfish #1 and #2 – Stock Price Performance

<Article snipped>

********

“When you give people freedom, you get chaos, but you also get incredible creativity”. Starfish organizations are incredibly resilient and powerful because they work on the fundamental premise that their employees and business partners are good, can be trusted and wish to contribute. However, the powerful forces of the starfish can be abused like in the case of the “leaderless” terrorist networks al-Qaeda and ISIS. German philosopher Friedrich Nietzsche said, “One must still have chaos in oneself to be able to give birth to a dancing star.” To this, we add, “One must cultivate ‘emptiness’ as a Bamboo Innovator to be able to give birth to a resilient and positive dancing Starfish.”

Warm regards,

KB

Managing Editor

The Moat Report Asia

www.moatreport.com

SMU: http://accountancy.smu.edu.sg/faculty/profile/108141/Kee%20Koon%20Boon

To read the exclusive article in full to find out more about the story of the wide-moat starfish business model and companies in Asia, please visit:

- Buffett’s Van Tuyl Auto Dealership: Starfish Vs Spider and Any Asian Starfish? Oct 6, 2014 (Moat Report Asia, BeyondProxy)

|

|

“In business, I look for economic castles protected by unbreachable ‘moats’.”

– Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia. Together with our European partners BeyondProxy and The Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produce The Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times. Our Members from North America, the Nordic, Europe, the Oceania and Asia include professional value investors with over $20 billion in asset under management in equities, secretive global hedge fund giants, and savvy private individual investors who are lifelong learners in the art of value investing.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

- Individual subscription at $1,994 per year:

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our subscribers.Questions range from:

- The nuances of internal dealings in Asia, including the case discussion of the recent deal in which HK billionaire’s Lee Shau-kee Henderson Landacquiring Towngas or Hong Kong & China Gas (3 HK) from his family holdings, seemingly déjà vu from the early Oct 2007 transaction when the market peak.

- The case of F&N Singaporespinning out its property unit FCL Trust and getting “free” special dividend-in-specie and the potential risk in asset swap restructuring to deleverage the hidden debt in the entire Group balance sheet.

- The dilemma of whether to invest in a Southeast Asian-listed company and hidden champion with a domestic market share of 60% due to family squabbles and a legal suit over the company’s ownership.

- Discussion of the wise and thoughtful 107-year-old Irving Kahn’s investment into a US-listed but Hong Kong-based electronics company with development property project in Shenzhen’s Qianhai zone and the possible corporate governance risks that could be underestimated or overlooked, as well as their history of listing some assets in HK in 2004.. This is also a case study of “buy one get one free” in John’s highly-acclaimed book The Manual of Ideasin which the “free” property is lumped together with the (eroding) core business to make the combined entity look cheap and undervalued. What are the potential areas that value investors need to watch out for when adapting the SOTP (sum-of-the-parts) valuation method in Asia?

- And many more intriguing questions.

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps.

|

| P.S.1 Here is a little more about my background:

KB Kee has been rooted in the principles of value investing for over a decade as an analyst in Asian capital markets. He was head of research and fund manager at a Singapore-based value investment firm. As a member of the investment committee, he helped the firm’s Asia-focused equity funds significantly outperform the benchmark index. He was previously the portfolio manager for Asia-Pacific equities at Korea’s largest mutual fund company.

He holds a Masters in Finance and degrees in Accountancy and Business Management, summa cum laude, from Singapore Management University (SMU) and had also published articles on governance and investing in the media, as well as published an empirical research paper Why ‘Democracy’ and ‘Drifter’ Firms Can Have Abnormal Returns: The Joint Importance of Corporate Governance and Abnormal Accruals in Separating Winners from Losers in the Special Issue of Istanbul Stock Exchange 25th Year Anniversary Best Paper Competition,Boğaziçi Journal, Review of Social, Economic and Administrative Studies, Vol. 25(1): 3-55. KB has also presented his thought leadership as a keynote speaker in global investing conferences. KB has trained CEOs, entrepreneurs, CFOs, management executives in business strategy, value investing, macroeconomic, industry trends, and detecting accounting frauds in Singapore, HK and China, and had taught accounting at the SMU where he is currently an adjunct lecturer.

P.S.2 Why do I care so much about doing The Moat Report Asia for you?

My personal motivation in embarking on this lifelong journey has been driven by disappointment from observing up close and personal the hard-earned assets of many investors, including friends and their families, burnt badly by the popular mantra: “Ride the Asian Growth Story!” I witnessed firsthand the emotional upheavals that they go through when they invest their hard-earned money – and their family’s – in these “Ride The Asian Growth Story” stocks either by themselves or through money managers, and these stocks turned out to be the subject of some exciting “theme” but which are inherently sick and prey to economic vicissitudes. They may seem to grow faster initially but the sustainable harvest of their returns is far too uncertain to be the focus of a wise program in investment. Worse still, the companies turned out to be involved in accounting frauds. Their financial numbers were “propped up” artificially to lure in funds from investors and the studiously-assessed asset value has already been “tunnelled out” or expropriated. And western-based fraud detection tools and techniques have not been adapted to the Asian context to avoid these traps.

After a decade-plus journey in the Asian capital jungles, it has been somewhat disheartening as I observe many fraud perpetrators go away scot-free and live a life of super luxury on minority investors’ hard-earned money. And these perpetrators make tempting offers to various parties in the financial community to go along with their schemes. When investors have knowledge in their hands, we have a choice to stay away from these people and away from temptations and do the things that we think are right. With knowledge, we have a choice to invest in the hardworking Asian entrepreneurs and capital allocators who are serious in building a wide-moat business.

|