Abe’s Stewardship Arrow to Shoot Down Criss-Crossed Accounting Woes

June 30, 2014 Leave a comment

“Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | June 30, 2014 |

Bamboo Innovator Insight (Issue 40)

|

|

Abe’s Stewardship Arrow to Shoot Down Criss-Crossed Accounting Woes

猫に鰹節(ねこにかつおぶし neko ni katsuobushi) – Local Japanese proverb translated as “fish to a cat”. It means a situation where one cannot let their guard down (because the cat can’t resist stealing your fish).

猫を追うより皿を引け(ねこをおうよりさらをひけ neko o ou yori sara o hike) – Local Japanese proverb translated as “rather than chase the cat, take away the plate”. It means attack problems at their root.

The swooshing sound of the arrow pierces through the hazy air last Tuesday with Abe’s televised address of Japan’s first corporate governance code. More than 120 institutional investors have signed up for the new seven-point Stewardship Code for them to engage with and monitor management team on strategy and governance and speak up for better returns.

The Code is voluntary yet forceful since it requires companies to comply or explain why they cannot follow the rules and would give backbone to the stewardship rules. To understand the implications of Abe’s third arrow aimed at shooting down the cozy cross-shareholding structure that shielded managers from failed investments and bringing shareholders perennially low profitability and returns, we need to travel back to a fishing village in 1921 and also have knowledge of the shortcomings of Japanese consolidated financial statements.

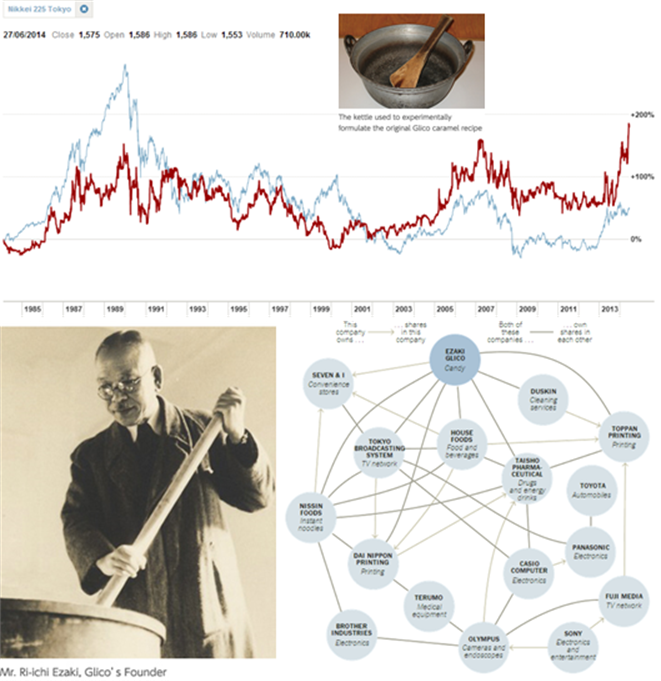

Ezaki Glico (2206 JP) – Stock Price Performance, 1984-2014

Greatly saddened after the death of his sons, Ri-ichi Ezaki sought solace in trip to a fishing village. Ezaki noticed a group of children playing by the seashore and was struck by how healthy they were. He determined that their diet of oysters containing glycogen contributed to their good health. Ezaki began experimenting with means of extracting glycogen for use in other foods, particularly in confectionery, in order to improve the health of other Japanese children. By 1921, Ezaki had launched initial production of his first sweet, a caramel containing glycogen named “Glico.”

Thus, the oyster-to-candy Ezaki Glico (2206 JP, MV $2.1bn) was born in 1922 and is now a confectionery giant with over $3.1bn in sales. Its intangible knowledge in food science technology has also created the hugely popular flagship product for the firm in 1965: Pocky Chocolate, a chocolate-coated, stick-shaped cookie product, which is also known as Mikado for western markets. The name for the product came from the Japanese rendering of the sound (“pokki”) made when the sticks were broken. Pocky is arguably the Asian success story equivalent to that of Oreo biscuit, owned by Kraft’s Mondelez (MDLZ US, MV $63bn), which registered over $2bn in sales. While Oreo has a patent for the secret method to give cocoa powder its characteristic black color, Pocky has no patents. Yet, besides Pepero by Korea’s Lotte Confectionery (004990 KS, MV $2.7bnbn), no other companies has the intangible knowledge to manufacture this seemingly simple coated stick snack. Even wide-moat companies including Mayora Indah (MYOR IJ, MV $2.2bn), Southeast Asia’s largest confectionery maker, Chinese rice-cracker giant Want Want(151 HK, MV $18.6bn) Apollo Food (APOF MK, MV $124m), Hup Seng (HSI MK, MV $286m) were sheepish in admitting they do not possess the manufacturing know-how much as they would like to add this super-seller to their portfolio.

With a brand franchise backed by a relatively strong balance sheet with $558m in gross cash ($275m in “short-term investments”) and over a billion in net asset, Glico has always been the target of many activist investors to push the managers to adopt more shareholder-friendly proposals such as paying out higher dividends and conduct share buybacks. American hedge fund Steel Partners, led by billionaire Warren Lichtenstein, had been the largest single shareholder in Glico since 2004 and tried to force the management to reduce its complicated cross-shareholdings in Japanese companies (see above chart) which resulted in financial losses and eroded the company’s profitability. “Management is responsible for running a good company, not an investment portfolio”, wrote Steel’s boss in 2008. Glico’s keiretsu-like cross-shareholdings include mutual stakes in companies as diverse as Duskin (a cleaning services company which also operates Mister Donut chain), Toppan Printing, TV network Tokyo Broadcasting System, instant noodles Nissin Foods. Steel Partners wanted to overhaul management and bring themselves in as an outside board member. Glico’s network of allies gathered and approved a poison-pill measure that fended off the “abusive acquirer”. By the end of 2008, Steel Partners dumped its 11.8-14.4% stake in Glico.

Steel suffered losses in its activist role in other Japanese companies such as Bull-Dog Sauce (2804 JP, MV $127m) and wig-maker Aderans (8170 JP, MV $618m). Japanese courts ruled in Aug 2007 that Steel was an “abusive acquirer” and cleared the way for Bull-Dog to issue a massive number of shares with 88% of the shareholders voted to adopt a poison pill to defeat Steel’s tender offer bid which was at a 26.7% premium to the previous month’s average price. Similarly, Steel has been in dispute with Aderans since 2007 when the company adopted a poison pill takeover defence. Steel had a 28.9% voting rights in Aderans and value investor Dodge & Cox had 9.3%. Steel had the rare success of replacing the board but still suffered losses from its average price of ¥2,700, according to an analysis of its regulatory filings by RiskMetrics (current price ¥1,560). The travails of Steel and Dodge & Cox had followed from the failed 1989 hostile takeover by T. Boone Pickens of Koito Manufacturing (7276 JP, MV $4bn), a first-tier supplier in the Toyota vertical keiretsu. Even after he became the largest single shareholder with 20% of Koito, Pickens could not put himself on Koito’s board. This was because other members of the Toyota keiretsucollectively controlled more Koito’s shares than Pickens and acted in concert to block him. Thus, cross-shareholdings made it hard for investors to have a voice and the Stewardship Code aims to dismantle this.

Bull-Dog Sauce (2804 JP) – Stock Price Performance, 1985-2014

Japan is both “developed” and “developing” at the same time: developed in the sense of its economic significance as the world’s second largest economy with depth and liquidity in its capital markets, but developing-status when it comes to corporate governance and shareholders’ rights protection due to the legacy of…

<Article Snipped>

Still, it is critical for value investors to understand the accounting dynamics of Japanese companies. Currently, major differences between Japanese accounting standards and international standards deal with accounting for business combinations and consolidations as philosophical differences persist between Japanese GAAP and IFRS. The key difference lie in that cross-shareholdings and interlocking ownership structures often make it difficult to differentiate between a parent company and subsidiaries, particularly if holding companies are involved. Below are a summary of the accounting risks, governance pitfalls and institutional dynamics distilled from our past decade plus of investing in Asia and Japan:

1) Parent and Consolidated Financial Statements – The case of Kanebo

One important feature of consolidation reporting in Japan is that both the parent company financial statements are disclosed as well as the consolidated financial statements. Sales between parents and subsidiaries may be recognized as revenue if consolidated financial statements are disclosed (this is prohibited in the United States). The Japanese began to use consolidated financial statements in 1978, at least half a century later than many of the other industrialized countries of the world. Beginning in March 2000…

<Article Snipped>

Anyone who has spent time around cats knows that cats, unlike dogs, bury their deposits with sand or dirt in various concealment actions. Thus, beyond the keiretsu-like hidden accounting woes and governance risks that cannot be identified by western-based quant screens and checklists, value investors should attempt to add the all-important third analytical dimension in identifying Asian wide-moat compounders such as… whether there is a corporate culture that fosters innovation and a resilient business model that have persistent influence on firm performance and value. Otherwise, the opaqueness and complexities of Japanese and Asian companies beyond their accounting numbers can engulf the value investor who is the fish to the keiretsu cat.

To read the exclusive article in full to find out more about the unique governance pitfalls and accounting risk of Japanese companies, including consolidation report and the Tobashi accounting method to disguise losses, as well as the implications of the Stewardship Code for institutional investors that was announced in both Japan and Malaysia, please visit:

Some updates:

1) KB will be going for his two-weeks mandatory military training with night exercises from 1 Jul to 12 Jul, following which KB will be on a business trip to Italy on 13 to 21 Jul as a keynote speaker in Ciccio Azzollini’s sold-out Value Investing Seminar and to attend Value Unplugged 2014. We will resume the Weekly on 28 Jul. Many thanks for understanding.

2) Value Unplugged 2014 and Value Investing Seminar in July in Italy Value Unplugged 2014 (www.valueunplugged.com) in Naples, Italy is now full. We’ll gather in a small, relaxed setting to learn and make friends. We’ll also attend Ciccio Azzollini’s sold-out Value Investing Seminar in July in Trani, Italy — the definitive summer conference for value investors – as one of the keynote speakers. http://www.valueinvestingseminar.it/content_/relatori.asp?lan=eng&anno=2014

3) We have lined up potential video interviews with hidden business leaders in Singapore to value-add to our Members. One of them is an ASEAN-listed subsidiary of a Swiss-listed MNC and one of our savvy subscribers Mr K had quadrupled his investments after listening to our interview on BeyondProxy in March 2013. Another is a business model akin to the early stages of wide-moat compounders Hero Motocorp and Bajaj Auto which one of subscriber, a hugely successful value investor, commented that one of his biggest mistakes (error of omission) is not investing during the early days of Hero and Bajaj because he thought these were heavy capex animals like the automakers but their business model is frugal innovations in assembly know-how and they are agile creatures with the bamboo characteristics in the “core-periphery network” that is the underlying source of their wide-moat. Because of our lifelong dedication towards investigating the pitfalls of value investing and the underlying sources of wide-moat in both the West and Asia at an early stage, we will contextualize the information in ways no one else had thought about to value-add to you.

4) Our latest Moat Report for the month of July is out. It investigates an Asian-listed company who’s theglobal #1 and #2 maker of two types of patient monitoring devices for both clinical- and home-use. The company is trading at EV/EBIT 9.7x and EV/EBITDA 8.8x and has an attractive dividend yield at 5.6% and a strong balance sheet with net cash as percentage of market value and book equity at 23% and 47% respectively.

|

| The Moat Report Asia |

|

“In business, I look for economic castles protected by unbreachable ‘moats’.” – Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia. Together with our European partners BeyondProxy and The Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produceThe Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times. Our Members from North America, the Nordic, Europe, the Oceania and Asia include professional value investors with over $20 billion in asset under management in equities, secretive global hedge fund giants, and savvy private individual investors who are lifelong learners in the art of value investing.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

Our latest monthly issue for the month of July investigates an Asian-listed company who’s the global #1 and #2 maker of two types of patient monitoring devices for both clinical- and home-use. Founded in 1981 and listed in 2001, the company’s reliable manufacturing technology platform for over 30 years has enabled it to build a global durable franchise in the niche patient monitoring device market that has stable resilient growth and yet is experiencing potential disruptions led by its new innovation. A secret to its success is its in-house capabilities to combine Swiss design, high-precision electronics and sensors components with clinical healthcare to produce world-class products with cost competitiveness. The firm has competitive technology and patents especially its core competence of having an algorithm to allow fast reading/filtering of signals and outputting the accurate results in a short period of time. The company has the potential to consolidate the market further. The company is also a sticky ODM partner to reputable companies including Wal-Mart, Costco, CVS and it has a diversified customer base with none of the customers accounting for more than 10% of its sales. The company demonstrated that it has bargaining power over its powerful customers with the ability to build its own brand since 1998 (62% of overall sales). 91% of its sales are to developed markets in US and Europe. The company is trading at EV/EBIT 9.7x and EV/EBITDA 8.8x and has an attractive dividend yield at 5.6% and a strong balance sheet with net cash as percentage of market value and book equity at 23% and 47% respectively. The firm has also undertaken the unusual capital management program to reduce 10% of its shares outstanding in Sep 2012 to boost capital efficiency by utilizing the comfortable net cash position. The proactive shareholder-friendly stance backed by its strong net cash position should limit any downside in share price. The company’s terminal value and downside risk will be protected by giants such as J&J, Bayer, Abbott etc who wish to swallow it up to possess its valuable manufacturing technology platform and worldwide patents in algorithm-technology. The company’s worldwide patents in algorithm-technology has been commercialized into an innovative product series that is at the heart of its total solution service business model. This valuable intangible asset is not factored into long-term valuation. The innovative product with the algorithm measurement technology are not merely additional features; it “forces” the clinical community to adopt them as the standard, which in turn helps drive home-use penetration as patients seek a consistent and integrated healthcare experience. It transforms the product into a unique strategy that incorporates software development to create value-added services for health monitoring and collaborating with hospitals and governments on tele-healthcare projects. As a result of its wide-moat, the company has a far superior ROE at 20.9% that is nearly double that of its key giant conglomerate rival. When we compare EV/EBIT relative to ROE and ROA, the company is cheaper by as much as 120-150% when compared to its key giant conglomerate rival. The stock price of the company is down nearly 20% from its recent high in end March 2014 on profit-taking by short-term investors. Share price is back to May 2013 level, representing an attractive opportunity to take position in this long-term durable franchise. The stable long-term shareholdings and patient capital by the founder and the management team who together own around 48% of the equity has enabled the firm to adopt a very long-term approach to building its business and cultivating new growth areas. While he may sometimes be slightly over-optimistic and thinking too far ahead with his long-term opinions, this idealistic engineer-visionary-philosopher has done a fantastic job in continuously defying the odds of many skeptics by growing the company from a small startup into one of the world’s leading patient monitoring equipment company. He is the rare Asian entrepreneur who was persistent in building his own brand despite the threat of offending his ODM customers. He was also early in cultivating and coordinating a global network with high-tech component, R&D and manufacturing in his home country, manufacturing, assembly and packaging in Shenzhen, China and medical R&D and clinical testing center in Europe, including making the difficult decision to establish a direct marketing sales force in Europe and North America given the high cost. Unlike most Asian business owners whose interest and focus in the core business starts to wane due to complacency from growing personal wealth and the inability to scale the core business, the founder is genuinely passionate in the company’s ability to add value to the patients and society. The firm can effectively run without the founder with the long-term corporate culture and management system in place, yet he can inject great value as the steward in new innovations; we believe that this combination is rare for an Asian company and deserves a valuation premium.

Our past monthly issues examine:

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our subscribers.Questions range from:

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps.

|

| Professional Development Workshops for Executives and Lifelong Learners |

|

Our 8th run of the series of workshop From the Fund Management Jungles: Value Investing Exposed and Explored– (Part 1) Moat Analysis, (Part 2) Tipping Point Analysis and (Part 3) Detecting Accounting Fraud – on 14 June 2014 has been well-received with serious value investors, professionals, and serious lifelong learners attending, with some who flew in from Jakarta and KL!..

Our 9th workshop will be on Detecting Accounting Fraud Ahead of the Curve sometime later in the year.

Thank you for your support all this while!

|

|

Thank you so much for reading as always.

Warm regards, KB Kee

Managing Editor The Moat Report Asia Singapore Mobile: +65 9695 1860

A Service of BeyondProxy LLC 1608 S. Ashland Avenue #27878 Chicago, Illinois 60608-2013 Other offices: London, Singapore, Zurich

|

|

P.S.1 Here is a little more about my background: KB Kee has been rooted in the principles of value investing for over a decade as an analyst in Asian capital markets. He was head of research and fund manager at a Singapore-based value investment firm. As a member of theinvestment committee, he helped the firm’s Asia-focused equity funds significantly outperform the benchmark index. He was previously the portfolio manager for Asia-Pacific equities at Korea’s largest mutual fund company.

He holds a Masters in Finance and degrees in Accountancy and Business Management, summa cum laude, from Singapore Management University (SMU) and had also published articles on governance and investing in the media, as well as published an empirical research paper Why ‘Democracy’ and ‘Drifter’ Firms Can Have Abnormal Returns: The Joint Importance of Corporate Governance and Abnormal Accruals in Separating Winners from Losers in the Special Issue of Istanbul Stock Exchange 25th Year Anniversary Best Paper Competition,Boğaziçi Journal, Review of Social, Economic and Administrative Studies, Vol. 25(1): 3-55. KB has also presented his thought leadership as a keynote speaker in global investing conferences. KB has trained CEOs, entrepreneurs, CFOs, management executives in business strategy, value investing, macroeconomic, industry trends, and detecting accounting frauds in Singapore, HK and China, and had taught accounting at the SMU where he is currently an adjunct lecturer.

P.S.2 Why do I care so much about doing The Moat Report Asia for you? My personal motivation in embarking on this lifelong journey has been driven by disappointment from observing up close and personal the hard-earned assets of many investors, including friends and their families, burnt badly by the popular mantra: “Ride the Asian Growth Story!” I witnessed firsthand the emotional upheavals that they go through when they invest their hard-earned money – and their family’s – in these “Ride The Asian Growth Story” stocks either by themselves or through money managers, and these stocks turned out to be the subject of some exciting “theme” but which are inherently sick and prey to economic vicissitudes. They may seem to grow faster initially but the sustainable harvest of their returns is far too uncertain to be the focus of a wise program in investment. Worse still, the companies turned out to be involved in accounting frauds. Their financial numbers were “propped up” artificially to lure in funds from investors and the studiously-assessed asset value has already been “tunnelled out” or expropriated. And western-based fraud detection tools and techniques have not been adapted to the Asian context to avoid these traps.

After a decade-plus journey in the Asian capital jungles, it has been somewhat disheartening as I observe many fraud perpetrators go away scot-free and live a life of super luxury on minority investors’ hard-earned money. And these perpetrators make tempting offers to various parties in the financial community to go along with their schemes. When investors have knowledge in their hands, we have a choice to stay away from these people and away from temptations and do the things that we think are right. With knowledge, we have a choice to invest in the hardworking Asian entrepreneurs and capital allocators who are serious in building a wide-moat business.

|

CONNECT WITH US CONNECT WITH US |

| MOAT REPORT ASIA OUR TEAM SUBSCRIBE MEMBERS CONTACT US

The Moat Report Asia Other offices: London, Singapore, Zurich |