|

Can the Market Add and Subtract? The Puzzling Yahoo Negative Stub from Alibaba’s Soaring Value and Are There Other Stubs in Asia?

Do you believe in “reincarnation” in asset pricing? We seem to have entered into such a vortex with the explosive listing of Alibaba, China’s dominant ecommerce company, on 19 Sep, 2014. Yahoo (YHOO, MV $40.7bn) is now valued at less than its $45bn stake in its Asian assets, which include 16% in Alibaba (BABA, MV $231.4bn) and 35% in Yahoo Japan (4689 JP, MV $23.1bn), or an implied valuation of negative $5bn (excluding $6.6bn in cash from selling bits of Alibaba over the years) for the core online-ad business.

The earlier version happened on March 2, 2000 when 3Com carved out 5% of Palm for a public listing to unleash its true value and declared that it would eventually spin off its remaining 95% stake to 3Com shareholders at a ratio of 1.5 Palm shares for every 3Com share before the end of the year. The 3Com shares thus represented 95% ownership of Palm and its non-Palm core business which were less fashionable but more profitable than Palm. At its height, 3Com also owned the naming rights to the San Francisco stadium where the city’s 49ers football team plays. In other words, 3Com should trade for more than 1.5 times the price of Palm stock. The day before the Palm IPO, 3Com closed at $104 per share. After the first day of trading, Palm closed at $95 and soared 4-folds in value to $53.4bn, implying that 3Com should have jumped to at least $145. Instead, 3Com fell to $81.8 and languished at $28bn. Investors were willing to buy expensive shares of Palm rather than to buy the cheap Palm shares embedded in 3Com and get 3Com thrown in. The “stub value” of 3Com was negative $63 per share: the non-Palm core business of its parent had an implied valuation of negative $25bn. Yet, this mispricing does not create exploitable arbitrage opportunities. Over the next two years, Palm shares plunged by more than 90%. 3Com was later acquired in 2009 by HP (HPQ, MV $68.6bn) for $2.7bn.

An even earlier version happened in 1923 when the young fund manager Benjamin Graham noticed that althoughDu Pont (DD, MV $65.2bn) owned a substantial number of GM (GM, MV $54.5bn) shares, DuPont’s market capitalization was about the same as the value of its stake in GM. Pierre du Pont, under his presidency, had used surplus cash to buy a large block of GM shares. Du Pont had a stub value of zero despite the fact that Du Pont was one of America’s leading industrial firms. Graham bought Du Pont and shorted seven times as many shares of GM and profited when Du Pont subsequently rose.

3Com, Du Pont and Yahoo are “equity stubs” in which publicly-traded subsidiaries or investments make up a surprisingly large fraction of the value of their parent company, so that the equity stub – the claim to the parent company’s businesses outside of the subsidiary – has low or even negative value.

<Article snipped>

An important question for value investors is whether there are other stubs in Asia that are not seductive value traps? We wish to distinguish stubs from sum-of-the-parts (SOTP) situations which are mainly a hodgepodge of multiple diversified bets and mainly comprise of some property assets. Stubs are akin to the investments Naspers (NPN SJ, MV $50.4bn) made by capital allocator Koos Bekker in Tencent (700 HK, MV $151bn). Naspers paid $30m to buyout 50% of Tencent in 2005 before its 2007 listing and now its 33.85% stake in Tencent is worth $51B, more than its $50.4bn market value.

From our observation, most Asian entrepreneurs are…

<Article snipped>

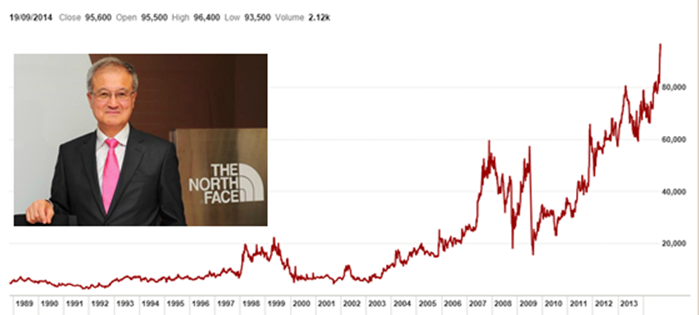

An Asian-Listed ‘Stub’ Helmed by Third-Generation Leader Mr. S – Stock Price Performance, 1982-2014

Charles Kettering (1876-1958), the American inventor-entrepreneur, had said, “You will never stub your toe standing still. The faster you go, the more chance there is of stubbing your toe, but the more chance you have of getting somewhere.” To avoid being stubbed in the toe by sum-of-the-parts (SOTP) value traps that are prevalent in the Asian capital jungles such as Taihan, it is critical to keep in mind the underlying wide-moat business model that is the foundation to generate sustainable cashflow in quality stubs such as … in order to journey far in Asia.

Warm regards,

KB

Managing Editor

The Moat Report Asia

www.moatreport.com

SMU: http://accountancy.smu.edu.sg/faculty/profile/108141/Kee%20Koon%20Boon

To read the exclusive article in full to find out more about the story of the other “stubs” in Asia, please visit:

- Can the Market Add and Subtract? The Puzzling Yahoo Negative Stub from Alibaba’s Soaring Value and Are There Other Stubs in Asia? Sep 22, 2014 (Moat Report Asia, BeyondProxy)

|

|

“In business, I look for economic castles protected by unbreachable ‘moats’.”

– Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia. Together with our European partners BeyondProxy and The Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produce The Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times. Our Members from North America, the Nordic, Europe, the Oceania and Asia include professional value investors with over $20 billion in asset under management in equities, secretive global hedge fund giants, and savvy private individual investors who are lifelong learners in the art of value investing.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

- Individual subscription at $1,994 per year:

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

Our latest monthly issue for the month of September investigates a Malaysian-listed company who is the #1 private pharmaceutical wholesaler and also one of the largest private sector manufacturer of off-patent medicines in its domestic market. Its integrated business model from pharma manufacturing to wholesale, distribution and marketing has carved out top-selling own-branded products such as #1 in medicated powder, #1 cough mixture, #1 cough expectorant etc. With its network of warehouses strategically located throughout the country, the company is able to provide comprehensive coverage and rapid access to markets and customers, delivering the “Medicines on Call” value proposition to over 4,000 private-sector customers from private hospitals, pharmacies to supermarkets and also serves as the long-term channel partner to international brands such as GSK, J&J, 3M, Colgate Palmolive, Nestle for over 30 years etc. From FY2014 onwards, the company has operationalized the business to contract manufacture orthopedic components for top MNCs with the full array of machining, casting, coating and forging capabilities. In an economy where fortunes are built from government concessions or licenses, the company has forged a different path by relying on its own capabilities to provide quality pharmaceutical products and healthcare services largely in the private sector. In an economy where fortunes are built from government concessions or licenses, the company has forged a different path by relying on its own capabilities to provide quality pharmaceutical products and healthcare. Dr K, the chairman and CEO, and his management team have exercised prudence and discipline in executing their operations and capex plans with a strong balance sheet fortified by net cash that’s around 10.5% of market value while deepening their core competencies in warehousing, logistics, sales and marketing to connect to the fragmented market of over 4,000 clients. For the business model of a pharmaceutical wholesaler-distributor, working capital management is critical. In terms of inventory management efficiency, at the inventory turnover period of 42 days, the company is nearly twice as efficient as state-linked giants and is nearly on par with world leaders McKesson and AmerisourceBergen, an impressive feat given the logistics challenge in emerging markets. The company’s 9.6% ROA is nearly double that of state-linked leader. AtEV/EBIT 10.1x, EV/EBBITDA 8.4x, PE14e 10.2x and P/Book 1.9x, the company is reasonably decent in valuations for its resilient earnings and cashflow growth. Giant drug dealers McKesson (MCK US, MV $44.4bn) and AmerisourceBergen (ABC, MV $17.4bn) are also on the global hunt for acquisition targets; McKesson has bought Germany’s Celesio, one of Europe’s largest drug distributors, for $5.4bn in 4Q13, to link up the supply chains of Europe and US; ABC has acquired a 19.9% stake in Brazilian drug wholesaler Profarma in March 2014 for $100m. More consolidation in the sector globally is likely and could be the catalyst to drive up the valuation of quality emerging market companies in the sector. Long-term downside protection in terminal value is provided by MNCs who will be interested to acquire or partner with the company to possess its valuable wide-moat advantage in its network of warehouses and wholesale-distribution know-how to reach the fragmented customers. The company has achieved an impressively consistent and improving performance in difficult times and is well-positioned in the local pharmaceutical industry which is among the few industries quite unaffected by economic cycles as the demand for drugs will continue even in difficult times. Public healthcare services in Asia face the problem of social and financial sustainability and the overcrowded public hospitals and clinics have sparked growing demand for reasonably-priced and quality private healthcare services, generic drugs and consumer healthcare products of which the company is a key provider and beneficiary.

Our past monthly issues examine:

- An Asian-listed company who’s the leading ecommerce group in its home country with the complete platform coveragein the Amazon-type of B2C ecommerce of selling directly to end consumers (Sales/Net Profit: 90%/78%), Rakuten-type of B2B2C platform (Sales/Net Profit: 4%/12%) to support the online SME merchants who in turn sell to the end consumers, and the eBay-type of C2C auction site (Sales/Net Profit: 2%/21%) where individuals buy and sell to one another. This “Amazon-Alibaba” is highly profitable with recurring free cashflow (FCF yield 4.6-5% compounding at 25% in the next 3-5 years) by pioneering the world’s-first 24-hour delivery promise and guarantee when world-class logistics experts said it cannot be done. In emerging markets and Asia where logistics costs is 15-20% of GDP, most ecommerce companies fail to scale up due to lack of fulfillment capabilities and inventory risk became the killing blow as they pursue growth without the intangible know-how. The company designs and builds its own warehouses to provide fast and efficient delivery with 99.68% on-time rate and also complete backend services to suppliers, widening the gap between itself and peers. With its superior infrastructure, the company is able to provide consumers a one-stop shopping experience with all goods purchased from different vendors packaged into a single box and delivered to the client’s door. The company has consignment agreements with suppliers which allow it to have control over inventory management but carry no liability of inventory on its balance sheet, in other words, there is minimal inventory risk for the company to scale up sustainably and without the usual accounting risks that plagued the ecommerce companies. With (1) a superior ROE of 23.6% due to its wide-moat business model in 24-hour delivery system, (2) negative cash conversion cycle (-29 days) in its unique warehouse system with minimal inventory risk, (3) a sustained 25-30% recurring earnings and cashflow growth per annum in the next 5 years, especially a long run-way in disrupting traditional retailers, and (4) potential exponential growth in its option value in the third-party electronic payment business, the company can scale up multiple times. Short-term downside risk is protected by its healthy $128m net-cash balance sheet (15% of MV) and proven management execution in prudent capex expansion to support sustainable quality earnings growth. Its terminal value and long-term downside risk will be protected by giants Alibaba, Rakuten, eBay, Amazon who wish to swallow it up to possess its valuable trust and brand equity support it enjoys and its wide-moat business model in 24-hour delivery system. The company is one of the few Asian ecommerce companies with good governance and low accounting risks with its net-value revenue recognition method and it deserves a valuation premium. Upcoming deregulation in third-party electronic payment with the passing of the law in Sep 2014 will result in various government restrictions to be removed, paving the way for the company to introduce stored-value payments, O2O payment, P2P payment (money transfer without transactions), multiple currencies’ payments, big data analysis, payment services for customers outside the group to boost transaction volume and scale up its existing proprietary PayPal/AliPay business. Led by the inspiring and highly-determined founder and Chairman who established and listed the company in 1998 and 2003 respectively, the company has overcome the multiple obstacles to ecommerce transactions in its home market. The founder described the obstacles to ecommerce transactions as ‘friction’, and that he “resolve to take on the Life’s Task to reduce this ‘friction’”.

- An Asian-listed company who’s the global #1 and #2 maker of two types of patient monitoring devices for both clinical- and home-use. Founded in 1981 and listed in 2001, the company’s reliable manufacturing technology platform for over 30 years has enabled it to build a global durable franchise in the niche patient monitoring device market that has stable resilient growth and yet is experiencing potential disruptions led by its new innovation. A secret to its success is its in-house capabilities to combine Swiss design, high-precision electronics and sensors components with clinical healthcare to produce world-class products with cost competitiveness. The firm has competitive technology and patents especially its core competence of having an algorithm to allow fast reading/filtering of signals and outputting the accurate results in a short period of time. Thecompany has the potential to consolidate the market further. The company is also a sticky ODM partner to reputable companies including Wal-Mart, Costco, CVS and it has a diversified customer base with none of the customers accounting for more than 10% of its sales. The company demonstrated that it has bargaining power over its powerful customers with the ability to build its own brand since 1998 (62% of overall sales). 91% of its sales are to developed markets in US and Europe. The company is trading at EV/EBIT 9.7x and EV/EBITDA 8.8x and has an attractive dividend yield at 5.6% and a strong balance sheet with net cash as percentage of market value and book equity at 23% and 47% respectively. The firm has also undertaken the unusual capital management program to reduce 10% of its shares outstanding in Sep 2012 to boost capital efficiency by utilizing the comfortable net cash position. The proactive shareholder-friendly stance backed by its strong net cash position should limit any downside in share price. The company’s terminal value and downside risk will be protected by giants such as J&J, Bayer, Abbott etc who wish to swallow it up to possess its valuable manufacturing technology platform and worldwide patents in algorithm-technology. The company’s worldwide patents in algorithm-technology has been commercialized into an innovative product series that is at the heart of its total solution service business model. This valuable intangible asset is not factored into long-term valuation.The innovative product with the algorithm measurement technology are not merely additional features; it “forces” the clinical community to adopt them as the standard, which in turn helps drive home-use penetration as patients seek a consistent and integrated healthcare experience. It transforms the product into a unique strategy that incorporates software development to create value-added services for health monitoring and collaborating with hospitals and governments on tele-healthcare projects. As a result of its wide-moat, the company has a far superior ROE at 20.9% that is nearly double that of its key giant conglomerate rival. When we compare EV/EBIT relative to ROE and ROA, the company is cheaper by as much as 120-150% when compared to its key giant conglomerate rival. The stock price of the company is down nearly 20% from its recent high in end March 2014 on profit-taking by short-term investors. Share price is back to May 2013 level, representing an attractive opportunity to take position in this long-term durable franchise. The stable long-term shareholdings and patient capital by the founder and the management team who together own around 48% of the equity has enabled the firm to adopt a very long-term approach to building its business and cultivating new growth areas. While he may sometimes be slightly over-optimistic and thinking too far ahead with his long-term opinions, this idealistic engineer-visionary-philosopher has done a fantastic job in continuously defying the odds of many skeptics by growing the company from a small startup into one of the world’s leading patient monitoring equipment company. He is the rare Asian entrepreneur who was persistent in building his own brand despite the threat of offending his ODM customers. He was also early in cultivating and coordinating a global network with high-tech component, R&D and manufacturing in his home country, manufacturing, assembly and packaging in Shenzhen, China and medical R&D and clinical testing center in Europe, including making the difficult decision to establish a direct marketing sales force in Europe and North America given the high cost. Unlike most Asian business owners whose interest and focus in the core business starts to wane due to complacency from growing personal wealth and the inability to scale the core business, the founder is genuinely passionate in the company’s ability to add value to the patients and society. The firm can effectively run without the founder with the long-term corporate culture and management system in place, yet he can inject great value as the steward in new innovations; we believe that this combination is rare for an Asian company and deserves a valuation premium.

- The world’s #1 ODM (Original Design Manufacturer) and global #5 manufacturer of a consumer healthcare device product that is used frequently, even daily, thus providing the foundation for stable recurring cashflow. This company is also a hidden champion in a niche product segment (50-55% of group’s sales) that has become a high-growth fashion product currently accounting for less than 10% of the overall industry. The company is able to mass-manufacture this niche product, but not the giants, because of its unique process IP in flexible manufacturing system and know-how to handle large-scale complex orders. The manufacture of this product itself is difficult to replicate and requires FDA/CE licenses because of its medical device nature and the entry barrier is not capital but the know-how and R&D expertise. In particular, the manufacturing integrates different fields of science including polymer chemistry, physics, optics, engineering, materials control, process control, microbiology, and, injection molding. The firm has also developed a proprietary system of tracking the manufacturing process of different sets of product so that if a quality issue arose, when and where the problem set of products was being produced could be swiftly identified, thus diminishing the scale and cost of product recall. This system has helped the firm win the long-term trust of its ODM customers to place stable large orders. The Big Four giants do not have such a system and have to incur substantial losses from product recalls. The company also possess its own brand which has many loyal followers and support in its home market where it enjoys a 30% market share and contributes to 25% of group’s saleswhile sticky ODM customers account for 75% of group’s sales, mainly from the Japan market. As a result of its wide-moat advantages, the firm enjoys a consistently high ROE of 41%, double or triple that of the giants. From FY07 onwards, even during the depths of the Global Financial Crisis in 2007/09, the firm has not raised equity. Since listing in Mar 2004, the company has only done one rights issue in May 2005. Also, it is able to sustain a strong stable cash dividend payout (>70% with 3% yield) with its healthy net-cash balance sheet (net cash $30m; net cash-to-equity ratio 23%) and proven management execution in prudent capex expansion to support sustainable quality earnings growth. M&A deals in the healthcare and medical device sector has been growing due to their strong defensive nature and giants seeking growth to overcome their own patent cliff. The firm will always be an attractive takeover target by giants who wish to swallow it up to possess its valuable flexible manufacturing system and know-how to fill their own missing competency gap and hence will enjoy long-term downside protection in its terminal value. In the battle between “ODM vs Brand”, we find the story of the company to be quite similar to that of TSMC (2330 TT, MV $103bn), now the largest ODM foundry in the world. “Skate to where the puck is going to be, not where it has been,” as hockey legend Wayne Gretzky advised. In our view, the profit and valuation premium in the value chain will start to skate to the “Inno-facturers” who are the hidden ODM innovators (the brand behind brands) consolidating the industry, such as TSMC and this company. While its valuation is not cheap with EV/EBIT (FY13) at 20.6x, when we compare EV/EBIT relative to ROE, the company is relatively cheap, by as much as 130-220% when compared to giants and other comparables. When we compare EV/EBITDA relative to ROE, the valuation gap is 90-160%. This long-term valuation gap implies that the company, with its far superior and sustainable ROE, could potentially double to $2.4bn, as it continues to consolidate its niche product segment and enter into a new product cycle of an innovative product whose patents are expiring in 2014/15 (US/worldwide) to make ASP/margin improvements in sustaining quality profits and cashflow. Its share price has dropped 18% from its recent high and underperformed the index by 26% in the last six months. This will present a buying opportunity for long-term value investors who can penetrate beyond conventional valuation metrics because of a deep understanding of its business model and underlying source of its wide-moat advantages. In Asia, many firms break apart or become value traps due to shareholder conflict, envy and differences in opinion on the business direction of the company. The stable long-term corporate culture infused by the late founder, who established the company in 1986 with the current executive chairman and 2 other key shareholders, to combine the energy and ideas of everyone to work hard to keep the business running forever is underappreciated.

- The Home Depot of Asiawhich has the largest market share in its home country and now seeks to expand regionally. It is one of the few home improvement retailers in the world which is able to achieve a structural negative cash conversion cycle (CCC) at -39 days for resilient, recurring and sustainable operating cashflow to enable the expansion of its store network while keeping a healthy balance sheet. It is hard to achieve negative cash conversion cycle (CCC) as a home retailer as compared to a supermarket retailer as the product nature is more durable. Even Home Depot, Lowe’s and Bed Bath & Beyond (BBBY) are not able to achieve a negative CCC. Led by the capable owner-operators since 1995, the company is a pioneer in proactively creating awareness and demand in the minds of consumers that upgrading your home can be fun and in incremental affordable steps. Its creative branding has resulted in the firm to become the “first on customers’ mind”, or what Charlie Munger elucidated as the “psychological wide-moat” advantage. 80% of sales are generated customers looking for home improvement and renovation ideas and solutions. Growth is supported by the management’s proven ability to identify and cater to dynamic changes in customer preferences. The firm’s comprehensive pre and aftersales service creates brand loyalty and sustains long-term sales. The merchandizing management is tailored to the peculiarities of customer preferences in each area to drive same store sales growth with creative customization by store, location, season and events. Its key strategy to expand its profit margin is to increase its higher-margin house brands and product-mix management. Its EBITDA/sqm of $400/sqm was higher than Home Depot until Home Depot experienced a rebound last year to $500/sqm. The firm’s resilient sales are supported by its unrivalled network of diverse locations throughout the country. Its bold vision and successful “Blue Ocean” execution in the highly fragmented second-tier markets has created a powerful wide-moat advantage that will last for many years to come. In short, the management have proven their ability to execute in difficult market and industry conditions especially in the past 5 to 7 years during the 2007/09 global financial crisis with the firm emerging much stronger. The Illinois Institute of Technology engineering graduate and quiet billionaire owner behind the home retailer is one of the few Asian business tycoons who has the thirst to scale up the business in a sustainable way, as opposed to opportunistic ventures, having been largely influenced by his early years experience observing the success of American wide-moat firms. If we can adjust the EV/EBITDA valuation metric to reflect the CCC, the company’s EV/EBITDA of 18.5x will be lower at 10-11x, while Home Depot’s EV/EBITDA 11x will be higher at 13x. Noteworthy is that Home Depot has a negative free cashflow throughout FY1989-2001 (13 consecutive years!) and yet market cap has climbed from $1.5bn to $103bn. Home Depot compounded despite the ugly valuations during the capex ramp-up. This once again highlights that the power of wide-moat is often underappreciated, misunderstood and overlooked. When Home Depot generated $180m in operating cashflow in FY1992, quite similar to this Asian firm now, Home Depot is valued at $5bn (vs $3bn). Store network is expected to double in the next 4-5 years, representing a potential doubling in market value.

- The Northeast Asian-listed companywho is the world’s largest maker of an essential component with applications in apparel, shoes, diapers, car seats etc. All top 20 global athletic shoe brands, including Nike, Adidas, Reebok, Sketchers, UnderArmor are customers and this Asian innovator with R&D capabilities has forged long-term “spec-in” partnerships with them. Its broad product offering is protected by over 110 patents. By locating its Pan-Asian production plant network in China, Taiwan, Vietnam and Indonesia close to its major clients, including sales/customer service centers and warehouses in US and Europe, the firm is better positioned to understand their requirements, deliver fast and meet their needs. While top 10 athletic shoe brands account 40% of its revenue, the firm has a diversified clientele base of over 10,000 customers, giving it resilience and growth with both the established and emerging brands as clients. The company is trading at PE14e 12x, EV/EBITDA 7.1x and EV/EBIT 10.6x with a dividend yield of 3.9%. Interestingly, its EBITDA margin is double that of Adidas and its 8.7% net margin is higher than Adidas’ 5.4%, though below Nike’s 9.8%. Given the tipping point of its Pan-Asian production network and contributions from its new products and as capex tapers off in the next few years, free cashflow could be around $50-60m and applying a P/FCF of 15x would yield a market value of $750-900m,, representing apotential upside of 100-150%. Thus, the firm offers a similar quality growth trajectory to Nike/Adidas with its unique knowledge-based business model and yet trades at a more attractive valuation and higher dividend yield as downside protection.

- The Middleby of Asia commanding a dominant market share of over 80% in hypermarkets, 50% in chain outlets, 30% in 4- to 5-star hotels in China and an overall 30% in its home market. Yet, no single customer accounts for more than 5% of its revenue. Just to recall for value investors, NYSE-listed Middleby, with its sleepy and boring business, has compounded 100-fold from around $50m to $5.7bn since its tipping point in 1999. The founders of this Asian family business demonstrated clear dedication in building up the company with its wide-moat business model backed by a strong and unique distribution/marketing network in finding, winning and binding new customers to build massive brand equity and long-lasting relationships with clients over time. Their devotion to its core product for nearly 20 years results in maximum problem-solving skills, innovative strength and product leadership and hence, to ever greater customer benefit that will protect the company to consolidate the fragmented market and provide ample opportunities to continue its profitable growth. The company is currently trading at PE13e 15.8x and an undemanding EV/EBIT 10.1x and EV/EBITDA 9.5xand its growth potential based on its unique business model is not priced in. There is a structural re-rerating of niche business models with (1) diversified client base, (2) steady revenue streams, (3) lean capex requirements that creates ample free cashflow and defensive growth. Based on PE, P/CFO and EV/EBIT, the company is trading at a 40-50% discount to the foreign listed comparables despite more efficient use of assets in generating profits and cashflow. It has an attractive 7% earnings yield growing at 20% over the next 3-5 years and a 3.8% dividend yield that is supported by its strong cashflow generation ability, steady revenue stream and lean capex requirements to limit downside risks in valuation. Based on the growth plans to penetrate new product and customer segments; build its third plant in India in addition to the ones in its home market and in China; and potential bolt-on acquisition opportunities with its healthy balance sheet in net-cash position, it has the potential to double its operating cashflow in the next 3-5 years and market value could double, representing an upside potential of 100-140%.

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our subscribers.Questions range from:

- The nuances of internal dealings in Asia, including the case discussion of the recent deal in which HK billionaire’s Lee Shau-kee Henderson Landacquiring Towngas or Hong Kong & China Gas (3 HK) from his family holdings, seemingly déjà vu from the early Oct 2007 transaction when the market peak.

- The case of F&N Singaporespinning out its property unit FCL Trust and getting “free” special dividend-in-specie and the potential risk in asset swap restructuring to deleverage the hidden debt in the entire Group balance sheet.

- The dilemma of whether to invest in a Southeast Asian-listed company and hidden champion with a domestic market share of 60% due to family squabbles and a legal suit over the company’s ownership.

- Discussion of the wise and thoughtful 107-year-old Irving Kahn’s investment into a US-listed but Hong Kong-based electronics company with development property project in Shenzhen’s Qianhai zone and the possible corporate governance risks that could be underestimated or overlooked, as well as their history of listing some assets in HK in 2004.. This is also a case study of “buy one get one free” in John’s highly-acclaimed book The Manual of Ideasin which the “free” property is lumped together with the (eroding) core business to make the combined entity look cheap and undervalued. What are the potential areas that value investors need to watch out for when adapting the SOTP (sum-of-the-parts) valuation method in Asia?

- And many more intriguing questions.

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps.

|

|

P.S.1 Here is a little more about my background:

KB Kee has been rooted in the principles of value investing for over a decade as an analyst in Asian capital markets. He was head of research and fund manager at a Singapore-based value investment firm. As a member of theinvestment committee, he helped the firm’s Asia-focused equity funds significantly outperform the benchmark index. He was previously the portfolio manager for Asia-Pacific equities at Korea’s largest mutual fund company.

He holds a Masters in Finance and degrees in Accountancy and Business Management, summa cum laude, from Singapore Management University (SMU) and had also published articles on governance and investing in the media, as well as published an empirical research paper Why ‘Democracy’ and ‘Drifter’ Firms Can Have Abnormal Returns: The Joint Importance of Corporate Governance and Abnormal Accruals in Separating Winners from Losers in the Special Issue of Istanbul Stock Exchange 25th Year Anniversary Best Paper Competition, Boğaziçi Journal, Review of Social, Economic and Administrative Studies, Vol. 25(1): 3-55. KB has also presented his thought leadership as a keynote speaker in global investing conferences. KB has trained CEOs, entrepreneurs, CFOs, management executives in business strategy, value investing, macroeconomic, industry trends, and detecting accounting frauds in Singapore, HK and China, and had taught accounting at the SMU where he is currently an adjunct lecturer.

P.S.2 Why do I care so much about doing The Moat Report Asia for you?

My personal motivation in embarking on this lifelong journey has been driven by disappointment from observing up close and personal the hard-earned assets of many investors, including friends and their families, burnt badly by the popular mantra: “Ride the Asian Growth Story!” I witnessed firsthand the emotional upheavals that they go through when they invest their hard-earned money – and their family’s – in these “Ride The Asian Growth Story” stocks either by themselves or through money managers, and these stocks turned out to be the subject of some exciting “theme” but which are inherently sick and prey to economic vicissitudes. They may seem to grow faster initially but the sustainable harvest of their returns is far too uncertain to be the focus of a wise program in investment. Worse still, the companies turned out to be involved in accounting frauds. Their financial numbers were “propped up” artificially to lure in funds from investors and the studiously-assessed asset value has already been “tunnelled out” or expropriated. And western-based fraud detection tools and techniques have not been adapted to the Asian context to avoid these traps.

After a decade-plus journey in the Asian capital jungles, it has been somewhat disheartening as I observe many fraud perpetrators go away scot-free and live a life of super luxury on minority investors’ hard-earned money. And these perpetrators make tempting offers to various parties in the financial community to go along with their schemes. When investors have knowledge in their hands, we have a choice to stay away from these people and away from temptations and do the things that we think are right. With knowledge, we have a choice to invest in the hardworking Asian entrepreneurs and capital allocators who are serious in building a wide-moat business.

|