| Part 1: A Family Office Investment Journey and Understanding the DNA of Fraudulent PromotersDear Moat Report Asia subscribers in Singapore,I have invited a guest speaker. He is Hemant Amin, founder, chairman and CEO of Asiamin Capital, a low-profile, successful multi-million single family office. He will be talking about his family office investment journey and understanding the DNA of fraudulent promoters in the Indian and Asian context with actual Indian cases accumulated from his wealth of experience in investing in Asia and India, where he is an early investor in Narayana Murthy’s Infosys which compounded over 60-folds for him: http://www.beyondproxy.com/grey-world/. His capital allocation track record over the past decade from 2004 to 2014 is outstanding, compounding at 29.3% and trouncing the S&P index by a factor of 3.6 times over the same period; a $1,000 would yield $16,857 during the period.

After witnessing over the decade plus how the Asian capital jungle has turned increasingly into a fertile ground for insiders-promoters-syndicates who have the incentive and power to manipulate prices and volumes, to deceive investors with fraudulent financial numbers, and to inject market “action” via positive corporate announcements of various sorts to excite the senses but rarely materializing subsequently in economic substance, luring investors and their funds in and then offloading the shares a pump-and-dump stock manipulation scheme, I desperately and madly wanted the SMU students to learn from a rare positive role model in the Asian capital jungle – and Hemant’s name is at the top of my list to invite as a guest speaker to inspire the students.

Hemant showed that it is still possible to win as a value investor because of one having not only the right investing approach but more importantly, having the right values in life. That it is possible to create value without compromising on values in this harsh, pretentious and messy world. That one can avoid investing in the fraudulent promoters by understanding their DNA.

It is immediately obvious that only someone who has a deep thinking process and value system can craft out such thought-provoking insights. Hemant’s carefully-prepared presentation material reflects and exudes his deep introspection, knowledge, resilient investment process and values. Having weathered through adversities and the mental drain in fighting the fraudulent promoters to reclaim the money invested, Hemant’s investment journey took a life-changing turn when he attended Berkshire Hathaway’s AGM in 1997 for the first time – and Hemant has made the pilgrimage to Omaha every year since. Hemant started to focus on the quality of the management and the business model and understood the difference between statistically-cheap cigar butts generated from net-net screens and checklists made famous by Benjamin Graham vs compounders which was the focus of Charlie Munger, the Vice-Chairman of Berkshire Hathaway and the influential partner to Buffett’s success.

Because Hemant’s presentation is so good, I have invited the team of economic crime prosecutors at AGC (Attorney’s General Chambers) Financial & Securities Crime Division who might be coming over for the presentation. The AGC has recently invited me for a talk session on accounting and securities fraud in Asia with their DPPs; it is a great honor and I wish to share with them Hemant’s great insights.

It will be great if you wish to join us on 17 March (Tuesday) at 4.30pm till 7pm.

Warm regards,

KB

The Moat Report Asia

www.moatreport.com

http://accountancy.smu.edu.sg/faculty/profile/108141/KEE-Koon-Boon

PS: We are honored that Hemant is a fellow Moat Report Asia subscriber. We will be making Hemant’s presentation material available for our Moat Report Asia subscribers.

Part 2: Mocking Asia, the Pixar Solution and the R.E.S.-ilence Handle

“If we were to mock Singapore, we would say it is a nation of bankers and real-estate developers. What we would like to become is a nation of entrepreneurs. The country is missing a big trick about how it thinks about entrepreneurial thinking. We make a list of all the things we want to do and we say okay, check, we’ve done that. It’s a list-building mentality. It’s not an opportunity-framing mentality – which is what entrepreneurial thinking is about… You cannot beat Apple by becoming more like Apple… We have to embrace being Asian… We have to build something uniquely Asian.”

– Singapore Management University (SMU) business dean Gerard George in “Thinking Beyond the Checklist”, 13 March 2015

“But my internal sense of purpose – the thing that had led me to sleep on the floor of the computer lab in graduate school just to get more hours on the mainframe, that kept me awake at night, as a kid, solving puzzles in my head, that fueled my every workday – had gone missing. I’d spent two decades building a train and laying its track. Now, the thought of merely driving it struck me as a far less interesting task. Was making one film after another enough to engage me? I wondered. What would be my organizing principle now? My desire to protect Pixar from the forces that ruin so many businesses gave me renewed focus. I began to see my role as a leader more clearly. I would devote myself to learning how to build not just a successful company but a sustainable creative culture. As I turned my attention from solving technical problems to engaging with the philosophy of sound management, I was excited once again – and sure that our second act could be as exhilarating as our first.”

– Pixar’s founder Ed Catmull in Creativity, Inc: Overcoming the Unseen Forces That Stand in the Way of True Inspiration

For the last 50 years in Singapore and Asia, which is built on the foundation of the farsighted pioneers who established the place as a magnet of FDI flow and MNCs, all firms and entrepreneurs had to do was answer the phone from clients and lease more office space. And excess profits are used to reinvest in trading and accumulating property assets and financial engineering activities. “Positional leadership” are prized on those who can maneuver the giant organizational machinery with their “well-rounded” skill-set and climb to the apex. That run is possibly over. Relationship-based deal-making capabilities coupled with access to cheap financing have experienced diminishing marginal returns, even losses, and internal in-fighting and succession woes have fueled a hidden vicious race to the bottom in accounting tunneling of group resources that is hidden at the surface. Like an inverted U-curve that was also highlighted earlier in May 2013 in Pilgrimage to Omaha + Entrepreneurship, Asian-Style:

“As value investors in Asia should know, path dependency has influenced the Southeast Asian (ASEAN) economy, which is the product of a relationship between political patronage and economic elitist power that developed in its initial starting point in the colonial era, and this politics-business nexus was sustained with a different cast of characters. Bet on the wrong jockey (entrepreneur) and the race is over. The Asian horse (business) doesn’t matter much; the ownership of the horse can change, a far more important information to monitor and analyze. Alas to the ones who are not in the insider’s track. These big Asian horses are often grants to quasi-monopoly or regulated/ protected concessions, normally in domestic goods and services industries without a requirement to generate the technological capabilities to compete on the global arena. These asset-based, deal-making trading businesses that form the foundation of many Asian tycoons are akin to elite forms of barber-like “services” in which the fiercely global competition cannot attack with impunity, such as commodities, construction/ infrastructure/ property, financial services. As Joe Studwell pointed out in his insightful book “Asian Godfathers: Money and Power in Hong Kong and Southeast Asia”, Southeast Asia has all the trappings of a modern dazzling economy with its high-tech factories and high-rise buildings but few indigenous, large-scale companies producing world-class products and services. The scraps that trickle down the big, long tables of the Asian tycoons are left to be competed fiercely in a lose-lose situation at the SME level. Even with the export-driven boom, the SME’s role as middlemen in taking and executing orders efficiently from their MNC customers has limited the scalability of their business model.”

Growth and entrepreneurship in Asia is not driven by innovation and science given that every creative field — innovation, science, music, movies, books, art — follows a Power Law. They bring into the world richly valued things which did not exist before. And these creations like Pixar take time and effort of a different nature as compared to the asset-based, deal-making trading businesses and positional leadership skill-set for big corporates in Asia.

From Pixar’s founder Ed Catmull story encapsulated in his inspiring book Creativity, Inc, we can sense and observe that the true innovator and compounder have:

- An idea larger than oneself that fuels their internal sense of purpose

- A burning desire to harness the voice of everyone so that everyone can be co-creators and be involved in the value creation process

- Faced rejection, tasted temptations, are highly misunderstood, and are ever more determined to stay focused, to just work with a palpable sense of urgency, to realize the intangible ideas and Purpose, to keep the flames burning

- Expressions of gratitude, the ability to see value in problematic situations as areas to improve through providing his or her service

Our mental model for navigating the Big Transition in Asia is to identify the Pixars and Bamboo Innovators, investing in the emerging tycoons, the innovators and the wide moats they are building – before they become obvious. We have discussed earlier about the philosophy of “Good is not the absence of evil”: how the value investor can only eliminate the “evil” ones with potential misgovernance and accounting tunneling fraud to limit downside risks – and still neglect and overlook the “good” compounders. And each time round there is a credit crisis punctuating the markets, there is an increasing premium on valuation for wide-moat business models in Asia as the Innovators stood apart from the Imitators and the swarming Incompetents. Value investors in Asia need to take the leap to become more Munger-like in selecting companies with wide moats that can generate compounding returns rather than dwell with a false sense of security in the realm of statistically cheap stocks that turn out to be either fraudulent or value traps.

Starting next week, we will start expanding on these thoughts of finding the emerging tycoons in Asia and the wide moats they are building – before they become obvious. As we have highlighted in “Any Benjamin Franklin in Asia? (Part 2): Reflections from the Story of Linkabit-Qualcomm and the Inverted U-Curve of Singapore/Asia”:

“True compounders have no time to waste and their brains and time are purposed towards ideas larger than themselves. In our interaction with Asian management over the past decade plus, the Bamboo Innovator like to sense this almost child-like fervour and time spent for ideas, which in the Asian context is deemed immature and foolish since the successful wealthy towkays feel that the mind should be occupied by the loud thought of “can make money or not” or “can be more famous and prominent or not”. That makes the difference between a wealthy local tycoon who creates wealth largely for himself or herself with the usually visible display of lifestyle to portray success and posturing activities to gain fame and social respect as compared to the quiet low-profile inventor-entrepreneurs who lived in the basement constantly thinking and worrying and keeping the ideas burning towards the flames of creation and scaling up.”

As we have discussed, a checklist approach in examining “successful” companies might overlook the resilient Bamboo Innovators. After all, there are much larger impressive trees in the forest. By comparison a bamboo looks smaller, thinner, and fragile. The list of Bamboo Innovators is a surprising one; many of them are not the typical ones that one would come across. While the details are always different, certain features of the Bamboo Innovators are remarkably similar to those that resulted in the astonishing vitality in bamboo: the R.E.S.-ilience factors in value creation.

- R stands for “Rootedness” in cultivating a culture of kindness, trust and cooperation to contend with and heal creative dissent and incentivize innovative experimentations.

- E for “Emptiness” like the empty hollow center of a bamboo in having (1) “indestructible intangibles” which in turn derives its strength from either a certain know-how or trust and support in the community; (2) a “core-periphery” network; and (3) an “open-innovation” business model in which both internal and external partners co-develop new products and creations

- S for “Sheath” in leadership to create the context, adaptive-govern, coordinate, synthesize and weave diverse networks and groups who might otherwise be excluded into a coherent whole, rather than the typical command-and-control “positional/title-based” leadership .

Sheaths are not the most obvious structures on a bamboo plant, but they are, perhaps, the most complicated. As the bamboo shoot breaks through the earth’s surface and reaches for the sun, it is covered and protected by a set of distinctive sheaths. Every soft and vulnerable emerging node of rhizome (root), culm, or branch bears a sheath that protects it during growth until it hardens. The outer surface of the culm sheath is usually tough while the inner surface is always smooth and glossy which allows the internode to rise rapidly through its casing. Similarly, upon crafting the culture and creating the context for resilient growth, sheath leaders play the role of protecting emerging nodes of innovation at the periphery from harm. An illuminating example would be how Singapore’s founding Prime Minister Lee Kuan Yew cleared the political obstacles and laid the ground to allow for the innovations devised by his key economic architect Dr. Goh Keng Swee to be implemented, as commented by Lee himself in his eulogy for Goh on 23 May 2010: “He [Goh Keng Swee] was my trouble-shooter. I settled the political conditions so that his tough policies we together formulated could be executed.”

Like its tough outer surface, sheath leaders are brutally honest in recognizing a problem rather than to pretend there is none. Without gratitude, honesty cannot be brought out meaningfully, since gratitude is the ability to see value even in humble, unremarkable and problematic situations as areas to improve through providing his or her service. Gratitude is antiheroic. It does not depend on courage or strength or talent. It is based on our incompleteness and born only where solidarity and the awareness of problems are present. If we are honest and do not hide it from ourselves, we can proactively work to receive the goodness and opportunities that life offers us and we can be grateful.

With its smooth inner surface, sheath leaders are able to weave diverse networks and groups who might otherwise be excluded into a coherent whole, quite unlike the typical command-and-control “position/title-based” leadership Sheath leaders are able to give voice to the unpopular, unconventional, unorthodox views to foster innovation.

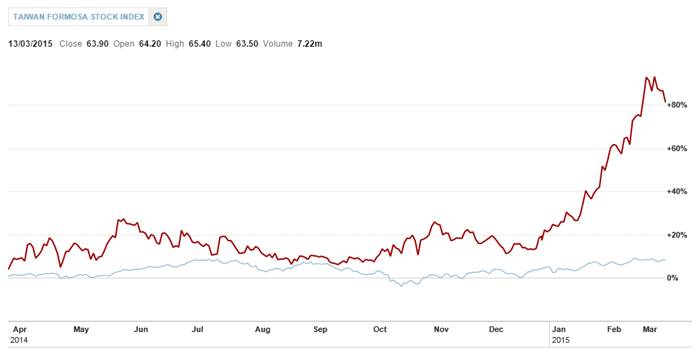

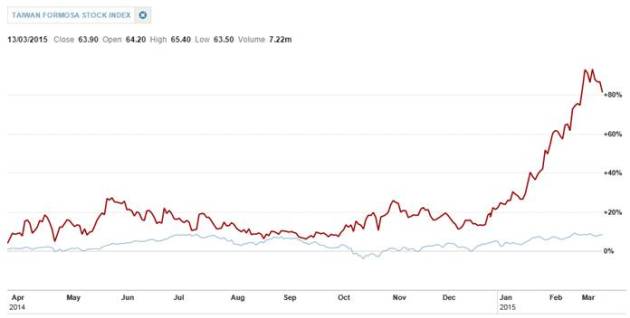

With this understanding of Sheath leadership in the Bamboo Innovator framework, we like to briefly discuss about Taiwan Paiho (TWSE: 9938 TT) which is up 80% since we highlighted the company in our Monthly Moat report in March 2014. Paiho is the world’s largest touch fastener tape maker (1.3m km/yr, >10% market share) with applications in apparel, shoes, diapers, car seats etc. All top 20 global athletic shoe brands, including Nike, Adidas, Reebok, Sketchers, UnderArmor are customers whom Paiho has forged long-term “spec-in” partnerships with.

Taiwan Paiho (TWSE: 9938 TT) – Stock Price Performance Vs Taiwan Formosa Stock Index

What struck us was how Paiho founder and CEO Vergil Cheng tried to cultivate a sustainable culture of innovation by giving voice to diverse views so that everyone are co-creators in the value creation process rather than just a few dealmakers/rainmakers or the emperor himself, the same mindset as Pixar’s Ed Catmull:

“The importance of R&D cannot be emphasized enough; it’s akin to helping the engineers and developers to “carry books”. At Paiho, all business unit managers and supervisors and above are automatically listed as a R&D personnel and can present their idea proposal. When a R&D project requires funding and the supervisor dare not make the decision whether or not to proceed, the business owner can provide his or her opinion. The investment opinion must not be based on the general macroeconomic outlook, but whether the specific product can have a breakthrough market potential.*“

Cheng explains how innovations enabled Paiho to pursue unique opportunities to widen its economic moat:

“Winning in a price war is a transient race; continuous innovation in product quality is like a marathon and the sustainable way to win. A pair of branded sports shoe is around TWD 2,000-3,000 ($66-100). So if the tape fastener in the branded shoe is of an inferior quality, the customer will scold the brand owner and not the fastener supplier. So the brand owner will be very strict in selecting the best supplier and not go for the lowest price supplier. Paiho is one of the rare few Taiwan and even Asian shoe materials company with proven R&D capabilities and is involved in the design stage with the client before the new product is launched. Our “spec-in” long-term partnerships with all the top 20 athletic sports shoe companies develop new materials/designs and provide better and patented solutions to avoid price competition and maintain stable margin. We send 8,000 pieces of sample products to our clients for them to do their trial tests. Only by doing co-R&D work with the world’s best brands and growing together with them can we provide the best customer service and solution, to master and even lead the industry trend. Our comprehensive product range is also protected by over 110 patents. Some of these patented innovations include our water-resistant tape fastener which can maintain its ‘stickiness’ in the water and is designed for water sports activities.*”

We particularly like a profound quote by Pixar’s Ed Catmull:

“Imagine an old, heavy suitcase whose well-worn handles are hanging by a few threads. The handle is “Trust the Process” or “Story is King” – a pithy statement that seems, on the face of it, to stand for so much more. The suitcase represents all that has gone into the formation of the phrases: the experience, the deep wisdom, the truths that emerge from struggle. Too often, we grab the handle and – without realizing it – walk off without the suitcase. What’s more, we don’t even think about what we’ve left behind. After all, the handle is so much easier to carry around than the suitcase.”

We think that there are many thoughts and statements about how Asia needs to be more entrepreneurial and innovative, akin to Ed Catmull’s “handle” trying to lift up the old, heavy suitcase of Asia. Unless one has a R.E.S.-ilience handle and framework to carry this suitcase, it will be difficult to invest in the emerging tycoons, the innovators and the wide moats they are building, like Taiwan Paiho and Vergil Cheng – before they become obvious – and uncover the hidden wealth inside during this critical transition period and in the coming decades ahead.

*Chinese to English translation by KB Kee. Any translation errors are KB’s.

Warm regards,

KB

The Moat Report Asia

www.moatreport.com

http://accountancy.smu.edu.sg/faculty/profile/108141/KEE-Koon-Boon

A new monthly issue of The Moat Report Asia is now available!

Access the in-depth idea presentation:

http://www.moatreport.com/members/ |