Activist Investors Gain in M&A Push; Shareholders Make Their Power Felt; Firms Review Operations, Make Pre-Emptive Moves

January 8, 2014 Leave a comment

Activist Investors Gain in M&A Push

Shareholders Make Their Power Felt; Firms Review Operations, Make Pre-Emptive Moves

DANA MATTIOLI and DANA CIMILLUCA

Updated Jan. 5, 2014 8:57 p.m. ET

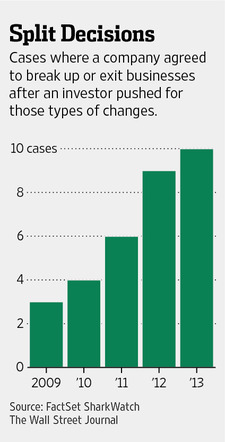

In a lackluster spell for mergers and acquisitions, activist investors have been a rare bright spot.![]() Aggressive investors including Elliott Management and Barington Capital Group LP were a driving force behind a number of deals at big companies in 2013. According to FactSet SharkWatch, there were 10 instances in 2013 in which a U.S. company agreed to break itself up or sell or exit businesses after an investor pushed it to make such changes, even if the moves didn’t always satisfy the activist.That is the highest such number in the five years covered by the corporate-activism database. In 2009, there were only threeinstances.

Aggressive investors including Elliott Management and Barington Capital Group LP were a driving force behind a number of deals at big companies in 2013. According to FactSet SharkWatch, there were 10 instances in 2013 in which a U.S. company agreed to break itself up or sell or exit businesses after an investor pushed it to make such changes, even if the moves didn’t always satisfy the activist.That is the highest such number in the five years covered by the corporate-activism database. In 2009, there were only threeinstances.

Deutsche Bank investment-banking honcho Paul Stefanick discusses the highs and lows of dealmaking in 2013 with WSJ’s Dana Cimilluca.

Although the absolute number of corporate sales and spinoffs sparked by activists is small compared with the thousands of M&A deals that take place every year, the power of these shareholders is being felt across the corporate world as companies launch reviews of their operations and, in some cases, make pre-emptive moves.

Shareholder activism has “had a profound impact in boardrooms across the country,” said Peter Tague, Citigroup Inc. C +1.42% ‘s co-head of global M&A.

In some cases, shareholderactivists are targeting household names. In March, oil company HessCorp. HES -1.02% , said it would shed a number of units. The announcement came roughly two months after Elliott bought a 4%-plus stake in Hess and began pushing it to sell assets and make other changes.

A representative for Hess, which has a market value approaching $30 billion, declined to comment. Elliott Management declined to comment.

Darden Restaurants Inc., DRI -1.38% with a market capitalization of about $7 billion, said last month that it would spin off or sell its Red Lobster seafood chain after Barington took a stake in the company and urged it to break up. Barington said the announced move doesn’t go far enough and another activist, Starboard Value LP, just before Christmas also disclosed a push for a broader breakup of the company.

Darden Chief Executive Officer Clarence Otis said on a conference call recently that the company had been considering moves, including a separation of Red Lobster, for a while, without saying how long.

DuPont Co. DD -0.86% , the chemical company, with a roughly $60 billion market value, in October said that it would spin off its performance-chemicals business. The move came after Trian Fund Management LP, which had accumulated a big stake in the company, privately advocated such a step, according to a person familiar with the matter.

A spokeswoman for DuPont said the spinoff is part of a broader strategic realignment that has been under way for years and isn’t a response to any individual shareholder.

Global M&A volume was $2.72 trillion in 2013, according to Dealogic, a data provider, 8.1% more than in 2012. The number of deals struck, however, dropped 15% to 36,950, while in the U.S. the decline was 19%.

In some cases, activists are succeeding in getting entire companies sold. Gardner Denver Inc. in March agreed to be bought by private-equity firm KKR KKR +0.83% & Co. for $3.7 billion, after ValueAct Capital, known lately for pushing for changes at Microsoft Corp.MSFT -1.30% , accumulated a 5.1% stake in the industrial-machinery maker and agitated for its sale.

“We wouldn’t have bought Gardner Denver had not an activist shown up,” George Roberts, KKR’s co-CEO, said at a conference last month. Gardner Denver declined to comment.

The threat that an activist shows up at a company’s doorstep has increased in recent years, as more investors are using the strategy and pursuing bigger targets. Assets under management by activist hedge funds rose more than 50% to $89.1 billion in the 12 months ended in September, compared with the same period in 2012, according to market-research firm HFR Inc.

In the past, companies often refused to engage with activists, sometimes leading to bitter public fights. But in recent years, more executives and their advisers have been receptive to opening lines of communication with activists in an effort to avoid spats.

These days, companies often take steps to avoid attracting an activist. A number of companies are analyzing their businesses and considering sales of ill-fitting or underperforming units even before an activist investor shows up on their share register, bankers said.

To be sure, activism can be a two-edged sword for deal making. One factor standing in the way of morecorporate takeovers is fear on the part of companies that such moves will draw the attention of shareholders who would rather see them slim down and narrow their focus.

SPX Corp., which itself had tried to buy Gardner Denver, attracted an investment from Relational Investors LLC after it failed to seal the deal. Relational said the company had overpaid for previous acquisitions. And Darden, when announcing its plans to shed Red Lobster, said it intends to “forgo acquisitions of additional brands for the foreseeable future.”

“Large-scale M&A runs counter to the ‘fit and focused’ theme that a lot of activists are pushing,” said Gregg Lemkau, co-head of global M&A at Goldman Sachs Group Inc.GS +1.56%

Activists would often prefer that companies use their cash to buy back shares or pay dividends rather than make acquisitions, which have a longer-term and less-certain payoff to shareholders.

Chris Ventresca, co-head of global M&A at J.P. Morgan Chase JPM +1.24% & Co., said companies are more rigorously comparing the returns on a share buyback and dividends with acquisitions. The difficulty, he said, comes when a buyback or dividend can deliver immediately for shareholders, while an acquisition could pay off more, but in the longer term.