The Chinese Emperor and His Number Two: Xi-Li Power Shift, What It Means for Value Investors and the Story of Hangzhou Robam

January 13, 2014 Leave a comment

The following article is extracted from the Bamboo Innovator Insight weekly column blog related to the context and thought leadership behind the stock idea generation process of Asian wide-moat businesses that are featured in the monthly entitled The Moat Report Asia. Fellow value investors get to go behind the scene to learn thought-provoking timely insights on key macro and industry trends in Asia, as well as benefit from the occasional discussion of potential red flags, misgovernance or fraud-detection trails ahead of time to enhance the critical-thinking skill about the myriad pitfalls of investing in Asia at the microstructure- and firm-level.

Dear Friends and All,

The Chinese Emperor and His Number Two: Xi-Li Power Shift, What It Means for Value Investors and the Story of Hangzhou Robam

Deng Xiaoping needs the number two man Zhu Rongji in China’s quest for prosperity in the 1990s as “Zhu Laoban” (朱老板, “Zhu the Boss”) pushed through wrenching state-sector reform and terrorized corrupt officials. Singapore’s Lee Kuan Yew has Goh Keng Swee, the economic architect who is said to feel depressed every time he passed by a school at the end of the school day as his thoughts were on how to find gainful employment for the school-leavers every year. The late Indonesian strongman Suharto is aided by Widjojo Nitisastro, the legendary architect of Suharto’s New Order economy. Wal-Mart is unstoppable when Sam Walton has David Glass as the key architect to implement the automated distribution vision at Wal-Mart since 1978 and is since up 1,000-fold to $250 billion in market value. Thailand’s Thaksin had Somkid Jatusripitak but the once-successful Thaksinomics ended with Somkid’s departure in 2006. The importance of a good number two man has been neglected and Thaksin’s parting shot then at the co-founder of the Thai Rak Thai Party has been predictive of his own future downfall: “Whether Somkid is in my next government or not is irrelevant to confidence in my government among business leaders. Nowadays, I am the main person who works. Everybody else in my cabinet is just my helper.”

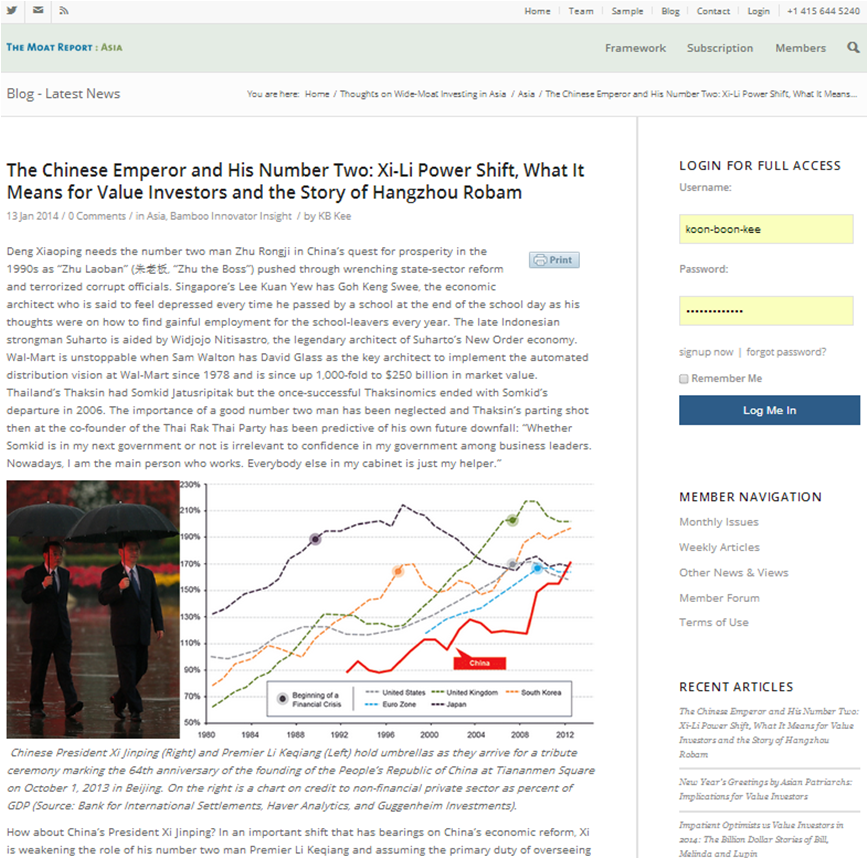

Chinese President Xi Jinping (Right) and Premier Li Keqiang (Left) hold umbrellas as they arrive for a tribute ceremony marking the 64th anniversary of the founding of the People’s Republic of China at Tiananmen Square on October 1, 2013 in Beijing. On the right is a chart on credit to non-financial private sector as percent of GDP (Source: Bank for International Settlements, Haver Analytics, and Guggenheim Investments).

How about China’s President Xi Jinping? In an important shift that has bearings on China’s economic reform, Xi is weakening the role of his number two man Premier Li Keqiang and assuming the primary duty of overseeing economic reforms, particularly after the Plenum in November 2013. “Likonomics” is replaced by “Jinpingnomics”. Xi had personally led the drafting of the Plenum economic reform plan – the first time a party chief had done so since 2000. Xi is subverting a nearly two-decade-old division of power whereby the president, who is also party chief, handles politics, diplomacy and security, while the premier manages the economy. Xi’s predecessor Hu Jintao had played a negligible role in the economy and shared power evenly with former premier Wen Jiabao who was in charge of the massive RMB4 trillion ($660 billion) stimulus plan to respond to the 2008-09 global financial crisis which led to over RMB20 trillion ($3.3 trillion) of local government debt and concerns by investors such as George Soros who wrote recently what is perceived as a prediction of an economic crash in China: “There is an unresolved self-contradiction in China’s current policies: restarting the furnaces also reignites exponential debt growth, which cannot be sustained for much longer than a couple of years.” After rapidly consolidating power over the party and the military in his first year, Xi is now stepping in on the economy, making him the most individually powerful leader since Deng who launched China’s economic liberalization in 1978. Xi is also said to want to avoid the mistake of Hu who was outshined by Wen during the ten-year Hu-Wen administration from 2002.

Interestingly, in the February and May 2011 monthly editions of On the Ground in Asia, the predecessor of the Bamboo Innovator Insight and the Moat Report Asia, we had highlighted how the weak emperors in China and Asia would attempt to consolidate and take back power from the powerful local warlords:

“Local provinces now have greater autonomy and real power and the local warlords strive to create political dynasties capable of controlling or influencing a wide range of government projects to entrench themselves. A key risk for Asia that has not been particularly publicly highlighted is that the weakened central authority, unhappy at how his power and money base is eroded by so many different local factions, attempts to first attract all the FDI and investment flows into the regions with buzz transformational projects and privatization or PPP plans, and then, after getting a critical pool of funds, “shuts down” the place partially to reallocate power and money back to the central authority. This is a potential macro risk in Asia that investors have to keep in mind.. leverage is flattened, particularly at the LGFVs (local government financing vehicles), so as to weaken the elitist grip in local provinces through controlling the finances, resulting in China taking a “big bath writedown”, contrary to market expectations of a relatively smooth economic condition.. The new (benign elitist) leader Xi Jinping can also start to quickly produce fruits on the burnt-and-fallowed grounds when he takes over to demonstrate his competence and authority.”

The Bamboo Innovator recalled when we wrote about the above opinion in early 2011, we were derided both by some external parties and even internally for being an unnecessary alarmist, especially when Asia had rebounded strongly for almost two years from the bottom in March 2009 and everyone was minting money from property, gold, commodities and so on. The local government debt risk is not something new or unexpected and is already a known risk factored into the markets, some commented. If the information is out there, someone is already worrying about it and the risk will be impounded into the prices, they added. Shanghai Composite index is down 30% since then, Hang Seng index is still slightly down, gold down 11%, while the S&P index is up nearly 40% over the same period. Yes, while the local debt risk is not new, it definitely isn’t weighted enough by the market….

<Article snipped>

… Asian patriarchs and matriarchs add value in ways that do not appear on balance-sheets through their relationship-based deal-making capabilities. These strengths and tacit knowledge are difficult to bequeath or transfer to one’s children, and these specialized and intangible assets cannot be capitalized easily in the markets. This is why some Asian empires struggle to outlive their founders and succession tended to coincide with tremendous destruction of value. Because most Asian companies are “one-man-shop” operations with the founder making all the decisions, one of our favorite due diligence questions for Asian entrepreneurs and managers: the willingness to build a culture of decentralization/ empowerment and invest in a system to cascade decision rights throughout the organization is an important signal that the founder desires and cares to scale up the company in a sustainable manner by not hoarding knowledge.

That is why the Bamboo Innovator likes to see whether the company or country has a David Glass, a Zhu Rongji. Often, in our interaction with the Asian management, we can sense whether the emperor is playing mind games on the people around him or her so as to ascertain the worthiness of the “successor”. True Asian compounders and Bamboo Innovators have no time to waste – they build an idea or a vehicle that is larger than them so that others can be co-creators and involved in the value creation process, rather than having to fight for favors and permission and engaging in time-wasting posturing acts to be perceived in a good light by the emperor. There is a palpable sense of urgency in wanting to get things done, to realize the intangible ideas and Purpose, to keep the flames burning..

To read the exclusive article in full to find out more about the implications of the Xi-Li power shift and the story of Hangzhou Robam, please visit:

- The Chinese Emperor and His Number Two: Xi-Li Power Shift, What It Means for Value Investors and the Story of Hangzhou Robam, Jan 13, 2014 (Moat Report Asia, BeyondProxy)