Beijing Tests Tools to Tackle Bad Debt; Provinces Set Up ‘Bad Banks’; Asset Exchanges Spring Up

January 12, 2014 Leave a comment

Beijing Tests Tools to Tackle Bad Debt

Provinces Set Up ‘Bad Banks’; Asset Exchanges Spring Up

DINNY MCMAHON

Updated Jan. 9, 2014 11:43 p.m. ET

China is gearing up for a spike in nonperforming loans and is experimenting with state-owned institutions that can take over bad loans. The WSJ’s Jake Lee speaks with Dinny McMahon about how Beijing is trying to combat the growing problem.BEIJING—China’s government is gearing up for a spike in nonperforming loans, endorsing a range of options to clean up the banks and experimenting with ways for lenders to squeeze value from debts gone bad.

Write-offs have multiplied in recent months. Over-the-counter asset exchanges have sprung up as a way for banks to find buyers for collateral seized from defaulting borrowers and for bad loans they want to spin off. Provinces have started setting up their own “bad banks,” state-owned institutions that can take over nonperforming loans that threaten banks’ ability to continue lending.

And several banks have tapped markets for funds via initial public offerings in recent months. Harbin Bank, named for the northeastern Chinese city, is planning to apply for a $1 billion IPO in Hong Kong this month, paving the way for a listing as soon as the second quarter, people familiar with the plans said this week.

“In recent years, Chinese banks have been exploring new avenues to resolve their bad loans,” said Bank of Tianjin, which is based in northeastern China. The lender recently listed more than 150 loans for sale on a local exchange. “We will continue to recover, write off, spin off and use other avenues in order to resolve bad loans,” it said.

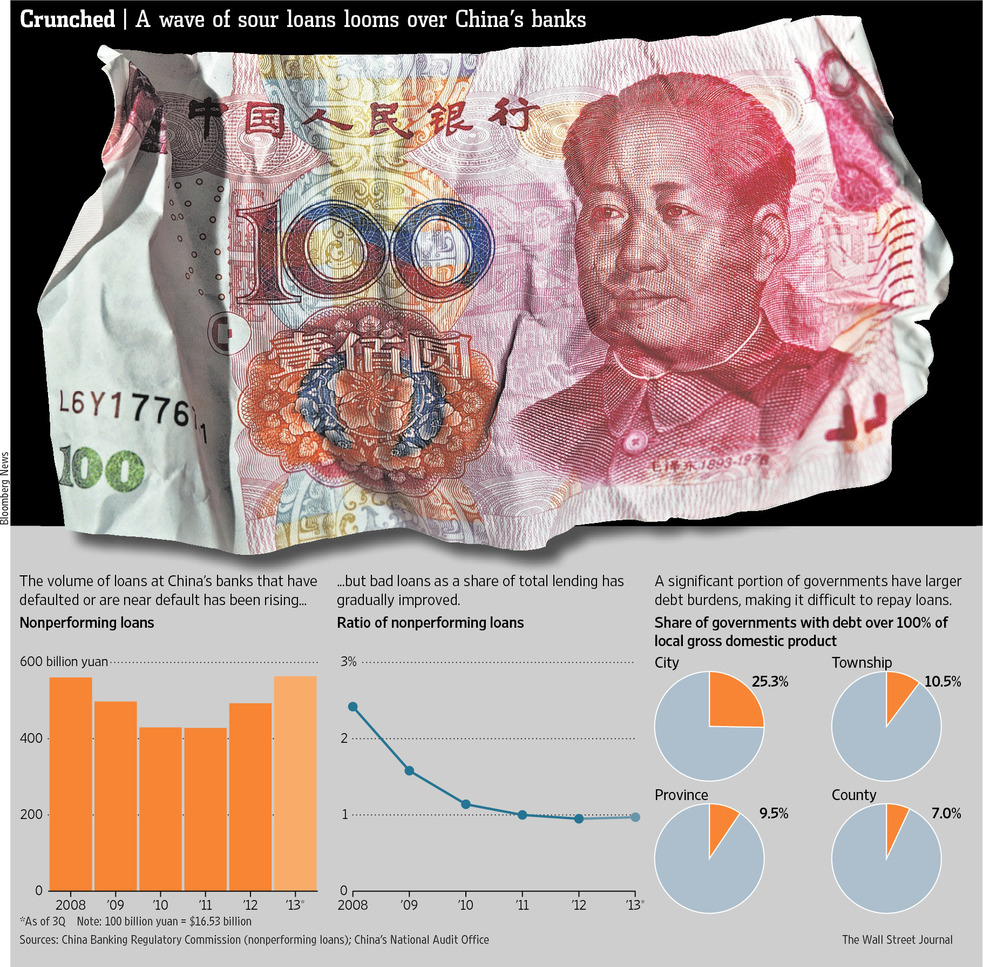

China’s banks reported 563.6 billion yuan ($93.15 billion) of nonperforming loans at the end of September. That is up 38% from 407.8 billion yuan, the low point in recent years, two years earlier.

Analysts think it is unlikely that Beijing would let major banks go bust. Still, investors suspect the cost of a cleanup could be a sizable economic burden and could become even greater if growth continues to slow.

The last time Beijing confronted bad-loan problems, in 1999 and 2000, the sums involved had crippled the banking system. Banks became far less able to make new loans, forcing the government to take action. Some 1.3 trillion yuan of bad debt was spun off the books of the biggest state banks and swept into four purpose-built bad banks.

This time, to avoid a costly bailout in the future, the government is pushing the banks to clean up their mess early. It is giving them new tools to do so: the exchanges to sell bad assets, provincial-level bad banks and permission to raise fresh capital using hybrid securities, complex products that combine aspects of debt and equity.

China Citic Bank Corp. 601998.SH -0.27% is taking the unusual step of asking shareholders for permission to write off nearly $900 million, citing a sharp rise in nonperforming loans. It said it wants to more than double the amount of loans it can write off in 2013 to 5.2 billion yuan. Analysts say other banks also increased their write-offs in 2013, but with less fanfare than Citic Bank.

Write-offs can be expensive, cutting into funds set aside to cover loan losses, or chipping away at lenders’ capital bases. Consulting firm McKinsey & Co. estimates Chinese banks will require about $320 billion in additional capital, including from bonds, hybrid securities and equity issuance, over the next five years.

In the past three months, three Chinese banks have launched IPOs in Hong Kong, the first Chinese bank listings since 2010. Another three, Guangdong-based Guangfa Bank, Bank of Shanghai and Harbin Bank, are expected to follow suit in coming months. China Cinda Asset Management Co. 1359.HK -2.92% , one of the original four bad banks, raised capital via a Hong Kong listing late last year, a move that will enable it to buy up bad loans as the supply of such debt rises. China Huarong Asset Management Co., one of its peers, is also preparing to list.

Enlarge Image

China Citic Bank wants investors to approve aggressive debt write-offs. Imaginechina/Zuma Press

Last February, the Ministry of Finance and the China Banking Regulatory Commission made way for a new safety net, letting each province set up one bad bank that would be allowed to buy large batches of loans from companies within the provincial borders. So far, Jiangsu is the only province to have set up its own bad bank, but Zhejiang and Shanghai have said they plan to.

Asset exchanges are giving commercial banks another way to find buyers for souring loans.

“Banks have asked us this year to hold large events to promote bad assets they want to transfer,” said Ding Huamei, general manager of Tianjin Financial Assets Exchange, which was set up in 2010 by China Great Wall Asset Management Corp., another of the four original bad banks, as a platform for selling bad loans and assets seized by banks. Buyers include companies, investors and some foreign firms, which bid at auction, typically by phone or electronically, he said.

Mr. Ding said about 20 exchanges around China list bad loans for sale. There is no data on the volume of nonperforming loans sold over such platforms.

Since September, more than 20 billion yuan of Agricultural Bank of China601288.SH 0.00% loans have been put up for sale on the exchanges in Tianjin, Beijing, Chongqing, and Shandong province. Much of the debt went bad before the bank’s listing in Shanghai and Hong Kong in 2010. The bank didn’t reply to a request for comment.

In November, Bank of Tianjin listed over 150 loans on the Tianjin Financial Assets Exchange. Including accrued interest and the face value of the debt, the total comes to 900.6 million yuan, slightly larger than the value of nonperforming assets on its books at the end of 2012.

A potential constraint on the bad-debt cleanup is the inexperience of buyers at pricing and dealing with distressed debt, never a significant asset class in China. Finding buyers for a failed factory or commercial property seized as collateral can be difficult, particularly in cities with weaker economies.

“There’s an immature market for collateral. So the banks’ capacity to resolve loans is more determined by the market than their own abilities,” said Simon Gleave, regional head of finance services at KPMG China.

Analysts see the bad-loan problem as a growing issue. Although figures as of the end of September indicate bad debt represents only about 1% of total loans in China’s banking system, a range of major industries are plagued with overcapacity and local governments are struggling to repay money borrowed to fund a construction binge. Investors broadly believe the actual bad-loan figure is much higher. The share prices of Chinese banks listed in Hong Kong have fallen, to trade below their book value.

“Chinese commercial banks’ asset quality will continue to deteriorate for sure,” said Hu Bin, a senior analyst at Moody’s Investors Service.