LGFV credit risk and the rate wall of China

January 12, 2014 Leave a comment

LGFV credit risk and the rate wall of China

| Jan 09 12:37 | Comment | Share

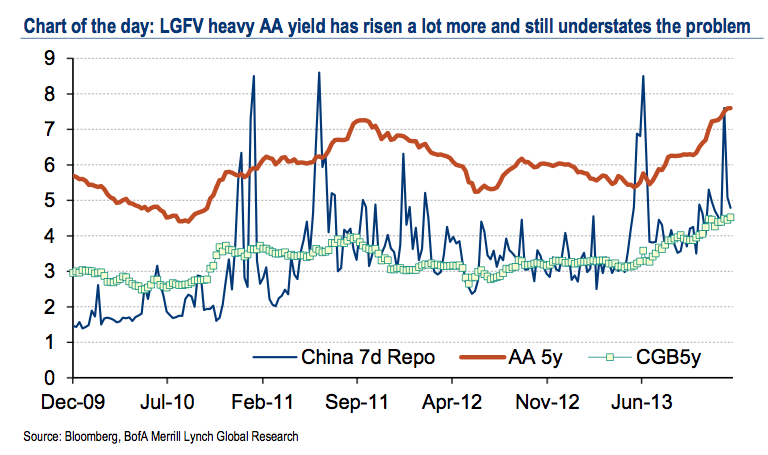

Have a chart from BofAML who, like many others, see financial conditions in China remaining tight as the PBoC tries to delever the economy and an inelastic, potentially spirally, demand for credit dominates. Basically, it shows one of the problems that occurs when interest rates are jacked-up. As we’ve written before, there’s probably a reason Chinese companies have been rushing to issue in dollars.From BofAML’s Bin Gao and Claudio Piron (our emphasis):

The trouble with higher interest rates is that a large amount of bonds are coming due for rollover. The heaviest redemption will come relatively soon in March and April of this year.Knowing the risk, the NDRC has recently issued a directive, allowing local government financing vehicles (LGFVs) to roll maturing bonds in the market.

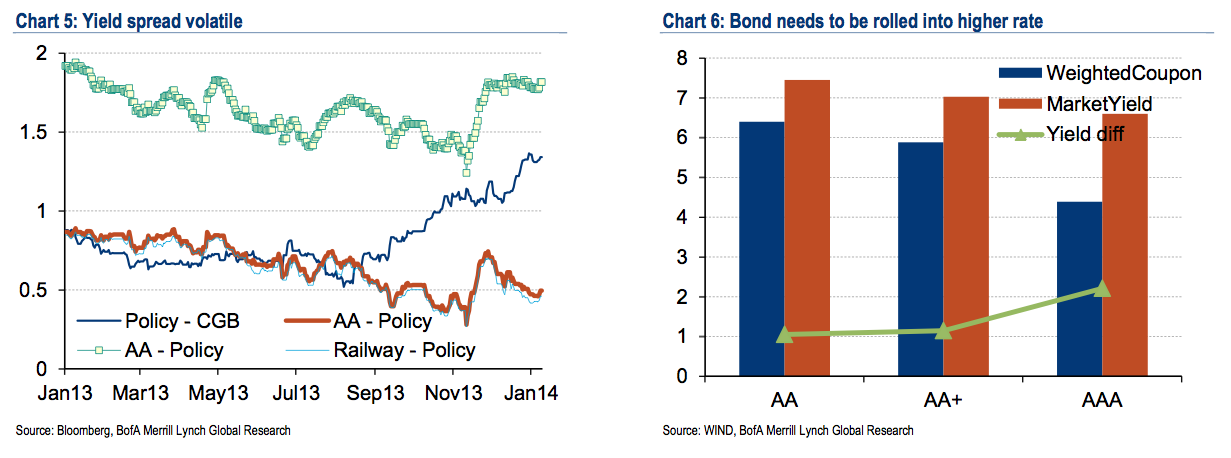

The trouble is, as the urbanization expands into third and fourth tier cities, the quality of borrower worsens even more. Looking at the LGFVs, recent borrowing have been concentrated in the AA segment, a sector whose yield has risen a lot more and has passed 2011 peak (Chart of the day). Worrying about the cost of bond roll, we examined the credit spread, yield spread between policy bank bonds and credit bonds, and argued it would widen. Since then, overall yield has moved higher and the spread has been fluctuating based on the market closes (Chart 5). Yet, the AA spread failed to narrow.

Furthermore, there are reasons to suspect that the market close for credit issues have been understating the true yield companies have to pay for bond issuance. On 8 January, the Huaihua local debt, 7y rated AA, was issued at a yield of 8.99%. On the day the market close for AA was 7.7 to 8%, depending on two different measures published by ChinaBond.

This is not an isolated case. A quick review of local debt issues shows at the current high yield level they dominate the issuance calendar, that the most common coupon was around 8.5% for AA-rated offers, suggesting much higher funding cost even before the fees. Based on the market close, the cost for more than CNY1tn credit-related issues to be rolled will increase the cost by 1% to 2%. Factoring the spread between the market yield and issuance yield, the cost could rise 1.5% to 3% (Chart 6).

Facing such exuberant costs, LGFV started looking for FX issuance. Shanghai Chengtou (上海城投) just issued its first dollar-denominated debt onshore in December, and swapped back to RMB through CCS. The cost was in mid-4%, much cheaper than the 6.25-9% rate a typical LGFV has to pay nowadays in the RMB market, depending on its credit rating. All this is good on the cost side, but it creates another problem on FX flows and could potentially further complicate the regulator’s effort in regulating FX flows and increases regulation risk.

BofAML do note the hope that the recently released draft shadow banking rules (known as Doc 107) might push money from the shadow banking segment to the bond market, leading to a bond rally. But they’re not optimistic. Significantly, Doc 107seems pretty damn weak and treats shadow banking as a healthy innovation in the economy. On top of that, the market has tried a few times in the past year to rally based on Directive #9, the seemingly more impressive predecessor to Doc 107, and was crushed each and every time. Interest rate liberalisation is going to be hard toput back in its box after all. As BofAML say:

Policymakers can help to ensure the safety and soundness of WMPs, e.g., by regulating the underlying assets; and matching the duration between assets/liabilities. But as long as the government hesitates to fold down the unsustainable projects, scaling back shadow banking activities will not reduce the overall demand for credit. Less supply from other channels and more demand through bonds could potentially drive up bond yields even higher…

The government deserves credit for trying to address the fundamental issues in the economy. But the pill addresses the symptom, not the cause. In our view, the problem is the incessant demand for credit from inefficient projects. Without proactively winding these down, borrowing will simply shift from one market to another. As the funding cost gets higher, it becomes harder and harder for these projects to sustain and the risk of default rises.

Interesting then, as Nomura’s Zhiwei Zhang points out, that China Credit Rating Company has downgraded its rating on Wuhan Urban Construction Investment & Development Co. (WUCID) to AA- from AA, according to Chinese-language 21 st Century Business Herald. It’s a pretty big beast as LGFVs go and we doubt a local government would be antagonised like this if the risk of trouble wasn’t very real:

Located in the capital city of Hubei province, WUCID is one of the largest local government financing vehicles (LGFVs) in China based on total assets and its outstanding debt level. Several factors reportedly contributed to the downgrade, including fast debt growth, a huge amount of maturing debt in the next one to two years, a shrinking bank credit line and continued large capex pressures in the future.

Moreover, the weak financing position of the Wuhan city government was also said to be one of the agency‟s concerns, as city government-incurred debt stood at RMB203.7bn, or 185.6% of its fiscal revenue, at end-June 2012. In our sample of 267 LGFVs that have disclosed financial information for Q3 2013, WUCID‟s interest-bearing debt has risen by 12.0% to RMB103.8bn from end-2012, while its growth rate ranks only at No.142 in the sample. We continue to expect some individual LGFV defaults to occur this year…

Finally, while we’re on the subject, it might be fun to ask, as Stephenson-Yang of J Capital does, what in a system in which government owns all important productive assets, whether directly or through proxies, is the difference between an LGFV and a private company that the local government has designated to develop a public works project?

The recent audit of the country’s public debt, showing that local government liabilities have risen to $3tn, up sharply over the past two years, was rather silent on the subject of corporate debt as a contingent liability…