Where the WMP things are in China; “Default probabilities from next year may rise because more and more Chinese companies depend on new borrowings to repay old debt.”

January 12, 2014 Leave a comment

David Keohane | Jan 08 09:36 | 6 comments | Share

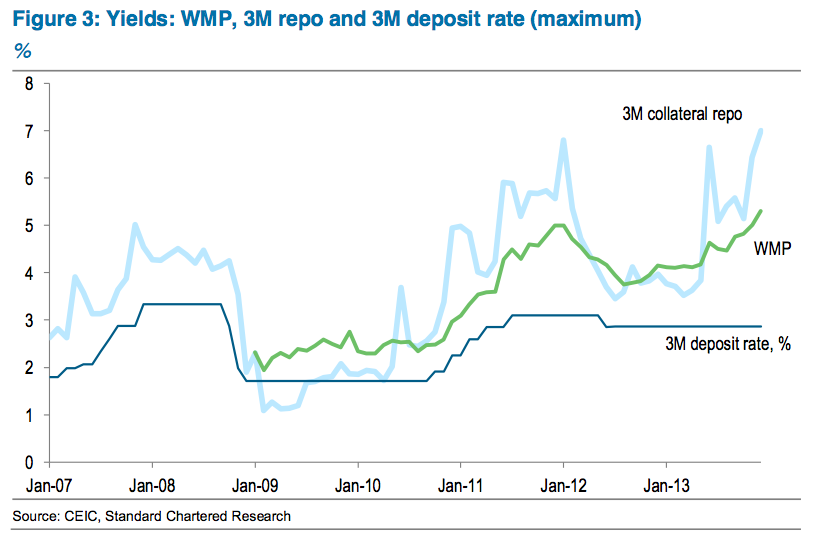

Consider this from Standard Chartered’s Stephen Green et al: [Wealth Management Products’] yields tend to move with interbank rates, since WMP funds reflect the banks’ marginal cost of funds. Current yields are well in excess of the 3M deposit rate. WMP yields also rise and fall with the interbank 3M repo rate (Figure 3). These higher WMP rates are not only attractive to households, but increasingly to corporates too – as we recently discovered, CFOs are increasingly buyers. The larger the rate differential between deposit and WMP yields, the faster the migration from deposits to WMPs, especially if chunky corporate deposits are also on the move. As a result, the current interbank tightness (owing, we believe, to a central bank anxious to begin deleveraging the economy and wanting banks to prepare for rate liberalisation) will likely result in even faster migration of funds to WMPs in H1-2014.

From where this blogger is sitting WMPs do a pretty good job of summing up the different ways of looking at what is going in China at the moment. On the one hand you have those, like Green, who see WMPs more as “off-balance-sheet deposit rate liberalisation, with a twist of risk” which are a useful tool on the liberalisation path, and on the other hand you have the Weapons of Mass Ponzi-focused brigade.

If you put more weight in the latter you will, like Anne Stevenson-Yang at J-Capital, be looking with rolled eyes at the recently released draft regulations known as Doc 107. From her good self:

The hilarious new Document 107 on shadow banking betrays how toothless the government is in the face of the mounting debt, because the only solution presented is more debt. The regulations, as reported by the Financial Times, presents shadow banking as a healthy innovation in the economy, but some shadow banks, like online Ponzi schemes, need to be “closely monitored.” The shadow of Document 9, issued last spring by a new and naïve regulator, is being politely forgotten.

But if you put more weight on the former interpretation than you are more in tune with Chinese regulators who apparently see most WMP activity as useful both for savers getting a decent return and for banks who need to get ready for interest rate liberalisation. As BofAML put it, for example:

…the recent rise in interbank rates and bond yields was mainly due to the bottom-up interest rate liberalization by financial institutions which competed for funds by bypassing caps on deposit rates via WMPs and MMFs (see here). Put differently, we cannot simplistically call rising interbank rates and bond yields as PBoC’s tightening when China is in the midst of interest rate liberalization.

Run with that as far as you will — and how far you get will probably be a function of your faith in China’s powers that be — but it appears to be the attitude to shadow banking in China generally at the moment with, as Yang summarised above, recently released regulation saying very little about WMPs and basically giving shadow banks the thumbs up while saying they need to be “closely monitored.” This begs the question, what was the PBoC trying to achieve with the cash squeeze? The guess is that it was using market forces to do what administrative diktat has been unable to. After all, the suggestion is that the PBoC had a hand in drafting Doc 107 even if the State Council was the final author. The WSJ has a piece worth checking out and here’s what Green has to say:

We believe that one of the PBoC’s motives for driving up interbank yields in recent months has been to reduce the riskier activities in the WMP market.

In June 2013, the PBoC made its first attempt at starving the market of funding in the run-up to the quarter-end reporting day. It did not end well. We believe the PBoC deliberately starved the market of liquidity. At least one interbank debt was not repaid on time, and the freezing up of the market made international headlines. After June, the PBoC kept interbank yields relatively high. It pushed up yields again in October, this time gradually and being extra-careful to provide liquidity when needed (Figure 3) – but at a price.

We see four results of this:

An accelerated transition from deposits into WMPs, given the higher yields on offer for WMPs.

Higher interbank rates likely attracted more WMP funds into interbank deposits, possibly away from riskier loan assets.

The June liquidity crunch encouraged banks to issue slightly longer-term WMPs. One bank we spoke to in Beijing said that it was issuing more WMPs of two- to three-month tenors, and far fewer of the one- to two-week WMPs that were popular before the June crunch. This reduces the maturity mismatch, but as the bank we met acknowledged, the problem persists.

The PBoC’s action has hit banks that were using short-term funding to finance the purchase of TBRs. We note a sizeable decline in overnight clean interbank borrowing since June (Figure 15), though the much larger collateralised repo borrowing market has not shrunk in size. We will have to see the listed banks’ H2-2013 books to assess how successful the PBoC has been in discouraging the holding of TBRs.

The risks of WMPs are manifold and we’ve covered them before– potentially risky duration mismatch (borrowing very short-term against illiquid assets such as property developments); underlying assets which are almost always well-hidden from investors; vulnerable trusts, securitisation companies and asset management companies creatively channeling the funds; and no explicit backstops — but some comfort can be drawn form the reality that bankers seem to understand that they are expected to make sure their WMPs don’t go belly up. Fact is more funds flowing to them seems unavoidable if higher borrowing costs are needed to restrain credit growth. (Recently introduced negotiable certificates of deposit are indicative of a longer-term move away from them anyway, but still.)

From Green again:

A banker involved in managing his bank’s WMP business told us that if there were more than 10 client complaints about a product, a senior bank manager would have to travel to Beijing to explain to the regulator what had happened – an unpleasant experience, and one likely designed to ensure that the bank solves the problem before complaints become too loud. The implication is that despite all the attempts to persuade WMP investors that the risk is theirs, practice so far suggests that the risk is actually the banks’.

All too optimistic? No idea really but we always get edgy when whack-a-mole finance and regulation pretend to be getting along — particularly when a suggestion of real control is mooted, and even more so when credit in a very credit-needy economy is in question, and triple so when China’s second largest broker is saying things like this:

Liabilities at non-financial companies may rise to more than 150 percent of gross domestic product in 2014, raising default risks, according to Haitong Securities Co. The ratio of 139 percent at the end of 2012 was already the highest among the world’s 10 biggest economies, according to the most recent data. That compares with 108 percent in France, 103 percent in Japan and 78 percent in the U.S., figures from the Bank for International Settlements and the World Bank show.

“We are concerned that the debt snowball may get bigger and bigger and turn into a crisis,” Li Ning, a Shanghai-based bond analyst at Haitong Securities, said in an interview on Jan. 3. “Default probabilities from next year may rise because more and more Chinese companies depend on new borrowings to repay old debt.”