How Pfizer snatched defeat from victory

May 28, 2014 Leave a comment

May 23, 2014 7:39 pm

How Pfizer snatched defeat from victory

By Andrew Ward

It was a warm and sunny spring day in the craggy archipelago that guards the entrance to Gothenburg harbour but when Leif Johansson woke up at his island home on Saturday, April 26 with the weekend ahead of him, any hopes of relaxation were extinguished by an email waiting in his inbox.

The message came from Ian Read, chairman and chief executive of Pfizer, the US drugmaker, asking Mr Johansson to be available for a phone call that afternoon.

The Swedish chairman of AstraZeneca understood he was about to be thrust into the biggest takeover battle of his long business career. Five months earlier, Pfizer had sounded out its UK rival about a deal but preliminary talks went nowhere. Now, it was clear, Mr Read was back.

In the four weeks since that email, the two men have wrestled for the upper hand as Pfizer tried to buy AstraZeneca in a near-£70bn deal . It was a showdown that pitted against each other not only two of the world’s largest drugmakers but some of the most powerful forces in Westminster, the City of London and Wall Street.

Pfizer had never failed a big takeover attempt. But with almost no chance of a deal before Monday’s deadline for an agreement under UK takeover rules, AstraZeneca looks set to preserve its independence. The story of how it defended itself from a $190bn US goliath, with the help of its Swedish chairman and French chief executive, is set to go down as one of the great dramas of British corporate history. Several people involved in the deal gave their account to the Financial Times on condition of anonymity.

When Mr Read first approached Mr Johansson in November, he was in a strong position. AstraZeneca’s share price, at around £35, was barely higher than it had been four years previously and sales were plunging as old drugs lost patent protection. Yet, when Pascal Soriot, AstraZeneca’s chief executive, flew with Mr Johansson to New York in January to hear Mr Read’s proposal, he had become optimistic about the company’s prospects. A range of new drugs was starting to emerge from its laboratories – chief among them a lung cancer drug, called MEDI4736, which Mr Soriot has forecast could reach annual sales of up to $6.5bn.

“Ian thought Pascal would fall into his arms when they met,” says one person close to AstraZeneca. “But Pfizer was trying to buy new Astra at an old Astra price.”

Back in London, the board rejected Pfizer’s £46.61 per share proposal and in mid-January the US group halted the private discussions. That was the end of the matter until news of the discontinued talks leaked in April. Asked by the UK Takeover Panel to clarify its position, Pfizer insisted it was not working on a new approach.

Yet, six days later, Mr Read sent his email to Mr Johansson renewing Pfizer’s interest. When the pair spoke, the Pfizer chief urged his counterpart to enter friendly negotiations. With no promise of an improved offer, Mr Johansson said there was nothing further to discuss.

On Monday morning, Pfizer went public with its interest, triggering the start of a 30-day window for it to agree a deal or walk away. It was the first big test of the so-called “put up or shut up rule” introduced in 2010 in the wake of Kraft’s protracted £10bn takeover of Cadbury. Now, a pillar of the UK corporate sector had once again become the target of a US suitor. Only this time Pfizer had to move fast to catch its prey.

For AstraZeneca, Pfizer’s about-turn created a sense of mistrust that only deepened during the brinkmanship that followed. “They never really tried to seduce us,” said one person close to the situation. “This was coercive from the beginning – the big US corporation that always gets its way.”

At this stage, one person close to AstraZeneca put its chances of remaining independent at less than 10 per cent. Prospects were not helped by the fact Mr Soriot was stranded in Australia visiting family when Pfizer made its approach, leaving Mr Johansson to orchestrate the defence, flanked by advisers Goldman Sachs, Morgan Stanley, Robey Warshaw and Evercore Partners, from its Paddington headquarters without him.

When Mr Read flew into London on April 29 to lobby for support from investors and reassure ministers over jobs, the sense of inevitability hardened. Then, the momentum shifted.

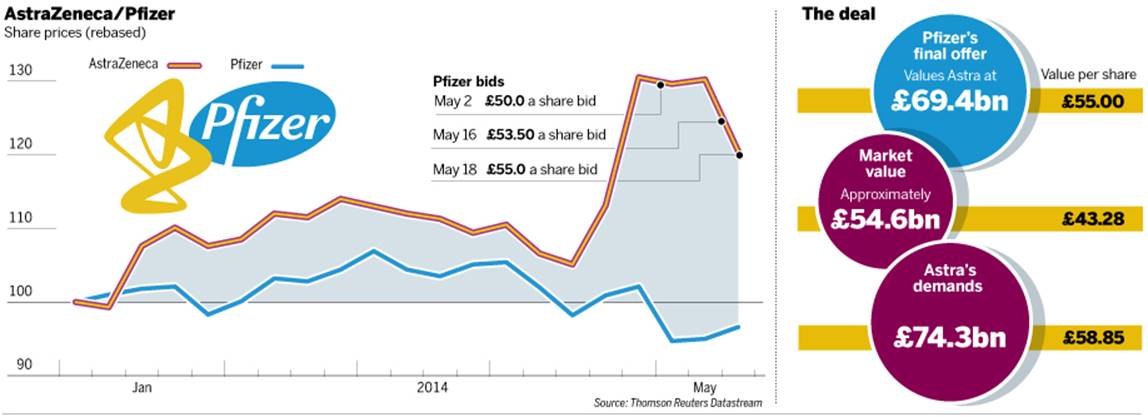

On May 2, Pfizer lodged a sweetened offer of £50-per-share, which AstraZeneca’s board again rebuffed as inadequate. Published alongside the revised offer was a letter to David Cameron, UK prime minister, in which Mr Read made a series of commitments on UK jobs, including a promise to keep 20 per cent of the merged group’s research and development workforce in the country for at least five years after any deal. It was intended to quell political concerns that the takeover would impact Britain’s life science sector. In fact, it had the opposite effect.

Downing Street had initially given a cautiously positive response to the proposed deal. George Osborne, chancellor, in particular, readily bought into Pfizer’s argument that it had been drawn to the UK by the government’s pro-business policies – including a generous tax break on intellectual property.

But Mr Read’s letter created the impression of a cosy deal with the government, even as AstraZeneca was trying to resist the US company’s advances. This perception was reinforced when Mr Cameron appointed two of the most senior Whitehall civil servants – Jeremy Heywood and John Kingman – to negotiate with Pfizer.

By the end of the week, Ed Miliband, leader of the opposition Labour party, was accusing Mr Cameron of acting as a “cheerleader” for Pfizer. At the heart of the political battle was a proxy war between two of the best-connected men in London. Pfizer’s initial advantage appeared to vindicate its decision to hire Sir Alan Parker’s Brunswick PR agency, drawing on its founder’s close ties to government, including a personal friendship with Mr Cameron.

But AstraZeneca had its own Svengali in the form of Roland Rudd, founder of Brunswick’s arch-rival, Finsbury. Mr Rudd was to be a leading figure in what company insiders dubbed the “Defence Committee”. As Downing Street came under pressure from Labour, Mr Rudd arranged a 15-minute call between Mr Johansson and the prime minister to urge the government not to take sides. Within hours of the conversation, Mr Cameron had signalled a change of tone by declaring AstraZeneca “a great British company”.

Meanwhile, the UK scientific community was swinging behind AstraZeneca over Pfizer’s record of cuts. “You can’t underestimate how much Sandwich had soured opinion,” says a senior figure at a UK scientific institution, referring to Pfizer’s partial closure of a big R&D centre in Kent two years earlier. “Mistrust of Pfizer runs deep.”

As momentum turned in its favour, AstraZeneca went on the offensive, announcing aggressive growth targets that promised a 75 per cent increase in revenues over the next decade as new drugs reach market. People close to the company acknowledge Mr Soriot now faces a stiff challenge to meet them. But the forecasts trumpeted AstraZeneca’s confidence and made clear Pfizer would have to come back with a much-sweetened offer.

Mr Read, meanwhile, was back in London to face questioning from two UK parliamentary committees. The lawmakers did not warm to the 36-year Pfizer veteran whose mid-Atlantic accent betrays only the faintest hint of his Scottish origins. Their jabs failed to cause any serious damage and, after further encouraging meetings with shareholders who said they were open to a deal, Mr Read flew back across the Atlantic on May 15 feeling cautiously optimistic he had weathered the storm.

Next day, Mr Read sent a letter to Mr Johansson with an improved £53.50-per-share offer. As AstraZeneca’s board, including former Barclays boss John Varley and Shriti Vadera, the former business minister, gathered at the Fleet Street headquarters of Freshfields, the company’s legal adviser, they sensed the endgame was near – but even they were surprised how quickly it came. Mr Johansson called Mr Read to inform him the price was still too low but he was ready to talk. A conference call was arranged for 3pm on Sunday.

They never really tried to seduce us. This was coercive from the beginning – the big US corporation that always gets its way

– Person close to the situation

AstraZeneca says it lasted two hours; Pfizer’s allies say it was less than one. Both agree it did not go well. Mr Johansson and Mr Soriot kept bringing the conversation back to concerns over execution risks – particularly their fear that Pfizer’s plan to split up AstraZeneca’s businesses would disrupt drug development. Mr Read made clear they could not reach the £59 price indicated by Mr Johansson as the level at which the board would consider a recommendation.

The call ended in deadlock and AstraZeneca’s board swiftly convened to formally reject the £53.50 proposal. Later that evening, with Mr Johansson and his team back at their homes and hotels, Pfizer went public with a new £55 offer. Not for the first time, Mr Read had taken them by surprise. By declaring the proposal “final”, Pfizer would not be allowed to increase the offer.

Some of AstraZeneca’s directors and bankers returned to Freshfields with others joining by conference call. By midnight they had decided on rejection. Executives and lawyers stayed up until 2am drafting the press release that would all but bring an end to Pfizer’s pursuit and spelt defeat for its investment bankers, JPMorgan, Bank of America Merrill Lynch and Guggenheim Partners.

In the days that followed, the US company tried its best to stir rebellion among shareholders who were unhappy AstraZeneca had rejected the final offer so quickly and without consulting investors. But people close to the UK company say Mr Read only has himself to blame for declaring the offer final, indicating Mr Johansson had been prepared for more talks to try narrowing the valuation gap.

“Pfizer managed to snatch defeat from the jaws of victory,” says one senior executive at a big AstraZeneca shareholder. For their part, Pfizer’s allies say it was clear all along that Mr Johansson did not want to seriously engage. As one says: “You can only have the door slammed in your face so many times in 28 days.”