Eating Out with Warren Buffett at Asia’s Wide-Moat Restaurant Innovators – Bamboo Innovator Weekly Insight (Issue 86)

June 8, 2015 1 Comment

| “Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | June 8, 2015 |

Bamboo Innovator Insight (Issue 86)

|

| Dear Friends,

Eating Out with Warren Buffett at Asia’s Wide-Moat Restaurant Innovators “If you have an enemy, wish upon them a restaurant.” – An old Chinese curse “…the more important point even, is that 3G – they’re not buying things to sell. And the other private equity firms.. buy companies with the idea of either IPO-ing them or selling them to competitors, or selling them to another private equity firm. That is not 3G’s strategy. They bought Burger King which is now Restaurant Brands International. They bought that to keep.” – Buffett in a CNBC interview. In a Berkshire Hathaway (BRK/A) news release dated December 12, 2014, Berkshire revealed that it currently owns 4.18% of the common shares of Restaurant Brands International (QSR), the new parent for Burger King and Tim Hortons fast-food chains. Berkshire also holds $3bn of preferred shares in Restaurant Brands that earns 9% annual interest. Warren Buffett has defied this old Chinese curse of restaurant business only rarely in his illustrious investments career. While restaurant chains have been a favorite target for value investors and private equity firms, because their cash-flow makes financing deals easy and brands can benefit from cost-cutting, the business dynamics of a restaurant business is characterized by challenges that makes them “a business that becomes harder as it grows bigger” and over 6 to 8 new restaurants out of 10 fail in the initial years. The deep-seated challenges surface in the form of (1) high fixed costs in operations; (2) the struggle to maintain consistent quality, uniqueness and experience in food and service at the individual outlets as it scales up in expansion – and one bad experience can eradicate three or four great customer experiences; (3) availability of suitable locations; (4) being held hostage by the key personnel that include the chef and restaurant manager and high employee turnover; and (5) low barriers-to-entry with little or no economic moat. The deep thoughts behind Buffett’s restaurant investments hold important lessons for value investors to uncover inspiring innovators in the restaurant business in Asia. With Buffett’s wisdom, we will better understand the story of how an electrical engineer-turned-billionaire restaurant-prenuer has been able to build a wide-moat in his restaurant chain known for its “dancing staff”, tech innovations and whose market value compounded to $1.47bn in market value after growing from only one outlet prior to 1984 to over 550 restaurants throughout Asia. However, such positive investment success stories in the restaurant business are uncommon. After all, Yum! Brands (YUM) had to write off $361m in goodwill in Feb 2015 related to the ever shrinking value of the company’s 2012 purchase of Little Sheep Mongolian Hot Pot for $860m from private equity firm 3i, following an earlier impairment charge of $258m in 3Q13. In Mar 2015, CVC Capital had to freeze the assets of the flamboyant Chinese restaurant owner Zhang Lan who sold sold a majority stake in her company South Beauty to the European private equity group last year for $300m, due to accounting tunnelling fraud. In India, there are private equity investment failures in Nirula’s, once the sole symbol of fast food in Delhi, south-Indian food chain Sagar Ratna Restaurant, Bangalore-based food chain Vasudev Adiga, etc. But first, let’s understand Buffett’s previous restaurant investment 14 years ago before his recent deal in Restaurant Brands International (QSR), the new parent for Burger King and Tim Horton’s fast-food chains. In 2001, Buffett bought 1.9m shares in OSI Restaurant Partners, owner of Outback Steakhouse, for $48m at around $25 per share. By 4Q06, Buffett completely sold his stake when OSI announced in Nov 2006 that it will be acquired by Bain Capital Partners for $3.18bn with the assumption of $185m in debt, or $40 per share, a 27% premium over its last traded price before the deal. In its final fiscal year (2006) as a public company, its operating profit was $152.3m. In 2008, revenue and profits declined and Bain was forced to take a goodwill impairment charge of $726m, an indication that it had seriously overpaid for Outback and the rest of OSI’s restaurant concepts. Prior to the acquisition, OSI’s debt was less than $200m, and its annual interest expense was just under $15m. After the takeover, debt was $2.6bn with $136m in interest, topping out in 2008 at $197m. OSI was relisted as Bloomin’ Brands Inc (BLMN) in Aug 2012 and it had managed to reduce its debt to $1.8bn and an annual interest bill of $83m. Its present market value at $2.7bn is still below the $3bn valuation nearly nine years when it was taken private. Interestingly, Buffalo’s Wild Wings (BWLD) is up more than 13-fold since its 2004 listing to a market cap of $2.9bn. OSI is part of the two big waves of PE acquisitions in the restaurant industry in 2005-2006 and 2010-2011. Since 2005, over $21bn in transactions has been recorded. Despite their average EV/EBITDA at acquisition at the decently attractive level of around 7.4x, many have failed and entered into Chapter 11, including Charlie Brown’s, Uno Chicago Grill, Sbarro’s, Bugaboo Creek, etc. OSI former staff and early leaders who inspired Outback commented how with the new private equity owners, the people-first attitude has left and been replaced by a devotion to profits. What could have attracted Buffett to OSI beyond the financial numbers? Or put in another way, why is Outback able to build a wide-moat in its business model when the general restaurant business has little or no economic moat?

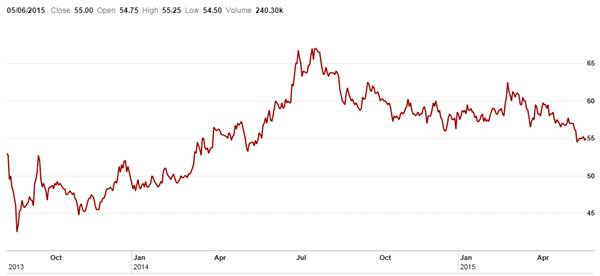

Outback Steakhouse began as one restaurant in 1988. The founders were two corporate guys and two art majors, Chris Sullivan, Trudy Cooper, Bob Basham and Tim Gannon (photo on left), who established the company because they felt they were not treated fairly by their former employee, Pillsbury, after helping the company grow the Bennigan’s chain. The founders resolve that if they were ever to own a business, they would never make anyone feel the way they were made to feel – underappreciated and under-rewarded. This was the underlying motivation behind the unique Outback ownership structure, which requires each restaurant manager invest $25,000 in his or her restaurant in exchange for a 10% ownership stake. Outback’s original reason was to create a company that did not take advantage of its employees but that shared the benefits of success with those who make it happen. The Outback’s founders understood people. They knew that (1) People want to be part of something that they can believe in and be proud of, (2) People want to be respected, treated fairly, recognized, and have the opportunity to advance, (3) People want to have control over their destiny. Outback’s owners believed in decentralized management. “We’ve been in their shoes. We’ve worked for companies and said, “If you guys would just leave us alone and let us do our jobs, we would be so much more efficient.” Each restaurant is a separate entity owned by Outback, a regional partner, and the restaurant’s general manager. Ownership means actual equity ownership – sharing in the annual profits and building equity under a buyout formula of 5x the last 2 years’ average annual cashflow. Other store personnel share in a bonus system on a quarterly and annual basis. People can see career paths and actual ownership at Outback, where the founders take great pride in the fact that they have created more millionaires than any other restaurant company. Every restaurant manager, JV or regional partner, and in some cases, chefs, too, are required to invest $25,000 to $50,000 cash for a 6 to 10% ownership interest in the restaurant depending on the concept. Store managers then are paid a base salary, and they receive stock options and 10% of the restaurant’s profits. They have a 5-year employment agreement and at the end of 5 years, they can resign or sell back their ownership interest based on a formula of 5 times the average cashflow for the last two years. Most managers who work at Outback for 10 years become millionaires. They also care about their restaurant, act like owners (because they are), and are able to engage their employees. Interestingly, Outback has no HR department. In addition, each restaurant has a profit-sharing program for waiters, waitresses, hosts and hostesses that is paid out quarterly. In addition, the company took steps to maintain positive working conditions for its employees, so that they would provide cheerful service to the restaurant’s patrons. “If you worry about your employees and their environment and their ability to do the job, and you make sure they’re happy, you don’t have to worry about the guest,” Gannon said. Accordingly, wait staff were responsible for only three tables apiece, and the company devoted 40% of the space at each location to the kitchen so food preparers would not be crowded. “We understand from having been managers, waiters, cooks, what they feel like,” Gannon said, “We know what the heat of the kitchen is like — personally.” Outback’s attractive arrangements for restaurant general managers and staff resulted in management turnover of 5% compared to 30 to 40% industrywide. So who is the wide-moat restaurant innovator in Asia that we mentioned is famous for its “dancing staff” and tech innovations? MK Restaurant Group PCL (SET: M) – Stock Price Performance 2013-2015

At family business MK Restaurants Group PCL (SET: M, MV $1.47bn), best known for its popular chain of value-for-money sukiyaki restaurants in Thailand where customers cook their food in hotpots at their tables, managing director Rit Thirakomen explained that the “MK dance” began within the company, as staff were asked to dance after arriving at their restaurants early in the morning, before they began serving customers. The original objective was to create an opportunity for restaurant managers to talk to their staff each day as a means of solving or pre-empting problems. It also helped to “energise” sleepy staff members. The MK dancing also helped staff to overcome shyness and work as a united group. Some diners have found it such fun that they have even formed a club to occasionally join in dancing with the MK staff. MK branches now have dancing shows for customers at noon and in the evening.

MK Restaurants has been investing in IT every year for almost a decade. Before the advent of iPad, MK had invested in personal digital assistant (PDA)-based ordering system in 2004, with the aim to improve service time in food ordering. Many people questioned the investment. Not only was the system able to save operating costs and time spent in serving customers, thereby freeing up tables more rapidly, but also a lot of customer satisfaction was created. The investment outlay would be returned in only two years and MK was able to satisfy even more customers. The restaurant chain also invested in GPS installed in all of its trucks to improve its logistics management and save on fuel costs. Khun Rit also planned to enhance the good relationship between MK Restaurants and its customers by issuing RFID-based member cards. In this way, existing customers will immediately be recognised in any branch and details revealed such as their favourite dishes. “With the smarter member cards, we will be able to treat our regular customers with the same standard of service as soon as they come in, even at different branches.” An engineer by education, Khun Rit said he preferred systematic methods rather than solving problems case by case. “From a small restaurant growing into over 500 branches, our target has always been to create customer satisfaction. Every customer must feel happy when they visit our restaurants. We don’t overlook even the smallest details. At MK, we design everything – from the smallest to the biggest matters,” Khun Rit explained. In paying attention to the smallest details, MK believes that most problems represent “the tip of the iceberg” and there is a need to discover the real causes. Some examples of MK’s attention to details incorporated into “MK designs” from design of services and extended into recruitment, training, motivation, the organisation’s culture, customer feedback, quality auditing and strategy alignment:

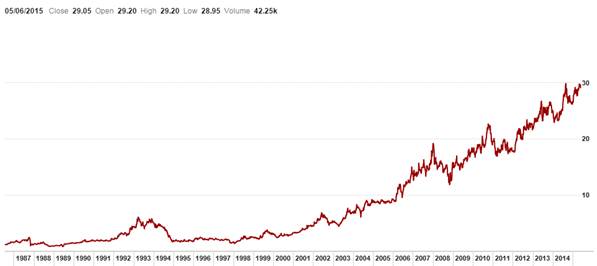

<ARTICLE SNIPPED> Employees work hard for companies where they believe they have a future and where they can have an impact. In the case at OSI, when they see that current top managers started out where they are now, as line employees, a powerful, self-reinforcing system is created. But the attitude and resulting behavior of top management is key. Humbleness is mission-critical. Top managers who have a sense of entitlement or superiority generally do not fit at high-growth companies, where humility is more important than status. Top management receives few perks at these companies. Except for compensation, the companies try to eliminate elitist executive perks. Like Buffett, the authentic value investors go beyond quant screens, checklists and financial numbers to understand the underlying business model dynamics that in turn is influenced by the motivation and character of the entrepreneurs and owner-managers. Just as OSI founders were influenced deeply by their experience of unfair treatment at their former employers and wanted to make things right by building an owner-manager environment, MK’s Khun Rit was shaped profoundly by his childhood experience which led him to found his first company called SE Education (SET: SEED). Khun Rit reminisced: “When I was a child, Thailand was still poor. The people were less educated, with no opportunities for them to receive a good education. I was hoping to see everybody allowed to receive a good education. I successfully entered the engineering faculty of the prestigious Chulalongkorn University. Because my long-cherished desire to receive a good education was achieved, I studied even harder at the university. I also helped my friends from time to time by translating their materials into English for them. Many of them were poor at English, so I helped them. This experience led me to establish a company for publishing and selling books. That is the company now called Se-Education. Our company has 300 branches across the country. I launched this company with a few classmates who graduated from the university along with me. This was an achievement of my childhood dream. As the company expanded, my life became gradually wealthy. This made me feel happy about the fact that we are providing less-educated people opportunities to cultivate themselves.” Besides MK as the role model of a wide-moat innovator in the casual-dining space in Asia, there are two wide-moat innovators in the quick-serve segment: Café de Coral (341 HK, $2.2bn) and… <ARTICLE SNIPPED> Café de Coral (341 HK) – Stock Price Performance 1986-2015

“Both Shin and KS were inspired by the idea larger than oneself: to bring about kindness and betterment to children and people in ruined lands through food technology and quality products and services. This larger idea has galvanized the trust and support among the community of customers, business partners and suppliers throughout the years. Whenever this core value is diluted, without the accompanying culture of trust and decentralization to empower the people in the pursuit of growth, globalization, size and diversification, chinks in the mighty armour start to appear and can deteriorate quickly into major problems that would bring down the organization.” <ARTICLE SNIPPED> Finally, to the next generation of leaders, MK’s Khun Rit offered the following viewpoint: “Study hard and find what you want to do in life, something you feel passionate about. These cannot be found unless you look for them seriously. If you can find a career that you really aspired to, this should be better than anything else. We are like artists who try to create good works but returning to them again and again and improving them little by little. A beautiful work can be created with a repetition of very careful, not hasty, finishing touches. Entrepreneurs need to have passion in what they are doing and a strong belief that other people will have the same passion for the products and services they deliver.”

What unites the original OSI, MK, Café de Coral and… is a sense of mission towards their customers and the people around them which inspires the extra level of intensity and dedication for them, forged by enduring dimensions as character, values, beliefs, capabilities, and personality. In a business organization, these enduring characteristics are a firm’s culture – the so-called soft factors that will actually sustain it over many years and through many situations while the hard factors like financial performance all too quickly come and go. These enduring characteristics resonate like the resolute gong of the temple bell because the sound reverberates in our hearts, stirring the everlasting values that matter: Forbearance, Honor, Duty, Hardwork, Fairness, and Humility, the timeless values that epitomize the Warren Buffett and Charlie Munger way of value investing and the core values of the Bamboo Innovator that bend but never break. Thus, before you start to bite into that restaurant stock based on its seemingly attractive numbers, make sure you are able to go back to the basics to digest this: Do you assess the numbers and valuations to be backed by a wide-moat business model and an enduring corporate culture that promotes owner-operators? Is there an idea larger than oneself underlying the business model? If your answer is a resounding Yes!, then you are able to eat well – and sleep soundly. Warm regards, KB The Moat Report Asia A new monthly issue of The Moat Report Asia is now available! Access the in-depth idea presentation: http://www.moatreport.com/members/ In the month of June, we investigate the #1 ice cream and pasta maker in its domestic market in an Asian country. It is also the main supplier of buns to McDonald’s in its home market. Its high-speed bun production business has expanded to serve other quick-serve restaurants, including Wendy’s and KFC. The firm has nurtured a corporate culture and deep know-how in branding to establish an impressive track record in acquiring and turning small heritage brands into market leaders in different food and beverage categories. Its share price is down 37+% in the past year. This is despite resilient results announced in May. The company was incorporated in 1957 by a group of entrepreneurial families and is now led by an outstanding down-to-earth third-generation business leader. |