Swadeshi Innovators in Asia (Part 2): Who Is The “Precision Castparts” of Asia? – Bamboo Innovator Weekly Insight

August 17, 2015 Leave a comment

| “Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | August 17, 2015 |

Bamboo Innovator Insight (Issue 96)

|

| Dear Friends,

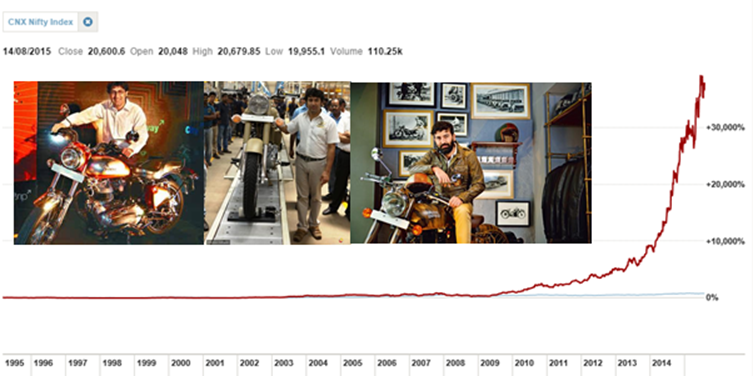

Swadeshi Innovators in Asia (Part 2): Who Is The “Precision Castparts” of Asia? “Brothers and Sisters, I would like to pose a question to my youngsters as to why.. we are forced to import even the smallest of things? My country`s youth can resolve it, they should conduct research, try to find out as to what type of items are imported by India and then each one should resolve that, through may be micro or small industries only, he would manufacture at least one such item so that we need not import the same in future. We should even advance to a situation wherein we are able to export such items. If each one of our millions of youngsters resolves to manufacture at least one such item, India can become a net exporter of goods. I, therefore, urge upon the youth, in particular our small entrepreneurs that they would never compromise.. on.. zero defect. We should manufacture goods in such a way that they carry zero defect, that our exported goods are never returned to us. If we march ahead with the dream of zero defect in the manufacturing sector then, my brothers and sisters, I am confident that we would be able to achieve our goals.” – Indian PM Modi’s at the country’s 69th Independence Day on Aug 15 “My Swadeshi chiefly centres around the handspun khaddar and extends to everything that can and is produced in India.” – M. Gandhi “Swadeshi innovators” was a term inspired by Indian PM Modi and coined by us during the last Independence Day speech in which Modi forged the “Made in India” industrial vision. The word Swadeshi derives from Sanskrit and is a sandhi or conjunction of two Sanskrit words. Swa means “self” or “own” and desh means country. Swadeshi, as a strategy, embodies the principles of self-reliance that stems from a certain deep intangible knowledge, as we have written in our Part 1 article “Swadeshi Innovators in Asia: Fluid, Fast and Nonlinear to Compound Value” on 18 Aug 2014. We commented on the rise of modern facilities in and around Pune in western India – with companies including Germany’s Volkswagen, Indian carmaker Mahindra & Mahindra (MM IN, MV $13.3bn), and autoparts maker Bharat Forge (BHFC IN, MV $2.9bn) helping turn India into a car exporting hub – suggests the industrial success is possible in parts of India. In Gurgaon and Manesar (New Gurgaon), southwest of New Delhi, this industrialization effort is led by Maruti Suzuki (MSIL IN, MV $13.2bn) and wiring harness and auto parts maker Motherson Sumi Systems (MSS IN, MV $5.1bn). Investing in listed emerging markets affiliates of MNCs has proven to be a winning strategy for shrewd long-term institutional investors such as Aberdeen. Unilever, for example, has listed affiliates in India, Indonesia and Pakistan in which it owns stakes of 37%, 85% and 75% respectively. There were 92 such companies across the emerging world, 24 of them in Asia, 46 in Emea and 22 in Latin America. Aberdeen also supported a research paper “Emerging Market Outperformance: Public-traded Affiliates of Multinational Corporations”. Yale’s finance professor Martijn Cremers found the share price performance of listed affiliates was vastly better than that of both emerging and developed markets broadly, as well as their own local markets, over the 13 years from June 1998 to June 2011. An equally weighted index of the 92 listed affiliates returned 2,229%. This compared with total returns of parents, local markets and parents’ markets of 407%, 1,157% and 147% respectively. The pattern of outperformance was consistent across regions too. Affiliates in Latin America, Emea and Asia outperformed their local indices by 41, 134 and 50 percentage points respectively. Adjusted for volatility the affiliates’ performance was even better, as many of them demonstrated defensive qualities during the 2008-09 financial crisis. In recent years since the study, there is increasing backlash against MNCs in emerging markets: from Nestle India’s poisoned Maggi noodles incident; Chinese regulators clamping down on MNCs for overcharging in price-collusion; to Korea forcing MNCs to report their detailed governance structure, business transactions and M&A deals to Korean tax authorities annually from 2017. With the backlash and the “Made In India” drive, we see the increasing localization of content driving Swadeshi Innovators in India and Asia. In Stage 1, Swadeshi Innovators have to forge tie-ups with MNCs to access technology – Maruti has rolled out India’s People’s Car in 1983 after a JV with Japan’s Suzuki Motor (TSE: 7269, MV $20.1bn). With around 40-44% market share supported by a dominant dealer service network, Maruti Suzuki today produces one passenger car every 12 seconds or 1.5 million vehicles a year. Suzuki’s 5.5% royalty stream on all Maruti sales was equivalent to a $500m annual cash dividend and is the recent target of activist investor Dan Loeb. As they grow dominant, they become more powerful than their “masters”, as evident from the split of Hero Motocorp and Honda in Dec 2010 after a 26-year JV partnership that dates back to 1984. However, it could be noted that while Hero Motorcorp survived the crisis and went on to rise around 30% after the split with its MNC partner, it underperformed the Nifty’s 75% climb over the same period. In Stage 2, Swadeshi Innovators attempt the M&A path or in-house R&D strategy to acquire technology for themselves. These include the success of Eicher Motors (NSE: EICHERMOT, MV $8.6bn) whose iconic Royal Enfield premium motorcycles contribute 40% of turnover and 80% of operating profit. Despite a five-fold increase in capacity in the last four years, the waiting period for a Royal Enfield averages between two and four months, as its distinctively-styled bikes fulfil the customer’s key aspiration of owning differentiated products at a reasonable price. Yet, Eicher group wanted to sell or shut down Royal Enfield back in 2000 due to losses and it was second-generation leader Siddhartha Lal who asked his father Vikram Lal for two years to effect a turnaround. We believe the valuation premium from the Aberdeen-style of investing in listed emerging markets affiliates of MNCs will increasing shift towards the Swadeshi Innovators and their listed affiliates. Eicher Motors (NSE: EICHERMOT) – Stock Price Performance vs Nifty index, 1995-2015

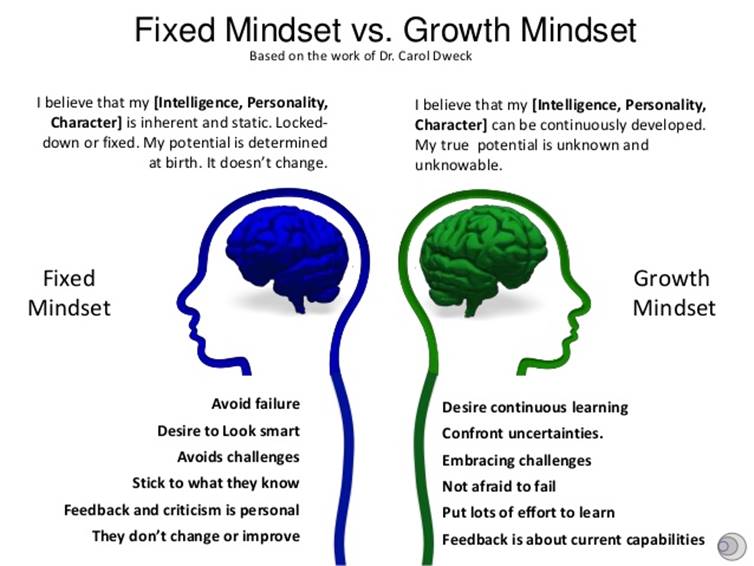

However, analyzing these innovators before they become successful is a huge problem for many value investors. Why? Consider the wisdom of Buffett’s candor who admitted in a recent CNBC interview that he had never heard of the Precision Castparts (PCP), Berkshire Hathaway’s biggest-ever acquisition deal(!), until around 3 years ago when his portfolio manager Todd Combs, who manages $9bn, invested in the company: “Three or so years ago, he added Precision to his portfolio. I had never really heard of the company before that.” Yet, PCP had been founded in 1949 and remains one of the best compounders in American capital history, up over 1,700x in three decades plus, growing from a small metal casting workshop to a global giant in aerospace and oil-and-gas components with a market cap of over $30 bn. In other words, an initial investment of $100,000 compounds to over $170 million, as highlighted in our weekly “Can Asia Produce a Precision Castparts (PCP), a 1,000X Compounder?” on Oct 2013. And Buffett has never heard of PCP until it was up over 1,700-folds. What are the important lessons does Buffett’s candor and the rise of Swadeshi Innovators in Stage 2 hold for value investors? Let’s understand a little more about why Buffett and most value investors tend to miss the PCPs, before we investigate the “PCP of Asia” and why analyzing their rise has proved more difficult unlike the Aberdeen-style of investing in listed emerging market affiliates of MNCs. <ARTICLE SNIPPED> Read more at the Moat Report Asia: http://www.moatreport.com/updates/ ******** Inspired by the work of Carol Dweck in her book “Mindsets: The New Psychology of Success” and based on our decade-plus experience of interacting with Asian entrepreneurs, we see parallels in Swadeshi Innovators as having the “growth mindset” as opposed to the “fixed mindset” of the Sexy Pretenders. A growth mindset is the awareness that painful challenges are inevitable in the journey and approaching them as a process with purposeful engagement to get better in developing one’s ability and character, rather than avoiding challenges and failure to maintain the sense of being smart or skilled. Entrepreneurs with a growth mindset understand the success is not an event-based victory based on a peak point, a punctuated moment in time, like concluding a M&A deal. Success is not merely a commitment to a goal, but to a curved-line, constant pursuit. Value investors will do well to understand the story of how entrepreneurs approach and overcome challenges that come from acquisitions or growing in-house its technological know-how. For instance, when MSS made its breakthrough acquisition in Visiocorp, the world’s largest mirror-making company with its manufacturing facilities largely in Germany, for $21m at the height of the financial crisis, turning around the firm appeared to be an impossible task and the firm was bleeding cash with sales falling off the cliff. It is to be noted that in Germany, if a business runs out of cash, the chief executive is held liable and can even be jailed. At that rather tumultuous stage, Sehgal took a decision that shocked many within the company. He decided to name the then 27-year-old son Vaaman as chief executive. “Of course we would never have allowed him to go to jail but that was the best training I could give him,” says Sehgal. “We saw things going from bad to worse,” recalls Vaaman. “First the lunch stopped, then the tea stopped and then the toilets stopped being cleaned.” For the next four years, Vaaman was put through the fire. He toured Visiocorp’s (since renamed Samvardhana Motherson Reflectec) facilities relentlessly and worked on making processes more efficient. He learnt German. He also made personal calls to his customers – Volkswagen, Audi and Porsche among others- so that orders started flowing in once automobile sales resumed. Within a year, Visiocorp was making a profit and today, it accounts for $1.3nn in sales for MSS. More importantly, with this acquisition, MSS had gained global scale, global customers and global ambition. Overall, between 2002 and 2015, MSS has made 15 acquisitions and compounded market value by over 300X to nearly $7bn. At the heart of what makes the “growth mindset” so winsome, Dweck found, is that it creates a passion for learning rather than a hunger for approval. Its hallmark is the conviction that human qualities like intelligence and creativity, and even relational capacities like love and friendship, can be cultivated through effort and deliberate practice. Not only are people with this mindset not discouraged by failure, but they don’t actually see themselves as failing in those situations — they see themselves as learning. The growth mindset leads people to more deeply engage with the limits of their skills and emotions at a particular time. We thrive, in part, when we have Purpose, when we still have more to do. Value investors will do well to sense that forward thrust, a reason and Purpose to continue making work, in order to distinguish between the Sexy Pretender opportunistically engaging in short-term financial engineering schemes that usually unwind into eventual impairment losses and the authentic Swadeshi Innovator.

Read more at the Moat Report Asia: http://www.moatreport.com/updates/ Warm regards, KB The Moat Report Asia A new monthly issue of The Moat Report Asia is now available! Access the in-depth idea presentation: http://www.moatreport.com/members/ This month of August, we highlight a listed Asian company who is the #1 functional beverage drinks company in its country with around 40% domestic market share by value and the leading functional coffee powder brand in terms of volume (#2 by value). The company is one of few Southeast Asian consumer firms who enjoy success outside of their domestic market, with overseas exports to over 60 countries contributing over 60% of total sales. The company is still in the early growth stage of deepening its channels in the overseas markets with functional beverage as the fastest growing category driving the growth of the global $200 billion nutraceuticals industry. Nutraceuticals is expected to play a central role in the frontline of the battle for consumer health with the rise in lifestyle diseases and consumers are increasingly making health-conscious choices from cutting down on carbonated soft drinks to switching to natural, organic diet. Gross margin has expanded from 30.3% in 2012 to 39.5% in 2014 with improving production efficiencies and rising higher-margin export sales. EBITDA and EBIT margins stand at 19.8% and 16.6% to generate ROE of 22.8%. The company’s high-capex era has stabilized and will enter into a bigger free cashflow and net cash position going forward. Interest-bearing debt-to-equity has dropped from 1-1.2x in 2012-13 to zero debt and net cash in 2014, with the latest net cash to book equity position at 21.7% in 1Q15, giving it a stronger position to make bolt-on acquisitions of niche nutraceutical companies, including expanding into the functional food category to strengthen its robust portfolio of functional beverage brands. The company trades at historical EV/EBIT 15.9x and EV/EBITDA 13.3x. |