Rising Strong: Lessons for Value Investors in The Turnaround Story of Bata India – Bamboo Innovator Weekly Insight

September 8, 2015 Leave a comment

| “Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | September 7, 2015 |

Bamboo Innovator Insight (Issue 99)

|

| Dear Friends,

Rising Strong: Lessons for Value Investors in The Turnaround Story of Bata India “The truth is that falling hurts. The dare is to keep being brave and feel your way back up.” – Brené Brown in Rising Strong

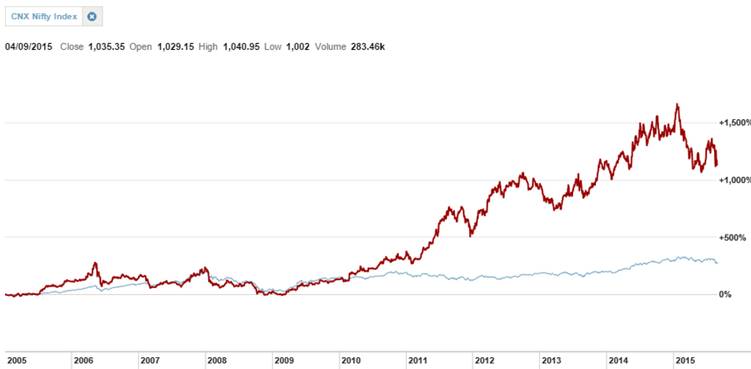

As economic conditions in China and emerging markets worsen, more Asian companies turned into the dreaded “earnings torpedo” in investors’ portfolios with weaker than expected results that led to plunges in share prices. How companies can bounce back to turnaround with sustainable performance is of paramount importance to “value investors” who tend to succumb to the disposition effect of riding losers for too long (because firm valuation metrics were thought to be getting “cheaper” as prices fell, but were in fact value traps) and selling winners too early. The turnaround story of Bata India (NSI: BATAINDIA, MV $997m) after three consecutive years of losses to generate over 1,000% returns when it regained its footings bears timeless lessons for value investors to distinguish between the alluring value traps in which the cheap gets cheaper and the sustainable turnaround story. Bata India (NSI: BATAINDIA) vs Nifty – Stock Price Performance, 2005-2015

Why is Bata India an interesting case? We have received feedback from some institutional investors about our Monthly Riddle article last week in which we investigated a listed Asian family business who is a wide-moat HVAC (heating, ventilation and air-conditioning) specialist that dominates in its domestic market and continuously innovates to “make available to the masses expensive products and services that used to be affordable by only the rich”. Our astute successful subscribers, who care very much about the knowledge and process that generates investment returns, pointed out the compounding power of investing in wide-moat companies that bring a rich man’s lifestyle, products and services affordable to the masses: Wal-Mart, Ford/Toyota, Charles Schwab, etc.

How did the Bata India management turnaround the company with key initiatives in 2005 to compound over 10-folds to a market value of nearly a billion dollars? During the initial years of Bata India in embarking the turnaround plan, many investment experts say it is a typical case of too little and too late and that the company is doomed. Understanding the fundamental dynamics and assessing the management ability of such “Rising Strong” companies in turnaround situations is important in our journeys to become better value investors. To do so requires traveling back in time to the company’s history to uncover its “Beginner’s Mindset”, which is also the underlying source of the economic moat and the origination power to overcome adversities and bounce back stronger each time round. The “complete value investor” – a term that Tren Griffin used to describe Charlie Munger in his thought-provoking book “Charlie Munger: The Complete Investor” illustrating how Buffett’s influential partner and Berkshire Hathaway’s visionary vice-chairman utilizes a set of interdisciplinary mental models to avoid the common pitfalls of bad judgment – would discover that the Bata Shoe Company faced multiple challenges and setbacks in its early days and yet it was able to rise stronger each time round. But what exactly was that origination power? It is the summer of 1895 and Tomáš Bata found himself facing financial difficulties, and debts abounded. To overcome these serious setbacks, Tomáš decided to sew shoes from canvas instead of leather. This type of shoe became very popular and helped the company to grow. Four years later, Bata installed its first steam-driven machines, beginning a period of rapid modernization. In 1904 Tomáš Baťa introduced mechanized production techniques that allowed the Bata Shoe Company to become one of the first mass producers of shoes in Europe. Its first mass product, the “Batovky,” was a leather and textile shoe for working people that was notable for its simplicity, style, light weight and affordable price. Value investors, check the box in the Mungerian mental model: does the company continuously innovate to make available to the masses expensive products and services that used to be affordable by only the rich? In the global economic slump that followed World War I, the newly created country of Czechoslovakia was particularly hard hit. With its currency devalued by 75%(!), demand for products dropped, production was cut back, and unemployment was at an all-time high. Tomáš Baťa responded to the crisis by cutting the price of Bata shoes in half. The company’s workers agreed to a temporary 40% reduction in wages; in turn, Bata provided food, clothing, and other necessities at half-price. Importantly, he also introduced the industry’s first profit sharing initiatives transforming all employees into associates with a shared interest in the company’s success (today’s equivalent of performance-based incentives and stock options). Consumer response to the price drop was dramatic. While most competitors were forced to close because of the crisis in demand between 1923 and 1925, Bata was expanding as demand for the inexpensive shoes grew rapidly. Soon Baťa found himself the fourth richest person in Czechoslovakia with his value-for-money shoe empire. In 1932, at the age of 56, Tomáš Baťa died in a plane crash during take off under bad weather conditions at Zlín Airport. Control of the company was passed to his half-brother, Jan, and his son, Thomas John Bata, who would go on to lead the company for much of the twentieth century guided by their father’s moral testament: the Bata Shoe company was to be treated not as a source of private wealth, but as a public trust, a means of improving living standards within the community and providing customers with good value for their money. Fast forward to 1973 in India. Tomáš visited India in the late 1920s to source rubber and leather for his footwear factories. He saw a number of barefoot Indians and realized there was a huge market in the subcontinent, too. The Indian shoe market in the 1930s was dominated by more expensive Japanese imports. He vowed to make affordable footwear for the masses. So the Bata shoe organization set up a factory in Konnagar, near Calcutta, in 1931, and later moved to Batanagar near Kolkata. The first India-made shoe machine was produced by Bata in 1942. In 1952 it set up one of the largest tanneries in Asia. When Bata listed stock in its India unit in 1973, it was the subcontinent’s market leader, churning out more than 40 million pairs of rubber, canvas and leather shoes and employing 22,000 people, including craftsmen, designers and chemists. The 1973 prospectus proclaimed that Bata’s mass production had brought about “a standardization in size, quality, pricing, etc., which was unique in India. Shoemaking … had become scientific, modern and sophisticated.” It even exported its shoemaking machines. The Indian market was promising. Per capita footwear consumption had soared all the way from 0.35 pairs in 1961 to 0.52 pairs in 1971. But by the 1990s, as India was finally opening up to the rest of the world, the trusty Bata brand was besieged by labor union troubles, intense competition from smaller players and a misguided strategy to offer higher-priced footwear–took a battering. Reports of nepotism and corruption were rife. Headquarters tried turnarounds to repair an image that by the early 2000s was marred by shortened store business hours (stores closed at 7 p.m. and were not open on Sundays), rude retail staff and sparse merchandising, but Indians walked away. The problems worsened with the “earnings torpedo” and three consecutive years of losses during 2002-04. Bata India now sells 50 million pairs a year and has doubled revenues in the last five years to $349m through store additions and renovations plus brand extensions to scarves, bags, sunglasses and belts. Last year it opened India’s largest–at 20,000 square feet–footwear store at Mumbai’s upscale Viviana Mall. The quality of retail ambience has upgraded; the stores now look contemporary and the product range has expanded. Bata India also has a strong distribution network with a footprint of nearly 1,300 stores across 500 cities where dealers buy from Bata on cash-and-carry basis and no inventory is owned by the company. Bata has around 8% share in the organised footwear market in India. The organised sector accounts for 30% of the total footwear industry. India is back among the top three revenue-generators for the $2.5bn-revenue Swiss parent Bata. South Asia, including India, Pakistan, Bangladesh and Sri Lanka makes up more than $600m in total revenues for Bata and accounts for more than 40% of the stores in the Bata universe. While it has 1,300 stores in India it counts up to 410 stores in Pakistan: 264 in Bangladesh and 65 in Sri Lanka. Bata India is currently 53% owned by the privately-held Swiss parent, which runs 5,000 stores across 90 countries. The founder’s grandson–Thomas George Bata–chairs the global corporation.

Spearheading the growth of Bata India is Rajeev Gopalakrishnan: ”We are making Bata young, fresh, trendy and affordable. I want Bata India to be at $1bn in revenue in the next five years”. This means a tripling in revenues, capitalizing on India’s rapidly growing middle class, the increasing number of women in the workforce and an evolving rural market. Per capita footwear expenditure is expected to go from $6.3 in 2013 to $11.6 by 2017. Bata in India now sells footwear ranging in price from $5 to $160 and Gopalakrishnan also consciously pushing it upscale–practically removing lower-end rubber slippers in favor of leather. Sports shoes is a promising niche in smaller towns, where the first-time buyer is more likely to try on a Power (Bata’s brand) rather than Nike or Adidas. Geographically, too, Bata is filling out its presence in central India after years of strength in the north and south. So what really happened in 2005 for Bata India? Small outlets and bleeding properties were closed and new remodelled large-format stores were opened. A graded choice of products was offered to diverse consumer segments. And in a major break from the past, it has extended its working hours, and stays open on Sundays. But importantly, in 2005, Bata India went back to its roots to drive entrepreneurial spirit by implementing a unique “K-Scheme”….… <ARTICLE SNIPPED> Thus, the K-Scheme fosters meritocracy and creates a strong sense of responsibility and involvement across the retail network with the performance incentive structure and career progression opportunity offered to outperforming retail employees. Bata India’s Gopalakrishnan commented: “The objective of the brand has always been to deliver the contemporary and aspirational range of products to the consumers at a high quality and affordable value. It gives us immense pleasure to welcome new consumers and loyal customers at our stores and offer an enriching experience with great customer service. We aim to deliver better than the best in future as well.” The “Rising Strong” process for value investors to evaluate the sustainability and scalability of “turnaround stocks” is illuminated by Bata’s entrepreneurial pledge: “Be courageous. The best in the world is not good enough for us. Loyalty gives us prosperity & happiness. Work is a moral necessity!” By revitalizing the entrepreneurial roots of founder Tomáš Baťa who introduced the industry’s first profit sharing initiatives transforming all employees into associates with a shared interest in the company’s success, Bata India is able to rediscover its “Beginner’s Mindset”, the origination power to stay resilient and rebound from adversities and challenges, just like the Bamboo Innovator who bend and not break, even in the wildest of storms that would snap the might resisting oak tree. PS: We also like to share with you an article “Scouring Accounting Footnotes to Prevent Tunneling” which we penned for our local newspaper Business Times Singapore that was published on 19 Aug 2015: PDF article link on SMU website Warm regards, KB The Moat Report Asia A new monthly issue of The Moat Report Asia is now available! Access the in-depth idea presentation: http://www.moatreport.com/members/ In the month of September, we investigate a listed Asian family business that has persevered for over fifty years since 1962 in this high-electricity-rates emerging country to sell something that seems risky – air-conditioners and refrigerators to consumers and commercial clients. Led by the capable, down-to-earth third generation leader Mr. C who believe in making available to his countrymen products and services that used to be affordable by only the rich as his family and personal SWFF, [Company’s name] is now the #1 market leader in air-conditioner (36.7% market share) and refrigeration (25.6% market share) which are under-penetrated appliances in the country, with household penetration rates at 6% and 35% respectively, amongst the lowest in Asia where its neighbours have at least twice the penetration rate, representing significant untapped market potential. Amongst the white good appliances that are disrupted by ecommerce, the sale of aircon and refrigerator remain resilient because they require installation and aftermarket service support. [Company’s name] provides unmatched end-to-end solutions from production to distribution to aftersales services network that spreads across the logistically-challenged country. [Company’s name] has over 90% appliance store coverage nationwide and its unrivalled aftersales service business is supported by over 170 accredited installer companies; over 130 accredited service centers; over 2,000 technicians; rapid sales facilitation and service turnaround from over 1,000 merchandisers deployed at the point of sale; and 8 dedicated parts stores; and a centralized in-house call center, distribution, parts availability/support as well as regional field personnel. Its robust logistics network ensure speedy delivery and fast service response. In terms of business nature, margins and profitability, [Company’s name] is comparable to India’s Voltas (NSI: VOLTAS), India’s #1 aircon company who is an affiliate of the Tata Group with a 20% market share. [Company’s name] has a much higher and more stable market share than Voltas and generates higher ROE at 23.1% as compared to Voltas’ 18.1%. Yet, [Company’s name] trades at a 140% valuation discount in terms of EV/EBIT and EV/EBITDA at 9x as compared with 21x for Voltas. We think [Company’s name] deserves to command a higher valuation premium for its market leadership in an under-penetrated domestic market, its strong portfolio of synergistic businesses, and its visible long run way to reinvest its profits back into the core business to extend its market leadership and widen the moat. The company has a healthy balance sheet with net cash comprising 26% of book equity due to its integrated business model that has enabled the generation of steady, resilient and growing margins, profits and cashflow and the efficient employment of capital with a 23.1% ROE. |