Selloff Rattles Asia’s Bond Market; Plunge in Riskier Corporate Debt Has Left Many Investors with Large Losses, and Stoked Broad Fears

February 25, 2013 Leave a comment

February 20, 2013, 6:47 p.m. ET

Selloff Rattles Asia’s Bond Market

Plunge in Riskier Corporate Debt Has Left Many Investors with Large Losses, and Stoked Broad Fears

By FIONA LAW

Fund managers worried about the end of an extended bull market in bonds might look to Asia, where a sudden selloff in a certain class of risky bonds has left many investors with large losses.

The plunge in so-called perpetual bonds is viewed as a cautionary example of an asset that had gotten too frothy and, some skeptics say, could be a sign of things to come in other corners of the bond market.

Prices of Asia high-yield bonds have continued to surge after a 20% jump last year, while companies have sold a record amount so far in 2013.

Reliance Industries sold $800 million of perpetual bonds, which were down as much as 5%. Above, a Reliance Digital store in Mumbai, India.

Perpetual bonds are corporate bonds that offer relatively high yields but are particularly risky because they would be among the last bonds to be paid off if a company runs into trouble.

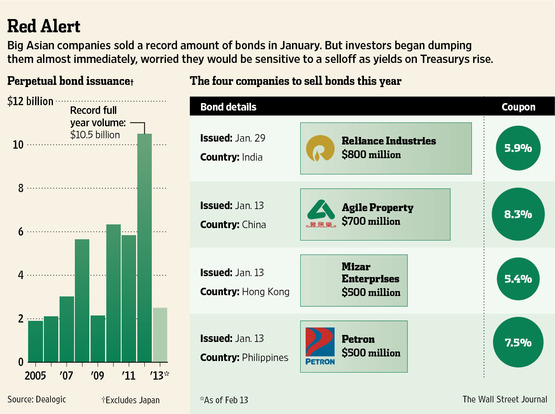

Four big Asian companies issued a combined $2.5 billion of the securities in January to satisfy the growing demand for high-yielding investments by Asia’s wealthy investors.

But almost immediately after the bonds were sold, investors began dumping them amid fears that they will be among the debt most sensitive to a selloff as yields on Treasuries rise in an improving U.S. economy. The rush for the exit sent prices down by nearly 10% in some cases, effectively wiping out nearly two years’ yield.

The sudden slump is a flashing alert for the Asian bond market, says Mark Reade, Crédit Agricole ACA.FR +3.89%CIB’s head of credit analysis. He advises clients to avoid buying some perpetual bonds.

Unlike some “junk” bonds issued by companies unknown to most investors and with poor credit ratings, these perpetual bonds were sold by giant firms controlled by some of Asia’s richest families.

They include Reliance Industries Ltd., 500325.BY +3.13% controlled by India’s Ambani family, and Hong Kong’s Cheung Kong (Holdings) Ltd., 0001.HK -0.89% controlled byLi Ka-shing, Asia’s richest man.

Chia-Liang Lian, a portfolio manager of Western Asset Management, which has $459.7 billion of assets, said he didn’t buy any perpetual bonds issued over the past month in Asia, “as we did not feel investors were sufficiently compensated for the risk.”

He said the volume of new bonds worried him as well. “We were wary of potential indigestion in the broader market, given substantial new supply in January,” Mr. Lian said.

While the bonds theoretically don’t ever mature, most are bought back by their issuer. They usually have a provision that pushes up the yield after a certain time period to give the issuer an incentive to redeem them.

The Cheung Kong and Reliance bonds didn’t have that feature, meaning investors were locked into the yields.

The $2.5 billion of perpetual bonds sold last month was up from $342 million a year earlier, according to Dealogic. Last year, a record $10.5 billion of perpetual bonds were issued, nearly double the amount issued in 2011.

Investors and bankers attribute the selloff to a combination of factors.

The first cause was the sheer amount of bonds issued. Also, they say, investors rushed to buy the bonds without much scrutiny. Only afterward did they realize they were effectively invested in long-term bonds, which are especially sensitive to interest rates. When Treasury rates ticked up this year, pushing the prices of bonds down, some investors sold.

A big stock-market rally drew investors away from the bonds as well. “This is a year of equities,” said Andrew Fung, head of treasury and investment at Hang Seng Bank Ltd.0011.HK +0.95%

For holders of bonds, there is limited room for further gains, given yields are already at rock-bottom levels. That means they may be vulnerable to price corrections, especially if U.S. Treasury yields continue to rise.

“I won’t touch any of them if they are structured with a fixed-rate-for-life feature, while the interest rate environment is apparently in an upward trajectory,” said Leong Wai Hoong, Asia portfolio manager for Nikko Asset Management Asia Ltd., which manages $154 billion of assets.

Indian conglomerate Reliance Industries sold $800 million of perpetual bonds, and Cheung Kong, Li Ka-shing’s flagship real-estate business, sold $500 million of the bonds. The Cheung Kong bonds recently were down as much as 10% from their initial price, while the Reliance bonds were down by as much as 5%. Both are investment grade.

The other two big issues in January came from China’s Agile Property Holdings Ltd.,3383.HK -0.50% which holds a junk rating and sold about $700 million of perpetual bonds. Those fell by as much as 9%. Philippines oil refiner Petron Corp.PCOR.PH -2.00% sold $500 million perpetual bonds. Their prices are up.

Despite the recent selloff, bankers say the demand for yield among Asia’s wealthy investors won’t go away.

“Will the window for perpetuals shut for the rest of this year? I don’t think so,” said Clifford Lee, head of fixed income at DBS Group Holdings Ltd. D05.SG -0.20% “The fundamental demand for bonds is still there.”