India: Government borrowing generates inflation, widens the external deficit and crowds out much-needed investment. Can India now overcome its debt addiction?

February 26, 2013 Leave a comment

India’s public finances

A walk on the wild side

Government borrowing generates inflation, widens the external deficit and crowds out much-needed investment. Can India now overcome its debt addiction?

Feb 23rd 2013 | MUMBAI |From the print edition

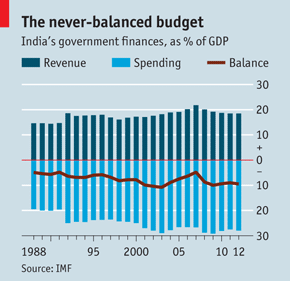

INDIA has grappled with its public finances for long enough. When presenting its first budget after independence in 1947, the finance minister of the day insisted that the country was not living beyond its means. Yet every budget since has failed to produce a surplus. India borrows more heavily than typical big emerging economies and faces more periodic crises. Palaniappan Chidambaram is the latest to try to tame the fiscal beast. He became finance minister, for the third time, last July. On February 28th he will present his budget, possibly the last one before the ruling Congress Party goes to the polls, which must take place by mid-2014.

India’s economy is a concern. Growth is running at about 5%, nearly half what it once was. The external deficit is at a record, while inflation remains stubbornly high. Last year India faced the threat of a downgrade of its credit rating to “junk” status. Thankfully, Mr Chidambaram has shaken Congress from its stupor. The party is to blame for the present budget mess, having launched a pre-election spending spree in 2008 that continued. Subsidies, mainly of fuel, almost doubled, to 2.4% of GDP. The central government’s deficit has been 5-6.5% of GDP. Add in spending by the states, and India’s overall budget deficit has been running at a wild 8-10% of GDP.

When the economy was zipping along, the borrowing did not matter so much. For a while, the national debt actually fell as a proportion of GDP, despite high budget deficits (the ratio is about 70% today). But now, with slower growth, a debt spiral is a real risk. Borrowing has taken a heavy toll. It has fuelled inflation and a balance-of-payments gap, while crowding out the private investment in factories and infrastructure that India badly needs.

Mr Chidambaram says that for the year to March 2013 he will limit the central government’s deficit to 5.3% of GDP. His budget is likely to project a modest decline to 4% by 2015. Chetan Ahya, an economist at Morgan Stanley, notes that the minister is squeezing spending, which fell by 9% in December against a year earlier. Subsidies on fuel are being cut. And the state is selling shares in public companies. Raghuram Rajan, the government’s economic adviser, insists accounting gimmicks will not be used to meet budget targets.

After the budget, however, the outlook is murky. Some still worry that Congress will try to spend its way to re-election. The last three general elections were preceded by splurges. And if a messy coalition comes to office, discipline may slip.

India is in a bind because normal checks and balances have been overwhelmed. In 2003 a Fiscal Responsibility Act was passed, designed to bind politicians to fiscal rules. Although it has led the states to behave better, the central government has ignored it. Meanwhile, the Reserve Bank of India (RBI), the central bank, keeps the debt market under its thumb. It forces banks to buy bonds, prevents foreign investors from participating, and has propped up prices by buying bonds itself. It now owns 16% of the public debt, not far off the level in the crisis year of 1991.

There is plenty of spending on politicians’ crazy schemes. One sanitation project claims to have built 84m rural lavatories, about 60% more than the 2011 census says exist. Meanwhile, fuel subsidies benefit the richest tenth of Indians seven times more than the poorest tenth.

The solution, some hope, is “direct transfer” schemes that give welfare payments directly to the poor, lowering waste and graft. Yet vital though such reforms are, they will not yield enough cash to come close to balancing the books.

Pressures to spend will always exist, says Subir Gokarn, an economist and former bigwig at the RBI. In areas such as education and infrastructure, that is only right. So revenues need to rise. A new report by the IMF compares India with other countries, adjusting for their wealth. It implies that India’s government revenues should be 25% of GDP. At present they are just 18%.

How to raise revenues? Selling off more badly run state firms would help. Lots of state land lies idle and could also be sold. A recent mapping exercise in Ahmedabad, a modest-sized city, concluded that $4 billion could be raised there.

But the tax system needs changing, too. Before India launched market-friendly reforms in 1991, taxation meant clobbering manufacturers with customs and excise duties. Since then the mix has shifted to direct taxes on individuals and firms and indirect taxes on services, which make up three-fifths of GDP. (Farming, which employs half of all Indians, contributes only one-seventh of all GDP and is largely exempt from tax.)

Much of the economy remains out of sight of the taxman. A lot of the services sector is informal and cash-based. The property market is notorious for black money. Big firms in the formal economy pay a decent rate of tax, but many smaller businesses fall under the regime for personal tax, where compliance is poor. Surjit Bhalla, of Oxus Investments, reckons income-tax receipts are two-thirds below what they should be. Just 32m people, or 2.5% of Indians, pay income tax.

Complexity discourages people from joining the formal economy and makes cheating easier. Each state has its own taxes, from the value-added sort and levies on luxury goods to duties on entry to specific areas. To deal with this, the central government has a Goods and Services Tax (GST) in the works. Its aim is to unify the rates of indirect tax across India and replace a tangle of local taxes. It should cut red tape and encourage more activity, such as construction, to enter the formal economy, says Vijay Kelkar, of the India Development Foundation. Encouragingly, rationalisation of the code for direct taxes is also on the government’s to-do list.

The fine print of these measures is still being debated. They have been in the works for years. Some worry that to win over the states, the government will dilute the impact of the GST. Yet these reforms have the potential to bring more of the economy into the tax net, raising revenues by several percentage points of GDP. When Mr Chidambaram speaks on February 28th it will be promises about progress on tax reform, rather than about the deficit two years hence, that will signal whether India is ready to cast off its fiscal chains.