Deflating shadow credit in China

February 27, 2013 Leave a comment

Deflating shadow credit in China

| Feb 27 08:59 | 6 comments | Share

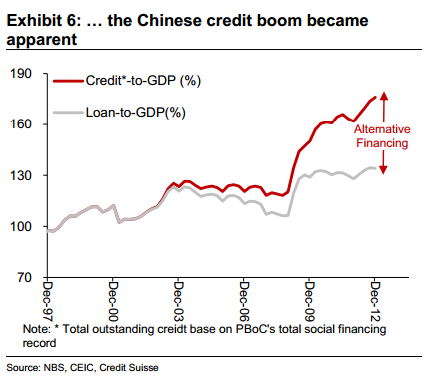

First, a reminder of the degree to which China’s growth has been increasingly fuelled by credit over the past few years:

The chart above doesn’t quite show it, but non-bank credit growth outpaced bank loans last year. The rise of China’s shadow banking scene has happened very rapidly — much of the growth only happened since 2009.

Shadow banking in China is not all necessarily shadowy; in fact some of it, such as trusts, are legal and regulated at least to a degree. A chunk of shadow loans are also originated by banks (Anne Stevenson-Yang of J Capital Research reckons about 30 per cent).

But it does also include a number of ever more complex and opaque products such as wealth management products. The underlying assets are hard to determine and usually turn out to be property or financial in nature. Investors often assume banks and the state are guaranteeing the principle because of the way they are marketed.

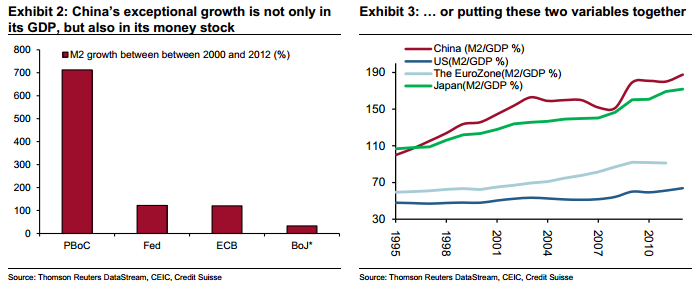

Although the regulatory status and state-backing of many shadow products is not clear, it’s not as though the authorities have been fighting their rise. Actually, it’s kind of the opposite: shadow finance has been a vital mechanism for the substantial amounts of money being pumped into the economy:

Yet it’s one that Chinese policymakers have only loose control over. There are clear signs, for example, that the central Chinese authorities are again worried about excessive property prices. And the pace of innovation in unregulated products is at times astounding.

There are numerous reasons to think China’s credit growth is at unsustainable levels. Morgan Stanley’s Ruchir Sharma sums up some of these reasons in a WSJ op-ed, citing a BIS paper by Mathias Drehmann and Mikael Juselius which finds that if the private debt-to-GDP ratio increases by 6 per cent or more above its 15-year average, that is a “very strong indication that a crisis may be imminent”.

The risks are huge. These investment properties and their derivative financial products make up the life savings of many Chinese people. If the credit growth contracts, what happens to the asset values?

Credit Suisse’s Dong Tao and Weishen Deng ask the obvious question: Why doesn’t Beijing stop shadow banking activities? Well, elements of Chinese leadership would like to — particularly at the People’s Bank of China. But there’s reluctance to rein in such a crucial facilitator of growth, write Tao and Deng:

We believe the entire push behind shadow banking is deeply rooted in the government’s desire for growth. Shadow banking activities have increased because China needs growth, and the banking sector has to a significant degree failed in its role of financial intermediary. Indeed, some government bodies have put out some restrictions on certain types of shadow banking operations, but the core issue has not been addressed. Private investment has disappeared in China, as manufacturing production becomes unprofitable due to surging salaries and severe over-capacity. Without the re-engagement of private investment, we believe the government will have no choice but to rely on infrastructure projects. It may ban one type of financial instrument, but it still has to deliver liquidity to local governments through alternative channels.

The CS strategists say 2015 is the time when this could all fall apart. They identify two key reasons: one is the maturation of some of the early wave of the current trust fund era. The other is inflation:

A key catalyst that we think could turn the shadow banking sector upside down is the incoming pick-up in inflation and potential for an eventual interest rate hike. The food cycle, especially the pork cycle, has already started moving upward. By the end of 2013, we project inflation will reach 4%, from its current 2.0%. The PBoC’s window of monetary easing is closed. Judging from the rise in rents and salaries, there is a good chance that the CPI could move towards 5%, forcing the central bank to tighten in 2014.

Credit Suisse are not the only ones anticipating inflation will return to steep levels soon. Nomura have been going on about this for nearly a year, and are forecasting inflation at 4.4 per cent in the second half of 2013.

CS argues that in the face of rising inflation, the shadow products’ “guaranteed” returns may look less attractive than just taking a punt directly in property and stocks. A drop in flows into some of these entities would be difficult to withstand:

Most shadow banking entities run on a thin equity base, so if one or two projects default, the capital base would likely be wiped out. The market would then be much more concerned about credit risk among shadow banking entities, as the funding drain and duration mismatch would be likely to be exposed.

Of course there’s still the possibility that the relevant authorities will do something about this. Our Beijing colleague Simon Rabinovitch revealed last night that plans are firming to more closely regulate the shadow finance sector, and perhaps to rein it in. Simon’s story should really be read in its entirety because it’s a complicated issue, but here’s a couple of representative paragraphs:

Taken together, the new regulations could lead to a slowdown in the explosive growth of China’s shadow banking by making it tougher for banks to funnel deposits into off-balance sheet vehicles.

But the moves would not spell the end of shadow banking. Instead, they reflect a consensus among policymakers that credit flows outside the banking system are a healthy development for China, so long as they are monitored and kept in check.

This isn’t a completely out of the blue — several central agencies have been signalling unease with the recent rate of credit growth, particularly the PBoC but also an influential economic planning agency (the NDRC) and the banking regulator (the CBRC). But again, the question comes back to how much China’s sometimes wild credit growth can be curtailed at the expense of economic growth.