Australian Central Bank Gov. Glenn Stevens Warns Against Hubris

December 10, 2013 Leave a comment

Australian Central Bank Gov. Glenn Stevens Warns Against Hubris

Stevens Faces Challenge of Weaning Economy Off Reliance on Mining

JAMES GLYNN

Dec. 8, 2013 3:13 a.m. ET

SYDNEY—Glenn Stevens steered Australia safely through the global financial crisis as head of the country’s central bank, taking decisive action that included cutting interest rates by 100 basis points in a day. Now, as growth again slows and joblessness rises, he warns Australia faces a new threat: hubris.

“We are building up this myth of 22 years uninterrupted growth. We shouldn’t do that,” Mr. Stevens said in an interview. “Sooner or later we’ll have another downturn.”

As the bank’s chief since 2006, Mr. Stevens, 55 years old, has presided over an unprecedented period of prosperity as demand for Australia’s raw materials such as iron ore to fuel Chinese steel mills and factories powered growth. The decadelong mining boom has reinforced the country’s reputation as “The Lucky Country.”

But with China’s economic engine slowing, Mr. Stevens faces one of the biggest challenges of his three decadeslong career: a race to wean the economy off its reliance on mining.

“We would be foolish to think that we have found the secret of completely eliminating the cycle, because we haven’t,” said Mr. Stevens, who earned a master’s in economics at the University of Western Ontario, and considered becoming a professional jazz musician before joining the Reserve Bank of Australia in 1980. “If we are sensible and prudent, and just a bit lucky, we can have cyclical downturns that are not so deep.”

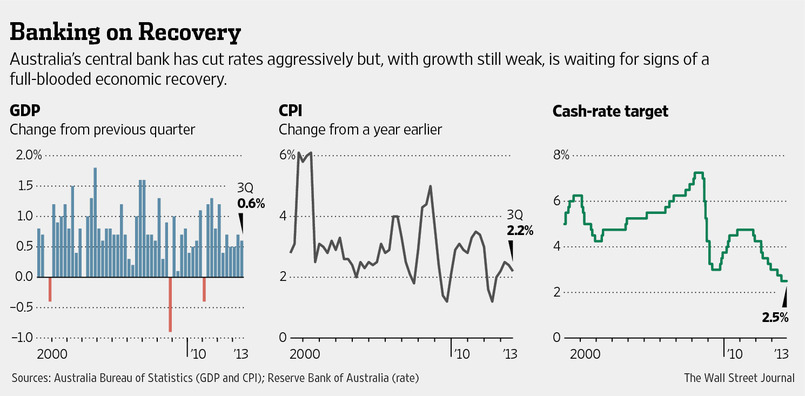

Australia’s central bank has slashed interest rates eight times in the past two years to a record-low 2.5% to help an economy suffering because of lower commodity prices. In doing so, Mr. Stevens has gone against his traditional hawkish leanings toward inflation. Having avoided recession, Australia was one of the first developed nations to tighten rates after the global financial crisis in October 2009. Ahead of the crisis, the governor was criticized for raising rates to head off inflation and keeping them high right up to the eve of the Lehman Brothers collapse in 2008 that tipped the global financial system into chaos.

“He makes his calls based on his best judgment and they are not necessarily affected by the politics of the time,” said Wayne Swan, the country’s Treasurer for six years until his left-leaning Labor party was defeated in September elections. He said Mr. Stevens was a thoughtful central banker who didn’t get drawn into the style of debate seen in the U.S., where opposing views of Federal Reserve leaders are often aired publicly.

“He is more into constructive, realistic, economic management,” Mr. Swan said, adding that he had never seen the dry, softly spoken governor lose his cool through the financial crisis, even as emotions were running high.

Despite Mr. Stevens’s outwardly reserved manner, one current member of the Reserve Bank’s policy-setting board, speaking on condition of anonymity, said the governor has a boldness that puts him in the same class as outgoing Federal Reserve chairman Ben Bernanke. “Bernanke had the willingness, in the U.S. circumstance, to go for quantitative easing in a very big way. We don’t have the same circumstances. But that kind of boldness and freedom from preconceptions is something that would be characteristic of Stevens,” he said.

That boldness was on display in October 2008 when, responding to the Lehman crisis, he cut interest rates by 100 points in a single day. He recalls taking a call from then Bank of England Governor Mervyn King, who asked for an update on the early reaction of financial markets to news of the Lehman collapse: New Zealand and Australia were among the first markets to open in the hours following the news.

Still, Mr. Stevens said his career at the central bank has been punctuated by private doubts. He nearly quit the bank a couple of times after headhunters came calling, as they did successfully with several colleagues.

“There was a time, and I think many people will experience this in the public sector, when you have got a young family and a mortgage. You could have turned left out of the train station in the morning instead of right and be paid 50% or 100% more,” Mr. Stevens said.

In September 2006, he was so convinced that he was going to be passed over for promotion that he even prepared his wife for disappointment over dinner one evening. It was only when the phone rang the next day that he heard from then Treasurer Peter Costello the job was his.

Now, Mr. Stevens is among the world’s most highly paid central bankers, earning more than 1 million Australian dollars (US$910,200) a year—more than the head of the U.S. Federal Reserve. That in itself has drawn criticism, especially amid a prevailing mood of austerity in the wake of the financial crisis.

Mr. Stevens harbors a thick skin and a pragmatic streak, though, that has allowed him not to be swayed by public or political opinion, according to former and current board members of the central bank. Recently, that pragmatism has led him to slash rates to reinvigorate an economy at risk of sinking just as the U.S. and Europe show signs of recovery.

“I think that some of the big jurisdictions are still in crisis-management mode a little bit,” Mr. Stevens said. “These economies are growing, but the legacy of the crisis period is still very much with them.”

The dilemma now for Mr. Stevens, though, is that rate cuts haven’t yet yielded the response the bank had hoped for: The economy expanded by just 2.3% in the year through September, much slower than quarterly growth rates as high as 4% last year.

Business investment outside of mining remains weak. And while construction and retail sales are recovering, the nation’s exporters are still grappling with a strong Australian dollar exchange rate—buoyed by the easy-money policies in the U.S. and elsewhere.

At the same time, Mr. Stevens faces the risk that in keeping rates low the bank is pushing up already frothy house prices, which recently surpassed a 2010 peak. The central bank on Tuesday kept interest rates steady for the fourth-straight month, saying it needed to see more proof the economy was rebalancing away from mining before it could rule out further cuts.

With the economy still too weak to raise rates—as it did in 2009 and 2010 to head off a nascent housing bubble,—Mr. Stevens is left with few options to aid the slowing economy other than talking the currency down.

Mr. Stevens last month said he was “open-minded” about the idea of central bank intervention to bring down the level of the local dollar, although his deputy Philip Lowe later said the threshold for intervention—in which the Reserve Bank would actively sell the Aussie dollar and buy foreign currency—was still “fairly high.”

Steering a six-seat plane through turbulence above Sydney recently—in his spare time—the governor pilots “angel flights” rescuing seriously ill patients from remote parts of the sparsely populated continent—Mr. Stevens declined to comment further on the currency.

Some economists argue, however, that he has been wrong to attempt to jawbone it lower. Neville Norman, a former consultant at the central bank and president of Australia’s Economics Society, who knows Mr. Stevens personally, said it was a “divisive” tactic that failed to recognize the benefit of a high exchange rate to some industries.

“Over the last six to eight years, the bank has failed to read the economy directly, and it would have been better to have left interest rates on hold. They’ve basically got it wrong nearly all of the time,” said Mr. Norman.

Mr. Costello, the former Treasurer in the center-right government of John Howard, said Mr. Stevens has been a steady hand doing a good job through difficult times.

Still, he felt the Reserve Bank of Australia failed to see the global financial crisis coming, and had raised interest rates too far in 2007-08 just as the crisis began to deepen.

“They were still raising rates when the subprime crisis was beginning to affect America,” Mr. Costello said. “I think they missed the fact that this was going to be quite a huge fallout.”

Demand for Australian exports of resources over the past 10 years pushed the country’s dollar to record highs against its U.S. counterpart and made it the world’s fifth most traded currency. That export boom boosted the economy and made Australian-dollar assets a haven, helping the country ride out the financial crisis. But it also hollowed out the manufacturing sector, as locally made goods became too expensive on a world stage.

Like many major economies, Australia has relied heavily on its central bank and exports to boost growth in recent times as lawmakers have shied away from any new spending pledges and sought to pay down debts incurred during the financial crisis.

The challenge now for Australian lawmakers is to nurture long-term growth through productivity gains, said Mr. Stevens.

“As a country we have to go get it. It doesn’t just land in our lap,” said Mr. Stevens. “Relative to most major developed economies, Australia’s economic challenge looks achievable.” What’s needed is a return to the reform agenda of the 1980s and 1990s, he said.

“That period produced a lot of change that paid off. There’s no reason why that can’t be done again,” Mr. Stevens said, referring to a period when the country floated its currency, deregulated banks and financial markets and reduced tariff barriers, which helped to spur sharp productivity gains.

“I’m reasonably optimistic,” he said. “We need to be doing things that foster innovation and productivity.”