Bursting the Stock-Market-Bubble Bubble

December 22, 2013 Leave a comment

Bursting the Stock-Market-Bubble Bubble

JUSTIN LAHART

Dec. 15, 2013 1:46 p.m. ET

No, stocks are not in a bubble. But that doesn’t mean investors must like them. With the S&P 500 up a blistering 25% this year, and with stocks like Tesla MotorsTSLA +1.79% sporting valuations that strain belief, the word “bubble” has been getting batted around a lot lately. Case in point: Over the past three months, a Factiva search returns 391 news articles with “bubble” in close proximity to “stock market”, up from 130 over the same period last year.Given that the dot-com stock bubble occurred during the professional lives of many, if not most, people investing today, the idea that what’s happening now is similar is odd. The S&P traded at 28 times prior-year earnings at its peak in 2000 compared with a price/earnings ratio of 17 now. The Nasdaq Composite’s ratio was 142 at its peak compared with 22 now.

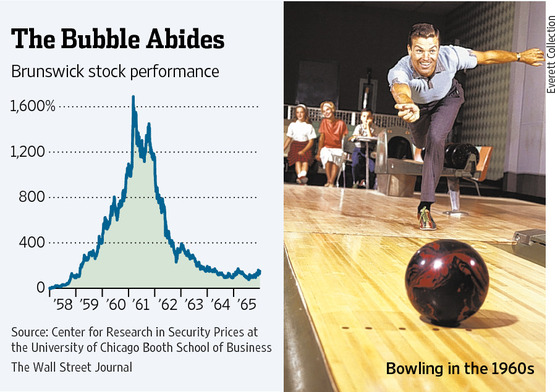

Nor should the fact that some companies’ shares seem bubbly be taken as a reason to be in a lather about the overall market. Think about the great enthusiasm investors showed for bowling-company stocks in the late 1950s and early 1960s.

When shares of Brunswick peaked in 1961, they were 1,590% higher than at the end of 1957, according to stock-price data from the Center for Research in Security Prices at the University of Chicago Booth School of Business. That was the end of the bowling bubble, but it wasn’t the end for stocks—the deep bear market of the 1970s was still more than a decade away.

Other hallmarks of bubbles also are missing. When a market is frothy, investors tend to trade very actively—a sign the greater-fool-theory (as in “I can find some greater fool to buy this at a higher price”) is in effect. But stock-market volume remains muted.

Nor have individual investors shown much of a penchant for stocks. When Gallup last conducted its stock-ownership poll in April, only 52% of people said they owned shares directly or indirectly, such as through a mutual fund. That compared with 62% in April 2000, and was the lowest reading in the 15 years Gallup has been asking.

But stocks don’t have to be in a bubble in order to be too expensive.

Although the S&P’s P/E multiple is only slightly higher than its average since the late 1950s, the profits that multiple is based upon may lack staying power if companies end up having to use more of their revenue to cover costs. Given how elevated profit margins have been, that seems likely.

After-tax corporate profits as a share of gross domestic product (a proxy for overall profit margins) were a record 11.1% in the third quarter, versus an average of 6.1% since 1929.

That is a reflection of how little hiring companies have done since the financial crisis, and how little they have spent on new equipment.

Given how leanly companies are running, and that the economy seems poised for better growth next year, they will now be faced with a tough choice. That is to spend more or lose market share.

Profit margins aren’t going to collapse next year, but they seem more likely to narrow than widen. If stocks continue going up next year, this will probably be on the back of more stretched valuations than stronger earnings.

And going beyond next year, one would expect there will come a time when the share of the GDP going directly to U.S. workers rather than corporate coffers will rise again, giving way to profit margins that look more like the historic norm. That will make its way into stock prices.

Consider this: Federal Reserve figures released last week show that in the third quarter, the value of U.S. equities was 234% of annualized, after-tax household income. That is a level that has only been surpassed during the dot-com boom and nearly twice the average since 1950.

Things don’t have to be in a bubble to seem out of kilter.