Bond-Yield Rise Means Borrowers Will Pay More; U.S. Treasury Bond Yield Climbs Past 3% for the First Time in More Than Two Years

December 28, 2013 Leave a comment

Bond-Yield Rise Means Borrowers Will Pay More

U.S. Treasury Bond Yield Climbs Past 3% for the First Time in More Than Two Years

MIN ZENG and MIKE CHERNEY

Updated Dec. 27, 2013 7:10 p.m. ET

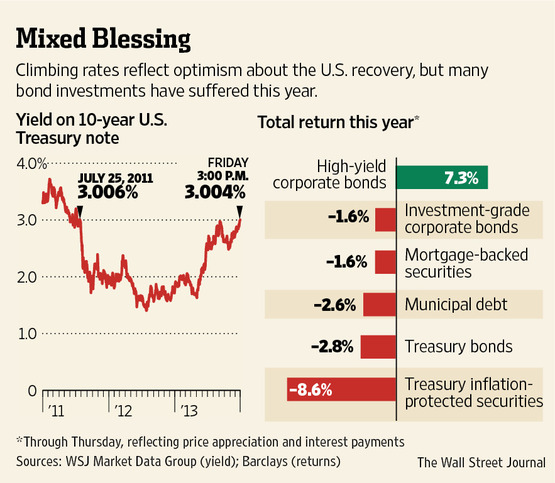

Growing confidence in the economy pushed a widely followed U.S. Treasury bond yield above 3% on Friday for the first time in more than two years. The benchmark 10-year note’s yield rose to 3.004%, pushing the price down 4/32 from Thursday’s close. While the yield already had more than doubled since sinking to a record low in July 2012, many analysts saw the 3% mark as a test of investors’ faith in the economic rebound’s staying power.The yield rose during every trading session of the holiday-shortened week, propelled by upbeat data from the labor and housing markets, business spending and household consumption. When bond yields rise, their prices fall.

But rising yields make borrowing more expensive. The 10-year Treasury yield is a reference point for many loans to U.S. businesses and consumers—and is used to set terms for foreign governments and companies selling bonds in U.S. dollars.

Trading in the 10-year note also helps determine interest rates in the $10 trillion U.S. home-loan market.

Analysts said Friday’s climb above 3% means interest rates that have jumped since the 10-year yield bottomed out in July 2012 will likely go even higher, though they will remain unusually low in historical terms.

“We are seeing the tide turn from a lower-rate era to a higher-rate era,” said Chris Rupkey, chief financial economist at Bank of Tokyo-Mitsubishi UFJ.

Some economists are worried that higher interest rates might start weighing on economic growth. But many investors and analysts expect little or no impact as long as future rate rises are gradual.

It also helps that inflation is low, constrained by inconsistent demand among businesses and consumers. Meanwhile, home-construction and house prices have improved despite higher mortgage rates.

Still, the climb in interest rates tied to the 10-year note’s yield is causing some prospective purchasers to reassess their plans.

Darien, Conn., officials are more likely to pay cash for property targeted for parkland, rather than borrow $1.9 million in the bond market, said Kathleen Buch, Darien’s finance director.

In 2012, the New York City suburb took advantage of low rates by selling $33.6 million in bonds to refinance existing debt. The move saved $2 million. “If we have to borrow at higher rates, that means the budget is impacted,” she said.

“The 10-year U.S. Treasury bond yield has more than doubled since its record low in July 2012.”

Bruno Fiabane of Princeton, N.J., closed earlier this month on his purchase of a second home in Vero Beach, Fla. The 66-year-old Mr. Fiabane decided to buy the $1.5 million home with cash after home prices rebounded and rising rates soured him on a loan.

“We saw prices really start to turn about six months ago, so we were much more inclined to make a decision,” said Mr. Fiabane, who runs an insurance business in New Jersey. He plans to use the Vero Beach property after he retires.

The average interest rate for a 30-year fixed-rate mortgage rose to 4.48% this week from 4.47% last week and 3.35% a year ago, according to Freddie Mac.

Investors have sold Treasury bonds en masse this year to seek higher returns in stocks and riskier fixed-income assets. Through November, U.S. bond funds targeting Treasury debt suffered a net outflow of $40.2 billion in 2013, according to data provider Morningstar Inc.

In contrast, funds that invest in low-rated “junk bonds” issued by U.S. companies have attracted $2.6 billion from investors.

Treasury bonds are on track to suffer their biggest annual loss since 2009, according to Barclays PLC.

As of Friday, the Dow Jones Industrial Average was up 26% so far this year, on pace to finish with the benchmark index’s strongest annual gain since 1996. The Dow slipped 1.47 points Friday to 16478.41, snapping the longest winning streak since a 10-session run that ended in March. For the week, the index rose 1.6%.

Stocks have remained strong despite the Federal Reserve’s announcement this month that it will start scaling back its $85 billion-a-month bond buying in January.

That is the central bank’s first major step to wind down its monetary stimulus five years after the financial crisis hit.

Some investors see no end in sight to the move into stocks from Treasury bonds. A continued exodus would push bond prices even lower and the 10-year yield higher.

“If we carry the economic momentum into next year and break above 3%, then one has to look for larger moves with an eye toward the 2011 yield highs at 3.75%,” said Jason Evans, co-founder of hedge fund NineAlpha Capital LP in New York.

Rick Rieder, co-head of Americas fixed income at asset-management giant BlackRock Inc., said he doesn’t expect interest rates to rise sharply. The reason: Fed officials have pledged to keep rates low through at least early 2015.

As a result, “risky assets will be in good shape for a while,” said Mr. Rieder.

Some analysts believe that investors who are lukewarm on Treasurys will resume buying them when the 10-year yield nears 3.25%.

At that level, Treasurys would look like a good value compared with stocks because the bonds are lower in risk and pay regular income.

Three percent is “a level that’s been out of reach for some time and represents good value relative to inflation, other industrial economy bonds and a moderately expanding U.S. economy that still faces challenges,” said Christopher Sullivan, chief investment officer at United Nations Federal Credit Union.

Opinions differ widely on how far or how fast the 10-year yield will rise now that it has crossed the 3% mark.

“Treasury yields are likely to crest in the 3% zone,” said Robert Tipp, chief investment strategist at Prudential Fixed Income, a unit of Prudential Financial Inc., Newark, N.J.