How to Invest as Interest Rates Rise; Treasury yields are on the upswing. Here’s how to adjust your portfolio

January 5, 2014 Leave a comment

How to Invest as Interest Rates Rise

Treasury yields are on the upswing. Here’s how to adjust your portfolio.

JOE LIGHT

Updated Jan. 3, 2014 11:51 p.m. ET

And so a new era begins. As interest rates rise, investors need to take a hard look at portfolios that were designed to hold up when yields were on the decline and safety was in high demand. It may be time to ditch beloved high-income sectors, such as utilities and telecommunications, in favor of those in which companies can increase earnings more quickly as the economy picks up steam. Commodities, which often suffer as interest rates rise, will be a tricky bet. Home values haven’t been as hurt by higher mortgage rates as you might expect.What the Market Did Under Past Fed Chiefs

In fixed income, investors should stay away from Treasurys and mortgage bonds—the securities most directly affected by the end of the Federal Reserve asset-buying program designed to juice the economy—and look for deals among municipal bonds that have been punished by default fears. Resist the temptation to load up on short-term debt.

Interest rates have been heading steadily down for more than three decades, but last year the rate on the benchmark 10-year Treasury climbed 1.27 percentage points to 3.03%, ending a three-year streak of declines and prompting investors such as Pacific Investment Management Co.’s Bill Gross to predict that the long bull market for bonds has ended. The rise in rates stuck investors in funds that track the Barclays U.S. Aggregate Bond Index with their first loss since 1999—albeit one of only 2%.

It’s important not to overreact. “Some investors have concluded that there’s a 30-year bear market in front of us,” says Kathy Jones, vice president and fixed-income strategist at the Schwab Center for Financial Research, a division of San Francisco-based brokerageCharles Schwab. SCHW +0.31% “It’s more likely that we just see a small, gradual rise in rates.”

What to Do Now

It is possible that interest rates won’t rise much further than they have already. Since 2000, 10-year Treasury yields have tended to settle about 0.7 percentage point below economic growth before adjusting for inflation, Ms. Jones says.

At current growth levels, that suggests the natural rate for Treasurys would be somewhere between 3% and 3.5%—not much higher than it is now.

There also isn’t any rule that bond rates can’t stay low for prolonged periods. Japanese 10-year government bonds have had a yield of less than 3% for well over a decade.

As bond rates dropped between 2010 and 2013, yield-hungry investors snapped up anything that could give them more income, including stocks of utility and telecommunications companies and real-estate investment trusts.

Yet in 2013, those stocks performed the worst relative to the broad market. A typical S&P 500 exchange-traded fund rose 32% in 2013. But the Utilities Select Sector SPDRXLU -0.32% climbed 13%. The iShares Global Telecom ETF IXP -0.28% gained 24%.

This year, if rates continue to rise, investors should expect these sectors to continue to underperform, says Alec Young, global equity strategist at S&P Capital IQ.

“The question is: How big a deal was the yield when someone bought one of these stocks?” Mr. Young says. Those stocks will continue to perform poorly, he says.

Investors should lean toward economically sensitive sectors, such as consumer-discretionary companies—which sell items such as automobiles—energy and financial stocks.

“There is some good news: Higher rates normally lead to higher returns for stocks and bonds.”

Those last three sectors have the added advantage of being relatively cheap. As of Thursday, the price/earnings ratio of the S&P 500, based on the past 12 months of earnings, is about 16.7, according to FactSet, compared with P/Es of 16, 13.9, and 14.2 for consumer discretionary, energy and financials, respectively.

It is easy to get exposure to such sectors with ETFs such as the Vanguard Energy ETF,VDE -0.24% which charges annual fees of 0.14%, or $14 per $10,000 invested. TheVanguard Consumer Discretionary ETF VCR -0.15% costs 0.14%, while the Financial Select Sector SPDR XLF +0.69% costs 0.18%.

Emerging-market stocks and bonds might have a lot to lose as the Fed unwinds its stimulus programs and, eventually, starts to raise short-term interest rates, says Ed Yardeni, president of Yardeni Research, an investment-strategy consultancy in Brookville, N.Y.

Many investors looked to emerging markets for income. If U.S. bonds, which are much less risky, start offering higher yields, Mr. Yardeni expects that investors will move back in that direction.

Research from Harvard Kennedy School of Government professor Jeffrey Frankel has found that commodities also tend to suffer when inflation-adjusted interest rates rise.

That is because as rates rise, the incentive to extract and the cost of storing commodities also goes up, and investors look for better returns elsewhere, Prof. Frankel says.

To be sure, though commodity prices historically have suffered when intermediate and long-term rates rise, they are more affected when short-term rates climb, he says, something that might not happen for years.

“It’s quite possible that after 30 years of a downward trend in interest rates, we could see them move upward in coming years and that could result in sending real commodity prices down,” he says.

Higher Returns

There is some good news: With higher rates, stock and bond returns should improve.

To figure out how interest rates affect gains, Elroy Dimson, an emeritus professor of finance at London Business School who researches the history of financial markets, and his colleagues Paul Marsh and Mike Staunton, looked at stock and bond performance from 1900 through 2012 in 20 countries, including the U.S., U.K., Japan and other developed and emerging markets.

Over those 113 years, average five-year returns for stocks and bonds were better when rates were elevated.

For example, when inflation-adjusted interest rates were between 0.1% and 1.5%—the range in which U.S. rates are now—stocks had an average annual total return, including dividends, of 3.9% after inflation over the subsequent five years, while bonds were flat.

In an interest-rate range of 1.5% to 2.8%—where rates were before the financial crisis—stocks historically have returned 4.9% annually over the next five years, while bonds have returned 1.5%.

“When interest rates are low, you’ve gotten rotten returns on bonds and rotten returns on equities,” Prof. Dimson says.

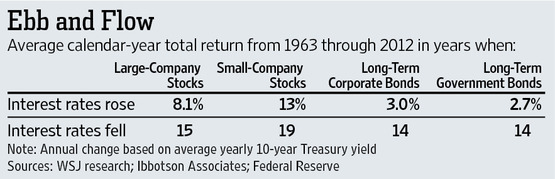

While higher rates can improve returns over the long term, there can be a lot of pain along the way. From 1963 through 2012, 10-year Treasury yields rose on average during 26 calendar years and fell in 24 years before adjusting for inflation, according to Federal Reserve data.

In an average rising-rate year, large-company stocks delivered returns, including dividends, of 8.1%, before inflation, according to a Wall Street Journal analysis of U.S. data from research firm Ibbotson Associates. That is 6.5 percentage points less than such stocks earned in falling-rate years.

Because long-term government bonds take the longest to mature, rising rates hurt such bonds the most. During a rising-rate year, long-term government bonds have returned an average 2.7%, 11 percentage points less than when rates fell.

Still, even in bonds, there are some steps you can take to improve your returns.

Impact on Bonds

Investors might be tempted to move the bulk of their fixed-income portfolios into cash or very short-term bonds. Such a move gives protection from rising rates but also gives up the income and diversification benefits bonds provide. There are better strategies.

To gauge a portfolio’s sensitivity to interest rates, investors use a measure called “duration.” A portfolio with an average duration of five years, for example, would be expected to lose 5% in price if rates were to rise by one percentage point immediately.

However, as the market begins to anticipate the Federal Reserve raising short-term interest rates, investors might find that portfolios with similar durations aren’t affected equally, says Jonathan Lewis, chief investment officer at Samson Capital Advisors in New York, which manages $7 billion.

That is because bonds that mature in between four and five years could see rates rise—and prices fall—more rapidly than both shorter- and longer-term bonds, he says. In other words, though a duration measure assumes that rates on bonds with any maturity rise equally, in reality, intermediate bonds could get hit hardest.

To achieve duration of four to five years without investing in bonds with those maturities, bond investors can use a “barbell” of shorter-term bonds and longer-term bonds, which together can average out to the same level, Mr. Lewis says.

Mutual-fund investors can see how the maturities of their funds’ bonds are distributed by looking at the “portfolio” tab on the fund’s page at Morningstar.com.

By the same token, investors would be well served by venturing away from Treasurys to other relatively safe bonds with slightly higher payouts, Schwab’s Ms. Jones says. That means taking a look at investment-grade corporate bonds and municipal bonds, she says.

One low-cost option is the Vanguard Intermediate-Term Corporate Bond ETF,VCIT +0.06% which yields 3.5% and has an annual expense ratio of 0.12%.

Municipal bonds, whose income is exempt from some taxes, right now have about the same interest rate as Treasurys, making them attractive to high-income investors in taxable accounts, Ms. Jones says.

Historically, the highest-rated muni bonds’ tax-advantaged status has caused their yields to be lower than those of Treasurys. Muni yields are now even with those of Treasurys in part because of legitimate worries of default for bonds issued by Detroit, Puerto Rico and a few other troubled areas, but thus far, those problems have remained isolated, Ms. Jones notes.

Finally, though rising rates will lead to higher mortgage prices, that shouldn’t necessarily cause home prices to drop, says Thomas Lawler of Lawler Economic & Housing Consulting in Leesburg, Va.

Historically, there’s been very little relationship between home prices and mortgage rates, all else being equal, he says. Of course, if higher rates come because of higher inflation or rising incomes, that could lead prices higher, he says.

In the short term, Mr. Lawler says, home prices might rise more slowly as institutional investors slow their buying and new-home inventory starts to hit the market.

Yet he says it still is a decent time to buy a home for buyers with good credit who plan to live there for a number of years and aren’t thinking of their home as an investment.