Emerging-Market Slide Tests How Much Nations Learned From Past

January 31, 2014 Leave a comment

Emerging-Market Slide Tests How Much Nations Learned From Past

IAN TALLEY

Jan. 29, 2014 7:46 p.m. ET

WASHINGTON—The latest emerging-market slide might look like a repeat of earlier cascading crises.

In reality, it is serving as an important test of which nations learned their lessons then.

The rapid interest-rate increases in South Africa, Turkey and India in recent days hark back to troubles in Asia in the late 1990s and Latin America in the early 2000s, when economies crumbled and investors fled while policy makers were forced to boost rates.

Today, more governments have floating exchange rates. Many have tackled their debt loads, winning points from foreign creditors. The adjustment will still be difficult, but emerging economies are already demonstrating an ability to break from the past.

“Emerging markets are more robust than they were in the last crisis,” said Uri Dadush, an economist at the Carnegie Endowment for International Peace and former World Bank official. “They learned from last time. They didn’t let things get out of hand quite as much as they did then.”

Related

Investors Face Shift in Markets as Fed Scales Back Stimulus

In Parting Gift to Bernanke, First Unanimous Decision Since 2011

Russia Prepared to Let Ruble Slide

Fed Sticks to Script on Paring Bond Buys

As Currencies Fall, Leaders Cast Blame Abroad

Rate Gambit Raises Stakes for Turkish Central Banker

Emerging-Market Slide Tests How Much Nations Learned From Past

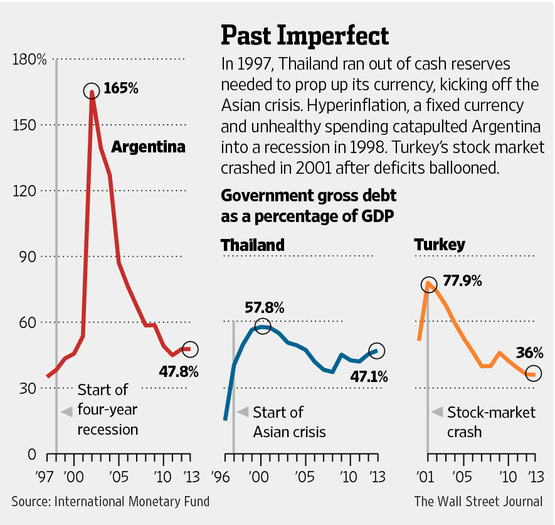

In earlier crises, many emerging economies had gorged on cheap cash from abroad without end. Officials had few tools to stem sudden outflows of foreign capital when investors realized many nations couldn’t sustain the high growth rates. When the sugar high ended, investors concluded it was a similar enough story from Argentina to Thailand.

The Asian crisis started ricocheting through the world after Thailand in 1997 ran out of cash reserves to prop up the currency. In Argentina, hyperinflation, a fixed exchange rate and unhealthy government spending catapulted the nation into a four-year recession at the end of 1998. The troubles forced the country to seek an International Monetary Fund bailout and ended in a government debt default in late 2001. Also in 2001, Turkey’s stock market crashed after Ankara admitted it had relied too much on foreign borrowing, and slowing growth couldn’t support ballooning government deficits.

The latest shock waves appeared to start last year as a generalized rout across emerging markets after the Federal Reserve signaled an exit from its easy-money policies.

But investors now are showing signs of discriminating between nations with stronger economic foundations, such as Mexico and Poland, and those with economic and political vulnerabilities, such as Turkey and Thailand.

“It will shift from being a generalized selloff to being concentrated on a couple of countries that have real problems,” said Adam Posen, president of the Peterson Institute for International Economics.

With a few exceptions, the largest emerging economies are importing proportionately less today than they did in the past. They are borrowing less from abroad, so when local currencies fall in value, the government and domestic firms aren’t as vulnerable to losses. They have also built up larger emergency cash buffers.

And unlike in previous crises, their currencies aren’t fixed at a specific rate. Back then, officials feared that allowing the value of their currency to fall would balloon the cost of paying off debt borrowed in dollars. Now, flexible exchange rates help absorb the impact from large investor moves in and out of their markets. They also curb excessive borrowing from foreigners.

That is one reason U.S. officials and the IMF aren’t as shaken by the recent selloffs.

U.S. Treasury Secretary Jacob Lew on Wednesday said markets are differentiating between emerging markets. “We’re seeing the countries that have taken tough actions and managed well are having a different experience,” he told reporters.

Still, addressing the latest troubles will require painful adjustments. India, Russia, South Africa, Turkey and Brazil are all battling rising prices, even though growth has drifted down in recent months. Governments have been too reliant on the cheap cash flowing in from abroad, and haven’t done enough to fix infrastructure bottlenecks and other constraints to more competitive growth.

Central banks in emerging economies are walking a tightrope in balancing a straightforward dilemma of inflation versus growth, rather than maintaining fixed-rate currencies.

The sharp currency declines are making imports for countries like Turkey and South Africa more expensive, driving inflation higher and exacerbating underlying growth problems. Raising interest rates would slow the outflow of capital and maybe even attract investors, boosting the currencies and slowing inflation. But it is also likely to slow their growth.

“It’s pretty straightforward,” Mr. Posen said. “They were too loose on monetary and fiscal policy, and now they have to tighten.”

Although central-bank officials in several regions have moved this week to temper dangerously high inflation, few believe the work is over.

“The pain is likely to get worse before any competitiveness gains kick in,” said Shweta Singh, an economist at London-based Lombard Street Research, in a note to clients.