European regulators warn as risky loans rise above bubble peak

April 5, 2014 Leave a comment

March 23, 2014 7:31 pm

European regulators warn as risky loans rise above bubble peak

By Anne-Sylvaine Chassany and Martin Arnold in London

Debt investors are abandoning normal creditor protections on European leveraged buyout loans as they snap up riskier securities at a faster rate and in greater proportions than at the peak of the credit bubble.

Growing volumes of euro-denominated “covenant light” loans have now aroused the interest of European regulators, who are increasing their monitoring of lenders’ behaviour.

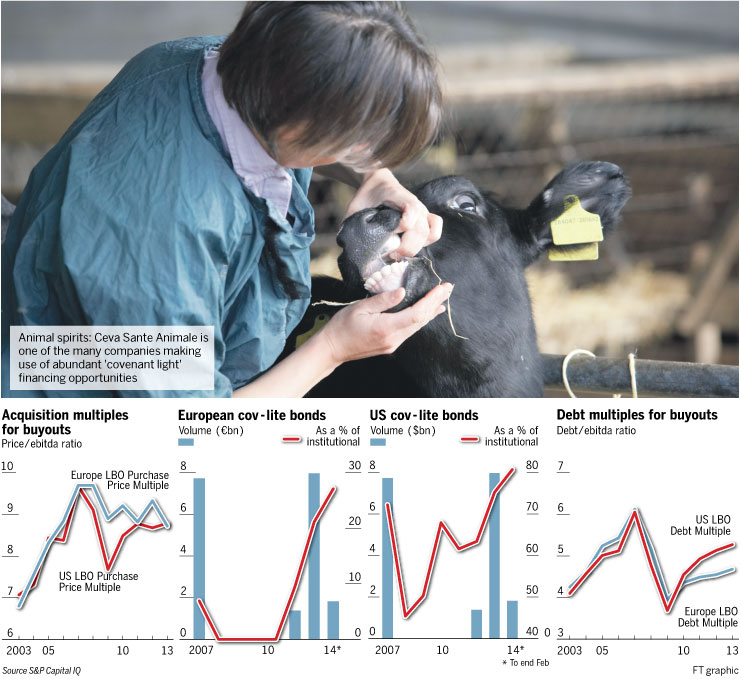

Nearly €8bn of these “cov-lite” loans were arranged last year, exceeding the €7.73bn previous peak of 2007, according to data compiled by S&P Capital IQ. Almost €2bn have been issued so far this year, representing more than a quarter of all leveraged loans sold to institutional investors, up from a fifth last year and 7 per cent in 2007.

Cov-lite loans remove the early warning signs that lenders would traditionally expect when extending credit. These include the obligation to maintain certain performance and financial ratios, which if breached trigger a default, allowing banks to request cash injections from shareholders, or a debt restructuring.

The revival of these riskier loans – which fell out of favour during the financial crisis – has alarmed some in the industry who fear a repeat of the excessive risk-taking that brought the global banking system to the brink of collapse.

Jon Moulton, the veteran British private equity executive, told the Financial Times: “Cov-lites are pretty dangerous pieces of paper for those who advance the loan.”

Recent financings have included Goldman Sachs, Nomura, Crédit Agricole and Natixis underwriting a €1bn cov-lite debt package for Ceva Sante Animale, a French animal drugmaker, which was one of the largest cases of that type of debt from a European company this year.

“Europe’s macroeconomic environment continues to improve and investors are more comfortable on sovereign risk,” Michael Masters, a London-based director at Barclays’ leverage finance syndicate, said. “Investors continue to search for yield right across the credit spectrum.”

The trend is mirroring a buoyant US market, which private equity groups have predominantly used so far to fund their European leveraged buyouts. Dollar-denominated cov-lite loans to US and European companies reached a record $260bn in 2013, or 57 per cent of the total volume, and 69 per cent more than in 2007.

This has prompted the Federal Reserve and the Office of the Comptroller of the Currency to warn that the lack of “meaningful” covenants was a sign that “prudent underwriting practices have deteriorated”.

They have in mind memories of banks including Citigroup – whose chief executive once told the Financial Times that in matter of leveraged loan frenzy, “as long as the music is playing, you’ve got to get up and dance” – taking big writedowns after markets tightened in 2007 and 2008.

In Europe, the total volume of leveraged loans is still lower than in 2007, leading to increased competition among underwriting banks.

“We haven’t had enough volumes of new deals that would allow investors to do some picking and choosing. There are so few issuances that banks are willing to be more aggressive,” Paul Gibbon, managing director at UBS’s leveraged capital markets unit, said.

In the UK, the Bank of England’s Prudential Regulation Authority has been “keeping a watching eye on developments”, according to a person familiar with the situation, though it is not doing any specific programme of work in the area. “The strength and depth of erosion of covenants in bank lending is not as strong a seen in the US,” said the person.

The one UK lender attracting particular attention is Barclays, because of its large leveraged loan business in the US. The PRA is helping US regulators to assess the riskiness of the bank lending to private equity in the North American market, as part of a wider programme being done on all lenders operating in the US.

“While the issue of a re-emergence of lending to leveraged clients is becoming a general concern requiring close monitoring, at this moment there is little evidence that would support such concern about the lending practices of European banks,” the European Central Bank said.