|

Dear Friends and All,

Willingness to be Misunderstood and the Swedish Corporate Model to Scale an Asian Wide-Moat Compounder: The Story of “Korea’s IKEA” Hanssem

“Inventing and pioneering requires a long-term willingness to be misunderstood.”

– Amazon’s Jeff Bezos

“We have decided once and for all to side with the many.. All nations and societies in both the East spend a disproportionate amount of their resources on satisfying a minority of the population.. Part of creating a better everyday life for the many people also consists of breaking free from status and convention – becoming freer as human beings. We aim to make our name synonymous with that concept too – for our own benefit and for the inspiration of others. We must, however, always bear in mind that freedom implies responsibility, meaning that we must demand much of ourselves.”

– Ingvar Kamprad wrote in IKEA’s Testament of a Furniture Dealer, 20 December 1976

Home is where the heart is. Misunderstood for over four decades, Ingvar Kamprad, 87, has moved back home on March 20 to his small town of Älmhult in a province known as the Bible belt of Sweden after leaving in 1973 for Denmark and later Switzerland in 1976 when he wrote the Testament of a Furniture Dealer. The multi-billionaire was misunderstood for years over his decision to outsource to communist Poland in the middle of the Cold War in 1961 when the Berlin Wall was just going up. Most people would not even think of doing business in the land of the enemy for fear of being branded as a traitor. Not Kamprad, who built IKEA from a garden shed selling watches, stockings and Christmas cards. It was a crucial point in building IKEA which was facing ruins when Swedish furniture dealers pressed suppliers to boycott IKEA as they were angry and envious at his low prices and growing success and they stopped filling his orders. Kamprad responded by designing his own furniture and created a covert network of suppliers to get the timber and textile he needed to scale up his flatpack DIY furniture idea. IKEA now owns and operates 349 stores in 43 countries with sales of $38 billion and 139,000 “co-workers” (the word employee is banned).

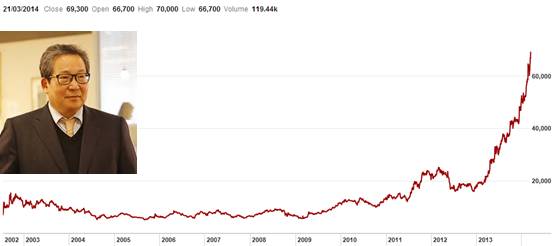

Hanssem (009240 KS), the “IKEA of Korea” – Stock Price Performance, 2002-2014

The willingness to be misunderstood in order to invent and pioneer new ventures and initiatives is what defines wide-moat compounders. Are there similar “misunderstood” stories of emerging compounders like IKEA in the 60s/70s in Asia at present? Before we highlight the story of Cho Chang-gul’s Hanssem (009240 KS, MV $1.5bn), the “IKEA of Korea”, on 20 Mar at the Singapore Management University, we catch up over lunch with Shiv Puri, the Managing Director at VS Capital, after our special dinner gathering with Moat Report Asia members in Singapore on 28 Feb. Shiv mentioned that he finds the Moat Report Asia to be interesting because we encapsulate value investing in Asia with the appropriate mental model of “Compounders vs Extractors” and that he liked our founding spirit was based upon observing up close and personal the hard-earned assets of many investors burnt badly in “extractor” companies turned out to be involved in accounting frauds. Their nice financial numbers were “propped up” artificially to lure in funds from investors and the studiously-assessed asset value has already been “tunnelled out” or expropriated. Having expounded this investment philosophy of identifying wide-moat innovators as an alternative path in the Asian capital jungles as opposed to chasing the statistically cheap and syndicate-pushed stocks and being misunderstood for the past decade, we founded the Moat Report Asia to add value to like-minded serious value investors. In addition to sharing our Bamboo Innovator framework at the 11th Value Investing Summit in Molfetta, Italy, in July as a keynote speaker, we will also be presenting at the upcoming Asian Investing Summit 2014 on April 8-9 in which famed value investor Jean-Marie Eveillard, SVP at First Eagle Investment, will also be answering live questions on investing in Asia and globally.

At a cursory glance, Asian and Swedish corporations are strikingly similar in terms of how the controlling families and business groups exploit the strong separation between ownership and control in complex pyramiding, cross-holding and dual-class share structure to establish control over several firms’ internal cash flows via a very small capital investment. For instance, the Wallenberg family has voting control over ABB (ABB SS, MV $58.3bn) even though they have a cash flow rights stake of only about 5%. This gives rise to the agency problem of tunneling or the transfer/stealing of corporate assets to the controlling owners, usually carried out via related-party transactions. Yet, why tunneling is prevalent amongst Asian firms but less so in Swedish firms is worthy of value investors to examine and reflect upon. Two large pyramidal business groups control firms amounting to roughly half of the stock market capitalization of all listed Swedish businesses, although their influence has increasingly waned. For instance, the Wallenberg group ownership sphere, which is organized around Skandinaviska Enskilda Banken (SEBA SS, MV $30.6bn) and Investor AB (INVEA SS, MV $26.9bn), held controlling positions in 42% of the market cap of the SSE (Stockholm Stock Exchange) in 1998; by 2011, their control (defined as controlling at least 10% of the votes) had declined to around 15% of the total market cap. Other core investments of the Wallenberg include Atlas Copco (ATCOA SS, MV $33.7bn), Electrolux (ELUXA SS, MV $7bn), AstraZeneca (AZN SS, MV $82bn), Husqvarna(HUSQA, MV $3.8bn), SAAB (SAABB, MV $3.1bn), SAS (SAS SS, MV $745m), NASDAQ OMX(NDAQ US, MV $6.4bn). Another outstanding super value investor is Melker Schörling whose investment company MSAB (MELK SS, MV $6.1bn) has core investments in ASSA Abloy(ASSAB, MV $19.3bn), Securitas (SECUB SS, MV $4.1bn), Hexagon (HEXAB SS, MV $11.9bn),Hexpol (HPOLB SS, $2.9bn), Loomis (LOOMB SS, MV $1.8bn).

<Article snipped>

Shiv and I discussed about the implications of the China escalating debt problems on Asian and ASEAN stocks after we have highlighted in our Jan 13 weekly insight article that a massive amount of debt will come due in April/ May 2014; back in January, market expectations were for a recovery in its economic growth engine with the reforms and that Chinese stocks were cheap bargains. The problems appear to have compounded when China central bank suspended the use of two forms of smartphone payments on Mar 14 and is considering regulations that would significantly limit the size of payments made through the Chinese internet giants Alibaba and Tencent in an announcement on Mar 18. Alibaba’s online money-market fund called Yu’er Bao launched nine months ago last June now has more investors (81m) than the country’s active equity trading accounts (77m) that attracted more than RMB500bn ($81bn) in deposits, making it the fourth largest money-market fund in the world.That means more than RMB1.3m worth of net investments flew into Yu’Er Bao every minute since it was launched in June. Investors have been attracted to Yu’er Bao and other online funds by annual interest rates of about 6% for deposits that can be withdrawn on demand, compared with the government-imposed upper limit of 3.3% that banks can offer on one-year deposits. The rate on offer for ordinary demand deposits in savings accounts at major banks is just 0.35% a year while the banks issue prime loans yielding around 6%. Such rapid expansion in a sector of the financial system that did not exist a year ago could pose risks to China’s debt-laden economy. Importantly, it provided depositors an alternative solution for their hard-earned assets and lured much-needed deposits away from the Chinese banks facing credit crunch with rising bad loans as they face refinancing woes in rolling-over their low-quality loans without the cheap funding source.

<Article snipped>

Hanssem was founded in 1970 by co-founders Cho Chang-gul and former president Kim Young-chul who started out in a 23-square-meter office in Seoul..

<Article snipped>

To read the exclusive article in full to find out more about the story of Cho Chang-gul’s Hanssem, “Korea’s IKEA” with its unique business model adapted for its home market; the origins of the Swedish Corporate Model and the super value investors in Sweden; why Sweden differs from Asia; the follow-up discussion with value investor Shiv Puri; please visit:

- Willingness to be Misunderstood and the Swedish Corporate Model to Scale an Asian Wide-Moat Compounder: The Story of “Korea’s IKEA” Hanssem, Mar 24, 2014 (Moat Report Asia, BeyondProxy)

|

|

“In business, I look for economic castles protected by unbreachable ‘moats’.”

– Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia. Together with our European partners BeyondProxyand The Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produce The Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

- Individual subscription at $1,994 per year:

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

Our latest monthly issue for the month of March investigates the Middleby of Asia commanding a dominant market share of over 80% in hypermarkets, 50% in chain outlets, 30% in 4- to 5-star hotels in China and an overall 30% in its home market. Yet, no single customer accounts for more than 5% of its revenue. Just to recall for value investors, NYSE-listed Middleby, with its sleepy and boring business, has compounded 100-fold from around $50m to $5.7bn since its tipping point in 1999. The founders of this Asian family business demonstrated clear dedication in building up the company with its wide-moat business model backed by a strong and unique distribution/marketing network in finding, winning and binding new customers to build massive brand equity and long-lasting relationships with clients over time. Their devotion to its core product for nearly 20 years results in maximum problem-solving skills, innovative strength and product leadership and hence, to ever greater customer benefit that will protect the company to consolidate the fragmented market and provide ample opportunities to continue its profitable growth. The company is currently trading at PE13e 15.8x and an undemanding EV/EBIT 10.1x and EV/EBITDA 9.5x and its growth potential based on its unique business model is not priced in. There is a structural re-rerating of niche business models with (1) diversified client base, (2) steady revenue streams, (3) lean capex requirements that creates ample free cashflow and defensive growth. Based on PE, P/CFO and EV/EBIT, the company is trading at a 40-50% discount to the foreign listed comparables despite more efficient use of assets in generating profits and cashflow. It has an attractive 7% earnings yield growing at 20% over the next 3-5 years and a 3.8% dividend yield that is supported by its strong cashflow generation ability, steady revenue stream and lean capex requirements to limit downside risks in valuation. Based on the growth plans to penetrate new product and customer segments; build its third plant in India in addition to the ones in its home market and in China; and potential bolt-on acquisition opportunities with its healthy balance sheet in net-cash position, it has the potential to double its operating cashflow in the next 3-5 years and market value could double, representing an upside potential of 100-140%.

Our past monthly issues examine:

- An emerging Asian Walgreens which is a top 3 community pharmacy operator in its home market. Walgreens is a classic neglected American compounder up over 272-fold to $54 billion from under $200m as it quietly consolidates the market. Over the decade, we observed that it is difficult to scale services-based businesses without an entrepreneurial mindset, committment and execution and the bold and unique management system of the company since 2000 allowed the pharmacists to be part-owner of the business which will lead to increased level of commitment and an owner’s mindset in growing the business for the long-term in the community. The firm has strong cash generation ability due to its negative cash conversion cycle (CCC) in the business model to help the business stay resilient during difficult times and to fund capex needs internally without straining the business model scalability as the network expands. The centralized logistics system provide regular deliveries to all of its community pharmacies enables the outlets to maximize retail space without the need to have space to keep stocks. This also enables the community pharmacies to optimize retail space to carry a wide range of products which is important as consumers increasingly have top-of-mind recall for the company as the destination to go to for their healthcare needs. Like Walgreens, the company believed in the power of embedding technology into the business model to better compete and its financial and warehousing/inventory management systems are integrated with its in-house POS (point-of-sale) system which is linked among all its community pharmacies and head office via virtual private network. The company is founded by five college friends who were somewhat frustrated that their pharmacy degrees were underappreciated and under-rewarded as compared to their medical degree counterparts even though they had studied hard for 4-5 years and had in-depth medical knowledge. They were eager to prove themselves that they are as capable, if not more so. This restless spirit to prove their capabilities resulted in them coming together to be entrepreneurs and they wish to provide the platform for similar restless pharmacists to apply their hard-earned knowledge acquired in the university. We find that this common purpose and camaraderie spirit is rare in Asian companies and makes the company unique to scale up sustainably. The company is currently trading at a EV/EBIT of 13.9x and EB/EBITDA 12.6%. In the next two to three years as the company expands its network of outlets, operating cashflow (CFO) could increase 50-60% and a re-rerating could result in a doubling in market value.

- An Asian-listed pharmaceutical company which has a dominant franchise in a neglected but growing disease and is a leader with a domestic market share of 49% in this niche segment and is the only fully-integrated player amongst the few pre-qualified WHO firms, giving it >30% EBITDA margin, better pricing power compared to the competition, and significant advantage over other players in ramping up the global business from the current 30% market share in the most-common treatment drug (vs Novartis 50%). Furthermore, the pharma company has the second-highest GP/TA (gross profit/ total asset) ratio in the industry at 56.3% and the most conservative accounting practice in the industry which “depresses” earnings relative to its peers i.e. it is the only domestic firm which expenses, and does not capitalize, all R&D. With the new plant for formulations export to US, the deepening of the niche drug franchise, growing wins in chronic pain and other niche areas and the commercialization of the potential blockbuster product of blood thinner by FY16/17, EBITDA could potentially double to $200m in the next 4-5 years, triggering a valuation re-rating to a market value of $3.4bn, a 130% upside.

- An Australian-listed company with market value $405m, EV/EBITDA 7.5x, EV/EBIT 10x, div 3%, 70% domestic market share whose management made the controversial bold decision to stop overseas exports in order to focus on cultivating the higher-margin domestic market with innovative marketing strategy and new products and is potentially doubling its supply in the next 3-5 years. It is in its 10th year of listing after piling the foundation in consolidation, investment, rationalization for its next stage. It has an all-time low debt-equity position 18.6% with healthy balance sheet. “Buffett of Nordic” recently increased position between Apr-Sep this year in the peer comparable of the company and the billionaire investor announced in Nov an acquisition of a rival in a wave of global consolidation and with the view on a sustained recovery in product prices.

- A Northeast Asia-listed company with global #1 market share leadership in 4 different products, including making the components for an innovative consumer product whose sales have climbed from $90 million to $526 million in the recent three years. The company is a hidden global consolidator with underappreciated growth. The stock is trading at PE 11.5x, EV/EBITDA 9x and generates a sustainable dividend yield 5.75%.

- A Taiwan and Southeast-Asian-listed entrepreneurial company, both with a dominant 80% domestic market share and have innovative business models to generate substantial cashflow to support both expansion and a 4-5% dividend yield.

- There is also a behind-the-scene conversation with the CEOs of the companies to understand their thinking process in building up the business.

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our existing institutional subscribers from North America, Europe, the Oceania and Asia,including professional value investors with over $20 billion in asset under management in equities, secretive Singapore-based billionaire entrepreneur who’s a super value investor and successful European multi-billion family offices. Questions range from:

- The nuances of internal dealings in Asia, including the case discussion of the recent deal in which HK billionaire’s Lee Shau-kee Henderson Land acquiring Towngas or Hong Kong & China Gas (3 HK) from his family holdings, seemingly déjà vu from the early Oct 2007 transaction when the market peak.

- The case of F&N Singapore spinning out its property unit FCL Trust and getting “free” special dividend-in-specie and the potential risk in asset swap restructuring to deleverage the hidden debt in the entire Group balance sheet.

- The dilemma of whether to invest in a Southeast Asian-listed company and hidden champion with a domestic market share of 60% due to family squabbles and a legal suit over the company’s ownership.

- Discussion of the wise and thoughtful 107-year-old Irving Kahn’s investment into a US-listed but Hong Kong-based electronics company with development property project in Shenzhen’s Qianhai zone and the possible corporate governance risks that could be underestimated or overlooked, as well as their history of listing some assets in HK in 2004.. This is also a case study of “buy one get one free” in John’s highly-acclaimed book The Manual of Ideas in which the “free” property is lumped together with the (eroding) core business to make the combined entity look cheap and undervalued. What are the potential areas that value investors need to watch out for when adapting the SOTP (sum-of-the-parts) valuation method in Asia?

- And many more intriguing questions.

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps. |