Second Chinese Bond Company Defaults, First High Yield Bond Issuer

April 15, 2014 Leave a comment

Second Chinese Bond Company Defaults, First High Yield Bond Issuer

Tyler Durden on 04/01/2014 08:01 -0400

In the middle of 2012, to much yield chasing fanfare, China launched a private-placement market for high-yield bonds focusing on China’s small and medium companies, that in a liquidity glutted world promptly found a bevy of willing buyers, mostly using other people’s money. Less than two years later, the first of many pipers has come demanding payment, when overnight Xuzhou Zhongsen Tonghao New Board Co., a privately held Chinese building materials company, failed to pay interest on high-yield bonds, according to the 21st Century Business Herald.

The company located in the eastern province of Jiangsu, missed the 10 percent coupon payment due March 28 on the notes, which it sold 180 million yuan ($29 million) of last year in a private placement.

As predicted, once Chaori Solar opened the gates for China’s default superhighway two months ago, and the realization that China will no longer bail out any and everyone, the default deluge has begun.

“In general, what we will see is a gradual unwinding of implicit government guarantee for a lot of credit products in China,” said James Zhao, chief investment officer in Beijing at the international department of CCB Principal Asset Management Co. “There will continue to be a mixture of bond defaults and too-big-to-fail, or too-entangled, cases. It’s now up to the market to find the pattern and investors will now have to figure out who is creditworthy and who is more likely to fail.”

Sino-Capital Guaranty Trust, the guarantor for the Zhongsen Tonghao security, refused to pay on behalf of the company, according to the Guangzhou-based financial newspaper.

A woman who answered the phone at Zhongsen Tonghao and wouldn’t give her name said the company couldn’t immediately comment on the matter. Two calls to Sino-Capital Guaranty Trust went unanswered.

Reluctance to bail out companies that can’t repay debt signals “regulators’ higher tolerance for corporate bond defaults amid financial market reforms, which is in line with the current central administration’s shift to adopt more market-oriented policies,” Moody’s Investors Service said in a report on March 7.

The number of Chinese companies whose debt is double their equity has surged since the global financial crisis, suggesting more defaults may come. Publicly traded non-financial corporates with debt-to-equity ratios exceeding 200 percent have jumped 57 percent since 2007. Chaori Solar may become China’s own “Bear Stearns moment,” prompting investors to reassess credit risks as they did after the U.S. securities firm was rescued in 2008, according to Bank of America Corp.

“SME private bonds are now facing relatively high risk,” said Pengyang’s Yang. “We expect more defaults to come in this area, especially those private enterprises without guarantees.”

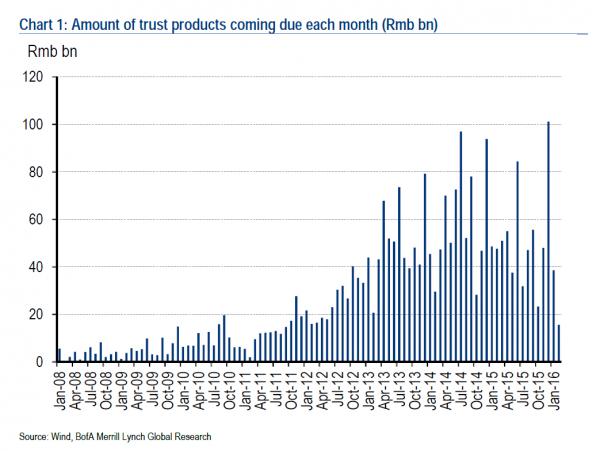

We have written extensively about the imminent funding and liquidity threats facing China’s real estate developers following the collapse two weeks ago of another closely held company based in neighboring Zhejiang province, property developer Zhejiang Xingrun Real Estate Co. This in turn has sent shockwaves throughout the Chinese housing market, and especially the offshore cash parking version, where recently we have witnessed the start of a mass liquidation wave in Chinese offshore property haven, Hong Kong. However, it now appears that the funding danger is becoming more pervasive than even we expected, and as a result a major adverse risk and rate repricing is imminent.

And while this default came out of the blue, the one we are waiting for is that of the Magic Property which we profiled before:

31 Mar 2014, Rmb196mn borrowed by Magic Property & arranged by CITIC Trust

Details: invested in an office building in Chongqing. The Chongqing developer ran into financial problems in mid-2013. CITIC Trust tried to auction the collateral but failed to do so because the developer has sold the collateral and also mortgaged it to a few other lenders.

Potential outcome: The developer and the trust company may share the repayment.

Reasons: 1) When CITIC Trust sold the product, it did not specify the underlying investment project. 2) The local government has intervened, fearing social unrest. A local buyer of a unit in the office building committed suicide as he/she could not obtain the title to the property due to the title dispute between the trust and the developer.

We can’t wait to see the look on Chinese investors” faces when they too learn the term re-re-re-re-rehypothecation.