Factoring in China’s Machinery Maker Blues; Chinese heavy equipment maker Zoomlion is suffering as customers delay making good on what they’ve bought. Now the banks want a piece too

April 16, 2014 Leave a comment

Factoring in China’s Machinery Maker Blues

ABHEEK BHATTACHARYA

Updated April 1, 2014 5:40 a.m. ET

At the foundation of China’s investment-driven economy lies concrete. So it doesn’t bode well that the makers of concrete and other construction equipment continue to suffer.

State-owned Zoomlion, 000157.SZ +1.43% a leading maker of the machinery used in China’s building spree, recorded a 20% fall in sales in 2013. Concrete equipment, which makes up nearly half of the company’s sales, was particularly hard hit.

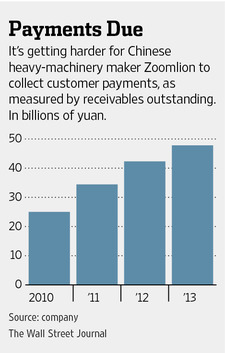

A deeper dive into Zoomlion’s books raises more worries. Its receivables jumped to 124% of revenue at the end of 2013 from 88% a year earlier, meaning it’s selling equipment without immediately getting paid. The net cash it earned from operations almost evaporated to just 43 million yuan ($6.9 million) in 2013 from 2.6 billion yuan the year before.

What Zoomlion does with its receivables also raises red flags. Like others in China, Zoomlion sells receivables to banks in return for cash up front, a practice known as “factoring.” Zoomlion says it sells a lot of receivables “without recourse”—that is, the final responsibility to collect payments shifts to the bank. Zoomlion then moves the risk of collecting those payments off its books.

Yet Zoomlion’s filings confusingly say the company is still on the hook for receivables it says it sold “without recourse,” notes Sun Hung Kai Financial’s Vik Chopra. So far, this has been a theoretical concern. But now the company says it had to pay 673 million yuan to buy back equipment from banks to whom it had earlier sold such non-recourse receivables.

The company says the banks repossessed this equipment, likely because the end-customer finally defaulted. It’s also possible banks are getting tougher on the factoring trade. Last year, regulators told banks to better monitor such lending.

It’s hard to gauge the total exposure to these off-balance sheet items. The company factored 30.1 billion yuan of “non-recourse” receivables the past two years, with the bulk of that in 2012. Easier to see are the 47.8 billion yuan of receivables Zoomlion keeps on its books, which are now equivalent to 114% of shareholder equity. Roughly 10% of these on-the-books receivables are past their due date, compared with 5% in 2012.

Zoomlion’s receivables should make investors cautious. With China’s economy slowing and cracks in China’s property sector widening, customer payments could prove elusive