Asia Joins Trend Toward Floating-Rate Bonds; Issuance at Fastest Pace on Record to Catch U.S. Demand

April 22, 2014 Leave a comment

Asia Joins Trend Toward Floating-Rate Bonds

Issuance at Fastest Pace on Record to Catch U.S. Demand

FIONA LAW

April 14, 2014 12:51 a.m. ET

To take advantage of demand from U.S. investors worried about rising interest rates, Asian companies are changing the way they raise cash, selling floating-rate debt at the fastest pace on record.

Unlike traditional bonds with fixed annual interest payments, these types of notes have coupons that usually adjust every quarter to track market rates. As a result, they offer better protection from rising interest rates.

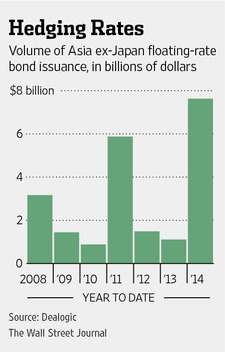

Not counting issuance from Japan, sales of floating-rate bonds have surged to $7.63 billion so far this year in Asia, a year-to-date high and nearly seven times the $1.11 billion at this time last year, according to Dealogic, a data provider. Companies in the market include China Petrochemical Corp., or Sinopec Group, which sold $2 billion worth of floating-rate bonds earlier this month, the biggest offering of its kind so far in Asia and the first by a Chinese state-owned company. The Japanese bank Mizuho Financial Group Inc. 8411.TO +1.01% raised $500 million in floating-rate debt as part of a $3 billion bond offering last week.

Snapping up the bonds are mostly large U.S. fixed-income money managers, who worry that investments in fixed-rate bonds will lose value if yields on U.S. Treasury debt head higher. Bond prices are expected to fall as the Federal Reserve reduces large-scale buying that had supported the market. Such a shift would result in higher yields because yields and prices move in opposite directions.

One such buyer is Pacific Investment Management Co., manager of the world’s largest bond fund, which invested in a $500 million offering in January by Kookmin Bank, South Korea’s largest lender.

“Some of our participation was motivated by the floating-rate nature of the bond,” said Scott Mather, a deputy chief investment officer at Pimco, which manages almost $2 trillion.

However, a bigger driver was the bond’s attractive value, he said. The bond yielded 0.875 percentage point above the benchmark three-month London interbank offered rate, or Libor.

“There appears to be increasing U.S.-based investor appetite for Asian [floating-rate] bonds,” said Mr. Mather, in Newport Beach, Calif.

Asia has been catching up with a global trend toward floating-rate bonds. U.S. issuance jumped 30% to $344.23 billion last year, according to Dealogic.

The trend is continuing this year with a 13% rise in new floating-rate bonds in the U.S., while Europe, the market with the largest issuance of these bonds, saw a pickup of 5%.

The Asian boom also comes as U.S. bond investors, encouraged by signs of health in the domestic economy, have scooped up debt, boosting prices and driving yields lower. These buyers are reaching out to Asia to capture the higher yields companies there are offering.

“Vis à vis U.S. domestic corporates with the similar rating, our Asian peers are offering a significant incremental” value, said Devesh Ashra, head of Asia debt syndicate at Bank of America BAC +1.46% Merrill Lynch.

To be sure, fixed-rate bonds still dominate the global debt landscape. But their floating-rate counterparts are increasingly popular. Union Bancaire Privée, a Geneva-based private bank with $100 billion in assets under management, says it has seen a huge increase in clients’ demand for floating-rate notes, known as FRNs.

“We have two funds dedicated to invest in FRNs, and we saw money inflows double last year,” said Philippe Graub, who co-manages both funds. He says the bonds are attractive as their tenors are typically no more than three years, meaning investors are less vulnerable as the Fed reduces its bond buying. The central bank’s efforts to scale back its easy-money policies tend to have the biggest impact on debt that matures in 10 years or longer.

UBP bought some of Kookmin Bank’s bond.

The borrowers are also benefiting because they get to tap into the large pool of U.S. investors. For banks especially, selling bonds with variable borrowing costs can be a plus, given that they lend the proceeds at floating rates, profiting from the gap between the two. The opportunity to issue the debt didn’t arise until the middle of last year when worries started to mount about interest rates picking up.

Floating-rate bonds “always work better for us because we provide loans to Korean companies at [floating] Libor-based rates,” said Hee-Sung Yoon, head of the international finance department at the Export-Import Bank of Korea in Seoul.

The deals were driven by interest from the U.S. because investors there are more sensitive to interest-rate movements, Mr. Yoon said. Interest is also increasing from Asian buyers, he said.

The state-owned bank, known as Kexim, sold a $750 million floating-rate note in January. U.S. buyers took up 70% of the debt, as well as 62% of Sinopec’s $2 billion in floating-rate notes. It isn’t known how much of Mizuho’s offering last week was sold to North America.

Mizuho public-relations manager Masako Shiono said the bank opted to raise debt at adjustable rates, in addition to fixed rates, to match an increasing need for this debt among investors. “This is one of the ways to diversify our means of fundraising,” she said.

Floating-rate notes “tend to attract [a] unique pool of liquidity,” said Duncan Phillips, head of Asia-Pacific debt syndicate at Citigroup Inc. C +4.36% He expects more Asian borrowers to follow the route.