Housing Trouble Grows in China; Overbuilding by Real-Estate Developers Leaves Smaller Cities With Glut of Apartments

Housing Trouble Grows in China

Overbuilding by Real-Estate Developers Leaves Smaller Cities With Glut of Apartments

BOB DAVIS and

ESTHER FUNG

April 14, 2014 10:30 p.m. ET

CHANGZHOU, China— Wu Xuesong, a professor in this city on the Yangtze, says he doubled his money on an apartment he bought as an investment some years back and is ahead on a second.

Buy a third? Forget it.

Mr. Wu slides open a dining-room window and points to the dark shadow of a new apartment complex, where only a handful of lights are on. “No one lives there,” he says. “That shatters my confidence” in China’s long-thriving real-estate market.

Economists have worried for years that China is setting itself up for a housing-market bust. In big international cities like Beijing and Shanghai, prices continue to rise. But evidence is mounting that in dozens of third- and fourth-tier Chinese cities rarely visited by foreigners, overbuilding is out of control and a major property-market slowdown is now under way.

The 200 or so Chinese cities with populations ranging from 500,000 to several million account for 70% of the country’s residential-property sales. In many of these cities, developers are slashing prices and offering freebies such as kitchen furnishings and parking spaces as they try to work through vast gluts of unsold property. Protests are breaking out among buyers angry that their investments are losing value.

Data in some of these smaller cities is scarce. But in 100 cities tracked by Nomura HoldingsInc., 8604.TO +0.66% 42% of those classified as Tier 3 and Tier 4 saw housing prices decline in March from February. Home construction in such cities is racing well ahead of population growth, says Beijing research firm Gavekal Dragonomics, as developers continue to build new projects without buyers.

A dramatic housing collapse such as the U.S. suffered a few years ago isn’t thought likely here. Chinese families don’t borrow as heavily for home buying as Americans, putting at least 30% down. China doesn’t have sketchy mortgages like those that infected the U.S. market at its peak, nor home-equity loans that let owners finance shopping sprees on the value of their homes. Chinese financiers haven’t put together arcane mortgage-backed securities such as those that blew up in the U.S.

Yet even with market strength holding up in the most prominent cities, the overall value of Chinese housing sold in the first two months of 2014 declined 5% from a year earlier, government statistics show. Private-sector data indicate the decline continued in March.

Price drops might seem a normal market response to oversupply, but when it comes to housing, the phenomenon isn’t benign. China increasingly depends on real estate to drive growth.

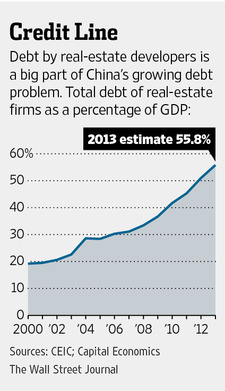

The construction, sale and outfitting of apartments accounted for 23% of China’s gross domestic product in 2013, Moody’s MCO +1.79% Analytics calculates. That is up steeply from 10% in 2006 and is higher than American housing’s share of GDP reached during the height of the U.S. housing boom in 2006, Moody’s says.

The housing troubles add to other headaches for the world’s second-largest economy. They come at a time when debt in China is climbing as rapidly as it was in the U.S., Europe, Japan and South Korea before their economies cratered in years past. And China’s growth, while still healthy by world standards, has slowed to its weakest since the Asia financial crisis of the late 1990s, amid less-robust demand both at home and abroad for Chinese goods.

Chinese state television aired a series this month on difficulties faced by home buyers and property developers. An owner in Shenmu County, in the north, said she couldn’t afford to pay the mortgage on her apartment but couldn’t sell it, either, because so many others were for sale.

The finances of some cities and developers are being affected. China’s local governments depend on land sales to developers for about 40% of their revenue. Now those sales are bringing in less cash.

After the city of Fenghua in eastern China cut the price of land, developer Zhejiang Xingrun Real Estate Co.—which had incurred higher land costs—found it tough to sell apartments and make payments on its debt, which the city website put at nearly $600 million. Municipal officials say they are trying to stave off a bankruptcy by the developer that could tarnish the city’s reputation. Principals of the developer couldn’t be reached for comment.

As developers grow short of money, some are using apartments instead of cash to pay their bills to construction companies. Anne Stevenson-Yang, research director at J Capital Research in Beijing, who crisscrosses China checking out property developments, sums up the real-estate market in China’s smaller cities “an incredible house of cards.”

Further weakness could mean trouble for construction companies and appliance and commodity producers. Furniture and appliance sales in China have been slowing along with the weaker pace of apartment sales. Also potentially affected are businesses that use real estate as collateral to get new loans; China’s banks rely on property holdings as the main collateral securing loans.

One risk is that consumers who are accustomed to seeing steady gains in their homes’ value pull back on spending. This is a danger because an unusually high percentage of Chinese household wealth is tied up in real estate—about two-thirds, estimates economist Li Gan at Texas A&M University. Americans, at the peak of the U.S. housing boom, had only about half that much of their family wealth in real estate. The figure is high in China partly because of few appealing investment alternatives, with the domestic stock market performing poorly for years and interest on savings deposits at banks fixed at a low rate.

Take a drive through China’s third- and fourth-tier cities and these issues are all too visible. Many cities are ringed by row after row of empty apartment buildings that reach 20 stories into the sky. At night, they are dark save for blinking red lights on top to warn airplanes.

Analysts have long taken note of Chinese “ghost cities”—sprawling new neighborhoods nearly devoid of inhabitants. These have sometimes been seen as anomalies. But over the past few years, building has proceeded at such a blistering pace that Nicole Wong, a real-estate analyst in Hong Kong for CLSA, figures the pace of construction in third- and fourth-tier cities needs to fall by half between 2013 and 2020 to get supply and demand somewhat back in balance.

In Yingkou, a dusty city of 2.4 million in China’s frigid northeast, the only sign of life in one complex of 20-story buildings is a small satellite dish in a first-story window. Zhou Mingqi says he is paid about $290 a month to live there, by owners of three units who want to make sure their properties aren’t occupied by squatters or the fixtures stolen.

The project, called Expo Garden, began in 2010 and was supposed to be finished by 2013. As of last month, only eight of the planned 16 towers had been built. A recent visit found grounds with rutted roads, no sign of workers and not even any billboards advertising sales.

City officials said the builder temporarily suspended construction because of winter. A representative of the developer, Xizang Zangye Group, said construction would resume in the spring. Other local developers said the city was trying to work out a deal to keep the project alive.

In Yingkou, real estate’s problems have become the city’s as well

. Its land-sales revenue has fallen by about 40% in the past three years.

China’s private real-estate market dates only to the late 1990s, when the Communist Party started to privatize housing owned by state-owned companies. The market went into overdrive in 2009, as Beijing told banks to start lending heavily to spur growth and make sure China wasn’t dragged down by the global financial crisis.

Around the same time, Beijing tightened restrictions on real-estate purchases in first- and second-tier cities to try to keep prices in those places from skyrocketing too high. (Four cities—Beijing, Shanghai, Guangzhou and Shenzhen—are considered first tier, and roughly two dozen second tier.)

The result of the twin policies was that money flowed heavily to medium-size and smaller cities. According to Citigroup, C +4.36% 12 provincial capitals are building an average of nearly 15 “new towns” each, meaning massive high-rise apartment projects on their outskirts.

One level below the provincial capitals, 133 cities that are the capitals of Chinese prefectures are building a total of 200 of these apartment complexes. Several dozen main county cities are doing the same.

Changzhou—the place where Prof. Wu has made money on past real-estate buys but now is afraid of the market—is a textile-exporting city of 3.6 million. When stimulus money started flowing in 2009 and 2010, the city decided on a makeover. Aiming to turn into a producer of advanced materials and high-tech goods, it started building a subway and blocked out a section for higher-end housing.

But Shanghai is only an hour away by bullet train. People with ambition and money often head to the megacity, crimping housing demand in Changzhou.

In the showroom of a cream-colored development of villas and high-rises in Changzhou, four young Ukrainian women in white fur stoles act as greeters. Ball gowns hang in the closets of the marble-filled model apartments. An outdoor swimming pool is decorated with statues of nymphs.

It isn’t enough to tempt many to buy. There are plenty of other opulent developments nearby.

“If all the developers here stop building right now, there’s still enough apartments to last the local and migrant populations for another six to eight years,” says a discouraged sales agent.

Faced with weak sales, the complex’s developers publicly slashed apartment prices by 40% in late February. City housing authorities called them in to urge them to be more discreet, according to competitors, who say the city didn’t want to get a reputation as a bad place to invest. Agile Property Holdings Ltd. 3383.HK -1.31% , a public company that is developing the project with a privately owned partner, declined to comment. City officials didn’t respond to requests for comment.

The developers kept the discounts but stopped advertising them.

Other developers felt they had to respond. Nearby, Feilong Road cuts through construction sites filled with unfinished apartment towers that reach as tall as 30 stories. Billboards for one project promise discounts of about 20%. Across the street, another developer offers free parking and about $24,000 off the final price.

At one project, sales manager Susan Yang says her bosses are considering “stealth price cuts”—rebates, of maybe 30%—that would keep the development competitive without undercutting its high-end image.

The real-estate oversupply “gives me a headache,” Ms. Yang says. “People expect prices will fall.”

On March 21, protesters lined up in front of Phoenix Lake Gardens, a middle-class complex of 20-story apartment towers in northern Changzhou. They put up banners, trashed architectural models in the showroom and demanded refunds from the developer, Wharf (Holdings) Ltd. 0004.HK -0.61% Wharf had cut prices by as much as 20% after these protesters bought their apartments, making their purchases suddenly worth less.

David Wan, 25, said he had put $40,000 down on a two-bedroom apartment just a week before Wharf cut the price. “The salesperson told me that prices wouldn’t fall,” he said.

Another buyer said she and her husband sold their hometown residence 100 miles away and borrowed from relatives for a 40% down payment here, only to see the price for similar apartments later slashed.

The buyer, who would give only her surname, Xu, was especially angry that the developer brought in guards to block the protesters from the showroom. “We are their earliest home buyers, and this is how they treat us?” she said.

Wharf defends using the guards, who a spokesman said “wouldn’t touch the customers unless they behaved unreasonably.” The company said it cut prices to clear inventory, which it called “normal market behavior.”

A few blocks away at another Wharf project, a police officer tried to explain to a demonstrator the new reality of housing in China.

“You bought a private home,” the policeman told the irate protester. “Prices will go up or down. It’s just like investing in the stock market.”

Apr 15, 2014

Too Much of a Good Thing: A China Property Glut FAQ

Tim Franco for The Wall Street Journal

China’s smaller cities are now the scene of a housing glut, which could undermine China’s growth. What are the possible consequences? How are developers reacting? Is the government doing anything about it?

Below WSJ reporters Esther Fung and Bob Davis answer those and other questions.

Why are the recent price cuts so bad? Isn’t this just the market at work—less demand, ergo lower prices?

The same could have been said for the U.S. in 2007. Falling prices in Las Vegas, Bakersfield, Miami were just the market at work. The problem is that if prices fall too far, they don’t invite more people to invest in property. Just the opposite. Would-be buyers keep their wallets closed, fearing that the value of a home will go down in value.

That’s particularly a problem in China, where people have thought for 20 years that real estate prices can only go up in value. If that psychology switches, it’s a huge problem.

There was concern that the property bubble had burst in 2011. What’s different now?

In 2011, the big worry was escalating prices in China’s major cities putting apartments out of the reach of all but the rich. The central government implemented property curbs, such as limits on multiple home purchases, to rein in speculation and frothy prices. After two tough years for developers, prices started heading up again smartly last year.

What makes the current problem different is that a) the problem is more widespread, hitting lots of small and medium-sized cities, b) the issue is a glut rather than rising prices, and c) China’s finances are tied ever more tightly to real estate.

Since 2008, debt in China has grown at a pace similar to the U.S, Europe, Japan and South Korea before they fell into deep recessions. One big reason for the run-up in debt is lending to real estate developers. If developers can’t afford to make payments on their loans because they can’t sell enough apartments, China has a big problem.

Speaking of which, how are developers paying their bills?

Many construction companies are getting paid in apartments as developers become more and more cash-strapped, according to Zhou Liping, a property consultant at Jiangsu Lianmeng Property Consultancy. “It’s quite common,” he said, adding that some of these construction companies then use the apartments as collateral when they take on bank loans.

Are there signs of construction workers losing their jobs?

Certainly it’s a danger. Unfortunately, unemployment data is unreliable in China and it isn’t counted by occupation. So far, there is no sign of widespread job loss. There are still more jobs than workers seeking jobs, largely as a result of demographic changes that are reducing the size of the Chinese workforce.

What are some signs that the growing glut is having economic ripples?

Copper prices have been falling since 2010, with analysts blaming slack demand in China as one reason. Copper is used in roofs, gutters and building expansion joints. Meanwhile, ArcelorMittal, the world’s largest steelmaker, has forecast slower growth in Chinese steel demand this year due to more muted construction demand growth.

Retail sales growth has also slowed recently, due in part to falling growth in sales of appliances and furniture, both linked tightly to apartment purchases.

What is the government doing about it?

The central government has indicated that it would allow local governments to adopt their own market regulations rather than implement a one-size-fits-all policy.

In some areas, local governments are trying help out. In Fenghua, government officials are trying to stave off a default by a local developer. In Changzhou, the government has been trying to keep discounts to a minimum to prop up the housing market. In Yingkou, the government has reduced fees and taxes for new purchases and made it easy for new buyers to get the residence permits necessary to obtain social welfare benefits, including public education for their children. So far, these measures have had only a limited impact on boosting sales.

Does this mean developers will finally start to cut back on their headlong, hell-for-leather building?

Some of China’s largest developers are now trying to focus again on China’s biggest cities, where demand is stronger. But why do developers keep building in problem cities despite obvious lack of demand? Why did U.S. developers do the same thing? Developers are optimists and salesmen by nature. Each thinks that its project will thrive even as others don’t.

According to Nomura, profits for a group of 142 listed property developers in China rose 581% between 2006 and 2012 and never fell during any of those years. Other non-financial companies saw profits rise 64% during that same period and profits sometimes fell year-to-year for that group.

“China’s real estate developers are behaving like internet start-ups,” says Mark Williams, a China economist at the Capital Economics in London. “They’re focusing on grabbing market share in a growing market, but the smaller and medium-sized cities they are in aren’t growing rapidly.”