The Unlikely Ascent of Jack Ma, Alibaba’s Founder; Alibaba Bets on a Growing Chinese Economy and New Consumers

May 11, 2014 Leave a comment

The Unlikely Ascent of Jack Ma, Alibaba’s Founder

By NEIL GOUGH and ALEXANDRA STEVENSONMAY 7, 2014

HONG KONG — The first time Jack Ma used the Internet, in 1995, he searched for “beer” and “China” but found no results. Intrigued, he created a basic web page for a Chinese translation service with a friend. Within hours, he received a handful of emails from around the world requesting information.

It was an introduction to the power of the web that would drive Mr. Ma to create the Alibaba Group four years later.

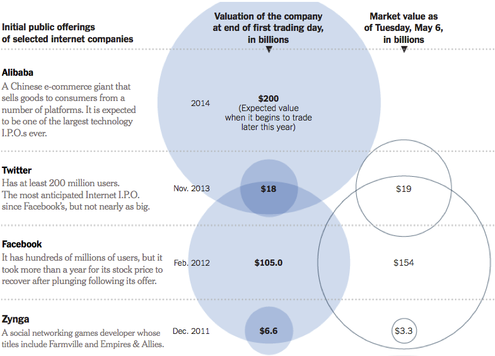

Today, Alibaba is China’s largest online retailer, with merchandise volumes that lag only Walmart, worldwide. The e-commerce giant is also moving forward with plans for a stock sale that is expected to rival Facebook’s $16 billion offering two years ago. If successful, the deal would help vault Alibaba and Mr. Ma, who owns 8.9 percent of the company, to the highest ranks of technology industry titans.

Mr. Ma’s ascent to dot-com billionaire is remarkable for not following the traditional script. Unlike Facebook’s Mark Zuckerberg, Apple’s Steven P. Jobs or Microsoft’s Bill Gates, Mr. Ma, 49, has no background in computing and professes not to understand technology. Raised during China’s Cultural Revolution, Mr. Ma began his career as an English teacher.

Instead, his role at Alibaba has always been as the company’s main strategist, a flamboyant motivator in chief to his staff and a relentless opponent to those who have competed against him. Alibaba’s two main websites, Taobao Marketplace and Tmall.com, now account for 60 percent of the packages shipped through the Chinese postal system.

“He effectively represents millions of people who now depend on Alibaba for their livelihood,” said Duncan Clark, who has known Mr. Ma since the late 1990s and is the chairman of BDA China, a consulting firm in Beijing that focuses on the digital and consumer sectors. “That’s a constituency. He’s a politician with a small ‘p.’ ”

He has also proved to be a serial disrupter — an outsider with a knack for creating new markets by reimagining old industries like retailing or finance. Alibaba and Mr. Ma are shaking up some of China’s most staid, state-dominated industries, starting ventures in banking and finance and mobile phone communications. He is even moving into the department store business and film production.

“Innovation in many industries has been triggered by outsiders,” Mr. Ma wrote last June in an opinion article in The People’s Daily, the official newspaper of the Communist Party — an unusual move for a private sector entrepreneur.

He was putting the country’s state banks on notice. Publication of the article coincided with the start of Yu’e Bao, a high-interest money market product that Alibaba initiated to attract investment from its customers’ online payment accounts. As of February, 81 million people had signed up for the product, which had $40 billion in assets under management.

“The finance industry needs a disrupter, it needs an outsider to come in and carry out a transformation,” Mr. Ma wrote in the article.

He brings his own flair to the role.

At a 2009 stadium rally to celebrate the anniversary of Alibaba, he emerged on stage wearing a waist-length blond wig, a black leather jacket with red flame and metal stud accents, sunglasses and lipstick. Raising a microphone, he ripped into a stilted rendition of “Can You Feel the Love Tonight?,” eliciting cheers from the crowd of 16,000 employees.

Since the beginning, Mr. Ma has shown a knack for thinking differently.

At a time when few Chinese households had their own computers, Mr. Ma in 1995 made the decision to leave teaching to set up an online business. In his hometown, Hangzhou, an eastern city about 100 miles from Shanghai, Mr. Ma established one of the country’s first officially registered Internet companies, a business index site called China Pages. Cui Luhai, who was then running a computer animation business, met with Mr. Ma at the China Pages office to learn more about his plans for the website.

“I can still remember the first scene I saw when I walked into his office,” said Mr. Cui, today a lecturer in new media at the China Academy of Art. “It was a pretty empty space with only one desk set up in the middle of the room. There was only one very old PC desktop surrounded by a lot of people,” he said. Mr. Ma, it turned out, had spent much of his money on registering the business and appeared to have little money left for hardware.

Mr. Ma struggled in his early efforts to get government support for his new venture.

In a memoir-style documentary about Alibaba and Mr. Ma called “Crocodile in the Yangtze,” Porter Erisman, a Mandarin-speaking American who worked at Alibaba from 2000 to 2008, presents footage of one of many visits Mr. Ma paid to officials in Beijing in the mid-1990s. Mr. Ma appears in a button-down blue denim shirt, sitting over a boxy old laptop computer in a smoky government office and explaining his business to a bespectacled official in jacket and tie.

“Nowadays, foreigners can use computers from any desktop to find products from around the world,” Mr. Ma explains to the official. “They can order directly from Hong Kong, Taiwan, Singapore, but they can’t order anything from China because right now there’s nothing from China on the Internet,” he says. “I hope the various departments will support us.”

But Mr. Ma’s pitches were rebuffed. He soon left China Pages in 1997 to work at a unit of China’s Commerce Ministry helping to create websites. In early 1999, he struck out on his own again, to start Alibaba.

The company’s first site, Alibaba.com, was a business-to-business marketplace that connected Chinese exporters with overseas buyers. Unlike most Chinese websites of the day, it was not a clone of Western companies.

In 1999, the company lured Joseph C. Tsai, a Taiwan-born former lawyer who had been educated at Yale and was working in a private equity business in Hong Kong. Together, Mr. Ma and Mr. Tsai brought in Goldman Sachs and SoftBank as investors.

Early on, Mr. Ma honed his skills as a strategist. He began Taobao, the company’s consumer-to-consumer platform, in 2003, at a time when eBay’s Chinese unit dominated the business. Fighting for market share, Mr. Ma decided to keep Taobao free, although it was hemorrhaging money.

“With eBay, he liked looking foolish and stupid,” says Mr. Erisman, the filmmaker. “From a Wall Street investors’ perspective, he was willing to run Alibaba into the ground to defeat eBay — the only thing worse than a smart competitor is a crazy one who is willing to just spend all their money with no hope of making profit.”

It worked. At a news conference in October 2005, Mr. Ma told reporters that Taobao had gained nearly 70 percent of the market share for online shopping in China. “Pretty soon we’ll be the only one left. EBay’s days are numbered,” he said. In 2006, eBay announced it was effectively leaving the China market and folding its operations into an Internet company controlled by Li Ka-shing, the Hong Kong billionaire.

“I had always wished that I was born in a period of war. I could have been a general,” Mr. Ma once said of his youth. “I thought about what I could have achieved in war.” Mr. Ma has had his share of boardroom battles. In 2011, an initial partnership with Yahoo formed in 2005 was briefly derailed. Mr. Ma transferred one of Alibaba’s most profitable businesses, the online payments unit Alipay, into a separate business under his control without formal approval from Alibaba’s board, where SoftBank and Yahoo had seats. When news of the transfer broke in May 2011, it brought an angry response from outside investors in Alibaba and Yahoo.

Mr. Ma argued that it was necessary to get a government license for Alipay, because Beijing did not want foreign investors controlling online payment businesses in China. “If Alipay were illegal or didn’t get the license, Taobao would be paralyzed,” Mr. Ma said at the time. “If Taobao were paralyzed, how could Alibaba reform and develop?”

Alibaba, Yahoo and SoftBank settled their differences over the issue, but not all shareholders were pleased. The hedge fund manager David Einhorn pulled his investment in Yahoo, saying the spat “wasn’t what we signed up for.”

Mr. Ma displays few regrets for his aggressive approach. In regard to the 2011 episode, he compared his decisions with those made by Deng Xiaoping, China’s paramount leader during the government’s deadly crackdown on Tiananmen Square protesters on June 4, 1989, which is widely referred to in China as the “6/4 incident.”

“As a company C.E.O., no matter if it’s the Alibaba incident, no matter if it’s splitting off Alipay, at that point, it’s just like Deng Xiaoping during 6/4,” Mr. Ma was quoted as saying in Hong Kong’s South China Morning Post in July. “As the country’s highest decision maker, he demanded stability. He needed to make this kind of cruel decision.”

As the company moves toward an initial public offering, Mr. Ma seems focused on his legacy.

He remains a hands-on executive chairman and oversees strategy at Alibaba, but in May 2013 he stepped down from his role as chief executive. The next day, he announced that he had been appointed the chairman of the Nature Conservancy’s board of directors for China. He has grown increasingly concerned over rampant pollution of the soil and water in China, something he has partly blamed for his father-in-law’s recent death from cancer.

In late April, Mr. Ma and Mr. Tsai, a co-founder, announced that they would donate shares representing 2 percent of Alibaba’s stock — a grant worth several billion dollars — to charitable trusts that would finance initiatives in the environment, medicine and education. Such a large donation is seldom seen in China, and the move was cheered by other prominent philanthropists, including Mr. Gates of Microsoft, Warren E. Buffett and Michael Bloomberg, the former mayor of New York.

Mr. Ma “wasn’t the type of person who starts a business keeping 90 percent of the equity for himself and really hoarding all of the wealth and riches,” said one Western executive who has known him for over a decade, declining to be named because of his company’s policy against speaking publicly about business contacts.

“In the earliest days, when Alibaba.com was first forming, he was giving equity to all of the high school students who were working with him,” said the executive. “He was bringing everyone along.”

Alibaba Bets on a Growing Chinese Economy and New Consumers

MAY 7, 2014

When American tech upstarts float their companies on the stock market, they often sell investors on a familiar dream — “disrupting” an existing industry. It doesn’t matter if the industry is advertising, software, commerce or some other sector. The start-up will usually claim that its business is a great technological leap forward that will greatly lower costs and improve service for customers and leave rivals unable to respond. Therefore, buy some stock.

Alibaba’s I.P.O. filing breaks with that well-worn theme. Instead of promising to disrupt an existing market, the Chinese e-commerce giant wants to do something far more straightforward, but potentially far more lucrative — insert itself at the center of a new, already expanding market being forged by powerful economic and cultural forces far beyond the company’s control.

That new market is China itself, particularly its ascendant middle class and its growing appetite for spending rather than saving.

Instead of disruption, Alibaba is betting on existing trends staying more or less the same: that China will continue to change into the world’s largest consumer gold mine, and Jack Ma, Alibaba’s charismatic co-founder and chairman, will continue to sit at the apex of the consumerist revolution.

Alibaba’s long-term goal highlights the difference in scope between Chinese Internet firms and their American counterparts. You may think of Jeffrey P. Bezos, Amazon’s chief executive, as an ambitious man, but he is really only betting that in the future, Americans will shift some of the dollars they are already spending from offline stores into his online store. He isn’t betting that Americans will start spending twice as much on everything as they do now.

That is precisely Mr. Ma’s bet. And as investors weigh Alibaba’s stock offering, they will have to consider which approach — Amazon’s disruption or Alibaba’s going along with an existing trend — is better.

The numbers seem to be on Alibaba’s side. “Our business benefits from the rising spending power of Chinese consumers,” the firm says in its filing.

The crux of Alibaba’s pitch to investors is that Chinese customers will begin to act much more like American customers. Today, much of the Chinese population doesn’t spend very much money compared with their counterparts in the West. Only about a third of China’s gross domestic product is made up of consumer spending, significantly lower than the consumption rate of other countries. By comparison, about two-thirds of the United States’ economy is made up of consumer spending.

Mr. Ma is counting on these habits changing in his favor. Alibaba is betting that the Chinese will continually increase their spending and that a huge pool of new money will flood through China’s economy.

Every economic metric suggests that is a very good bet. According to a recent report by McKinsey & Company, China’s middle class will continue to grow at a staggering pace well into the next decade. “The evolution of the middle class means that sophisticated and seasoned shoppers — those able and willing to pay a premium for quality and to consider discretionary goods and not just basic necessities — will soon emerge as the dominant force,” the report states.

The McKinsey researchers noted that in 2000, just 4 percent of urban Chinese households earned a middle-class wage. By 2022, the study predicted, more than 75 percent of urban households will have joined the ranks of the middle class, with income among that group twice as much as it is today. The growth of this vast new market is occurring across the country and many of these newly wealthy people are hooked on online shopping.

“You’re really seeing consumer behavior change in all kinds of ways in China,” said Kelland Willis, an analyst who studies global retail trends at the research firm Forrester.

While the growing middle class has resulted in a growing population that can afford to shop, Ms. Willis said that many newly wealthy Chinese had been initially wary of spending money in the new ways that the Internet allowed for. Alibaba’s genius has been in recognizing and constantly adapting to society’s evolving views about shopping. The company has been adept at finding the reasons that people might be suspicious about spending money, then looking for novel fixes.

“What you see them doing is trying to understand exactly what the Chinese consumer wants and then experimenting with technological solutions to address those problems,” she said.

That plan has worked phenomenally well so far. As the I.P.O. filing points out, Alibaba already commands a vast portion of the Chinese e-commerce market. Of the 302 million Internet shoppers in China, 231 million already shop at Alibaba’s properties. More than 76 percent of the total value of all mobile commerce in China flows through Alibaba.

What is more, offline retail in China is a far less developed part of the economy than in the United States. This means that unlike American e-commerce companies, Alibaba isn’t fighting against brick-and-mortar stores or even another online retailer. Instead, it is riding a bigger tide. As wealth grows, Alibaba is pushing to make shopping of all kinds a safer and more widely practiced part of Chinese life.

A big example is Alipay, the online payment system that Alibaba introduced in 2004. In the United States, online payment companies like PayPal were meant to replace older, more costly and slower ways of paying, like personal checks or money transfers. But in China, online payments weren’t really a replacement of an old way of doing business. For many people just entering the consumptive middle class, the whole idea of paying large sums in any way, whether offline or online, has always been risky. Fraud and trickery abounded and buyer protections weren’t an ingrained part of consumerism.

Thus, unlike PayPal, Alibaba didn’t just need to come up with a faster or more efficient way of paying. It needed to find a payment method that would allay people’s fears that paying for goods was a bad idea in the first place.

Its innovation was escrow. When a buyer purchases an item from a seller using Alipay, the firm holds the buyer’s money in an account. Only when the buyer informs Alipay that she has received her goods does the payment firm release the money to the seller.

This sounds like a simple, perhaps even obvious, idea. It’s hardly a technological breakthrough. But that’s exactly the point. The Chinese market didn’t need an extremely sophisticated way of paying for goods. It simply needed a way to pay for goods that wasn’t rife with fraud. Alipay satisfied that minimum requirement, adding a badly needed sense of buyer protection over the consumer market. It has become a juggernaut. According to Alibaba, the payment site now commands about half the market for electronic commerce in China.

Many of Alibaba’s other innovations have followed a similar pattern. To Americans, Alibaba’s breakthroughs may look comically backward compared with the technological wizardry being peddled by Amazon, Google, Facebook and Apple. There are no unmanned drones, robotic warehouses, self-driving cars or software-based assistants.

But as admirable as they may be, these American efforts at disruption are also far riskier than Alibaba’s simple plan to ride a cultural wave. Nobody knows if self-driving cars will pan out or if we will ever be O.K. with aerial drones delivering our toothpaste. But the idea of serving a gigantic new consumer market with a set of tools to make shopping easier and safer? That’s not disruptive. It’s obvious. And often, what is obvious wins.