Takeaways from the Berkshire Hathaway AGM 2014 and the Pearl River Delta (PRD) Trip

May 20, 2014 Leave a comment

|

“Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | May 19, 2014 |

| Bamboo Innovator Insight (Issue 34) |

|

Dear Friends and All,

Takeaways from the Berkshire Hathaway AGM 2014 and the Pearl River Delta (PRD) Trip

Q: “How does management factor into valuing intrinsic value?” |

Warren Buffett at the Berkshire Hathaway AGM 2014:“Actually, Ben Graham didn’t get too specific about intrinsic value in terms of calculations. Now it is equated rightly with private business value. Aesop was the first who came up with it. It is intrinsic value if you can foresee the future, the present value of all cash that will be distributed between now and Judgment Day. You put money in and you take money out. One in hand is worth two in bush. The question is: how sure are you that two are in the bush; how far away is the bush; what are the interest rates – Aesop wanted to leave us something to play with over the next two thousand years so he didn’t spell it all out. In calculating it, Ben would say he wanted two dollars of cash in the bush and pay a dollar and emphasized financial factors for those birds in the bush. Fischer would use qualitative and business quality factors to estimate the number of birds in the bush. I started out very much influenced by Graham, so it’s more quantitative, but Charlie came along and said to look more at qualitative factors.”

Come every April-May, the world congregates not only in Omaha to immerse in the wise teachings of Buffett-Munger at the Berkshire Hathaway AGM, but also in Guangzhou, the capital of Guangdong province with its trillion-dollar GDP, for the Canton Fair. Held bi-annually since 1957, the year when Buffett bought his house on Farnam Street after creating Buffett Associates the year before, the Canton Fair is the world’s longest-running trade shows, a monument to China’s industrial versatility and export prowess, connecting foreign buyers with the Chinese factories that have been anonymously manufacturing their products for decades. Occupying 1.1m square metres, the equivalent of 880 Olympic swimming pools, the Fair houses everything from Segway knockoffs to a giant McDonald’s and a mosque for Muslim visitors to bring about the dating of nearly 200,000 buyers from more than 200 countries with roughly 25,000 Chinese manufacturers. The value of total deals in 1957 was $87m and had risen dramatically after Deng launched his economic reforms in 1978/79, peaking at $75bn in 2011. The Fair acts as a barometer for the health of Chinese trade.

While the crowd in Omaha has gotten stronger over the years, those in the Canton Fair have quietened down. In the recently concluded Canton Fair, companies signed $31bn in deals, down by more than half since its 2011 peak and a 13% decline from last spring. The sluggish performance was a result of rising wage pressures that hurt the cost competitiveness of the ubiquitous low-end manufacturers and OEMs, and trade flows moving to Southeast Asia and the ecommerce platform, such as e-Cantonfair.com created by Alibaba, the world’s largest ecommerce company who filed its IPO last week. We believe that the sharp slowdown risk in China is still underestimated by the market. As we have noted in the February and May 2011 monthly editions of On the Ground in Asia, the predecessor of theBamboo Innovator Insight and the Moat Report Asia, we had highlighted how the weak emperors in China and Asia would attempt to consolidate and take back power from the powerful local warlords by flattening the leverage in the system so as to weaken the warlords’ grip in local provinces through controlling the finances. It was an unconventional opinion back then when Asia had rebounded strongly for almost two years from the bottom in March 2009.

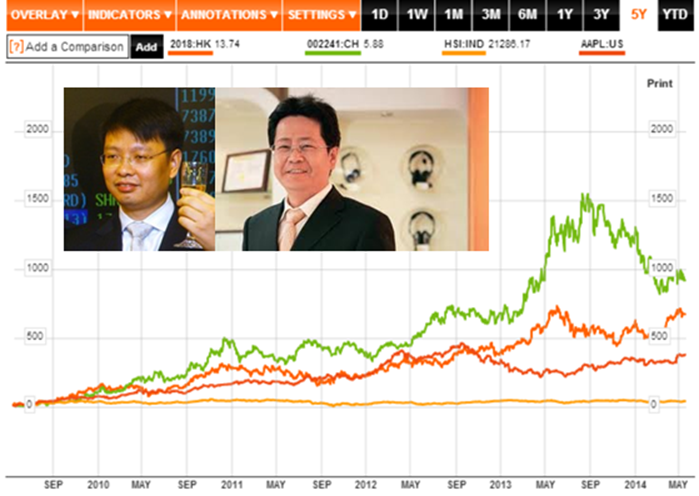

During our trip from 4 to 13 May to the Pearl River Delta (PRD) where we had visited the factories and facilities of diverse industries and interacted with the management and government officials to hopefully bring the financial data alive, we continue to find some possible pockets of competitive “Made in China” strengths. Mobile phones and tablets are increasingly made in China with China’s supply of sophisticated handset components growing to over 60% of total global supply, up from under 10% in 2000. Leading companies include the acoustic suppliers to the iPhone, Samsung, Lenovo such as HK-listed and Shenzhen-headquartered AAC Technologies (2018 HK, MV $6.8bn) and Shenzhen-listed and Shandong-based Goertek (002241 CH, MV $6.7bn). AAC is founded in 1993 and listed on the HK Stock Exchange in Aug 2005. The secretive billionaires Benjamin Pan Zhengmin (below photo on the left) and his wife Ingrid Wu are the co-founders of AAC. Goertek is established in Jun 2001, listed in May 2008 and controlled by Chinese billionaire Jiang Bin (photo on the right). Both AAC and Goertek compete with Knowles Electronics, part of Dover Corp (DOV US, MV $14.4bn) and the world’s largest supplier of micro-electrical-mechanical systems (MEMS) microphones which are widely used in smartphones.

AAC Technologies (2018 HK) and Goertek (002241 CH) Vs Apple and the Hang Seng Index – Stock Price Performance, 2009-2014

Acoustic components account for… <Article snipped>

We also paid a visit to a hidden Chinese export champion based in Zhongshan, Guangzhou with a market value of $460m (PE14e 12.3x, EV/EBIT 11.9x, P/BV 2.1x, P/Sales 0.7x, dividend yield 1.3%). Established in 2002 and listed in…

Amongst the many companies that we saw on the trip include an update on Tencent (2988 HK, MV $128bn), the most valuable Chinese internet giant company.

<Article snipped>

With no time to waste, we pounded the streets of Huaqiangbei – 1.45 square kilometres in the heart of Shenzhen, which, for the past two decades, was the city’s most prosperous area. The latest gadgets – genuine, smuggled or knockoffs – could be found there and shipped all over the world. Since the early 2000s, Huaqiangbei has been the center of China’s shanzhai industry, which churns out electronic goods that imitate well-known brands, mostly mobile phones. Many shops in the biggest electronic components market in China – possibly the world – were now closed, with lease and sale signs hanging on their premises. During its peak in 2009/10, the area had more than 20 malls, many of them boasting a floor space of more than 10,000 square meters, and a district-wide employee count of more than 130,000. At that time, more than one million people visited these shops every day, bringing business worth RMB120bn a year to the business center. Worries about Huaqiangbei’s decline have spread quickly throughout the Delta, especially among the digital product traders and manufacturers who have made the place globally famous.

We had also met with the management and chief economist from the Shenzhen Stock Exchange (SSE) to find out more about the institutional dynamics and governance framework underlying the quoted stocks, including the upcoming cross-border sharing trading plan in…

<Article snipped>

Long-time value investors in Asia are familiar with how management would show the investors-in-suit the “good stuff” while hiding skeletons in the attic. When visiting the Chinese factories, foreign investors are often impressed by being put through the rigmarole of careful hand washing, the donning of sterile scrubs and caps, and so forth, before going on to the bustling factory floor. It is all very impressive, professional looking, and confidence-inducing. Once the funds are transferred and invested (with the transaction executed by the brokers, sell-side analysts and investment bankers who had arranged the trip and later informed the management), these rituals fall by the wayside and are no longer practiced, and the busy activity quiet down. Throughout the visit, it is not uncommon to be showered with the Chinese elaborate art of courtesy or keqi. When cocooned in such hospitality, it would make the issue of raising meaningful and tough questions seem awkward, with the visitors feeling the onus not to spoil things by embarrassing the hosts. Until of course the painful realization that what goes on is façade.

Yet, beneath the façade, institutional and behavioral patterns do not change much. Without intellectual curiosity and a critical mind, visiting companies and meeting with people will be a futile exercise. The enduring art of questioning according to the culture and context will always prove relevant, as Buffett and Munger had shared in their illuminating reply during the Q&A session in the recent Berkshire Hathaway AGM 2014:

Q: “If you are 23 years old and not a software/tech engineer, what would you do with your entrepreneurial instincts – what are would you go into?

Warren Buffett: “I would do what I did at 23 years old and go into the investment business. And I would look at lots of securities and talk to lots of people. I would see CEOs of 8 or 10 coal companies. I often didn’t make appointments, but they almost always would see me. I would ask them, if they had to put all of their money into any coal company except their own, and go away for 10 years, which one would it be? And which would they sell short over 10 years and why? If I did that, I would know more about the coal companies than any manager would.. You need real curiosity about it, it has to turn you on.. If you are open to things and keep learning things, you’ll find something.”

Charlie Munger: “You should do like Larry Bird, who asked a lot of agents who would be their number two choice – and when they all said the same person, Bird hired him and negotiated the best contract of all time.”

Above all, in our decade-plus journey applying value investing principles in Asia, we find that it is critical for diligent value investors to have a balanced perspective, for Truth lie somewhere between glory and disaster. Most importantly, value investors need to have the same heartbeat as the wide-moat compounding Bamboo Innovators: value investors cannot see the elusive Bamboo Innovators as some dragons to slay; we got to look at them with soft eyes until everything – us and them – becomes one.

To read the exclusive article in full to find out more about the wide-moat factors behind AAC and Goertek and the highlights of the various visits at the Pearl River Delta region; please visit:

|

|

| The Moat Report Asia | |

|

“In business, I look for economic castles protected by unbreachable ‘moats’.” – Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia. Together with our European partners BeyondProxy and The Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produce The Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times. Our Members from North America, the Nordic, Europe, the Oceania and Asia include professional value investors with over $20 billion in asset under management in equitiesand savvy private individual investors who are lifelong learners in the art of value investing.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

Our latest monthly issue for the month of May investigates the Home Depot of Asia which has the largest market share in its home country and now seeks to expand regionally. It is one of the few home improvement retailers in the world which is able to achieve a structural negative cash conversion cycle (CCC) at -39 days for resilient, recurring and sustainable operating cashflow to enable the expansion of its store network while keeping a healthy balance sheet. It is hard to achieve negative cash conversion cycle (CCC) as a home retailer as compared to a supermarket retailer as the product nature is more durable. Even Home Depot, Lowe’s and Bed Bath & Beyond (BBBY) are not able to achieve a negative CCC. Led by the capable owner-operators since 1995, the company is a pioneer in proactively creating awareness and demand in the minds of consumers that upgrading your home can be fun and in incremental affordable steps. Its creative branding has resulted in the firm to become the “first on customers’ mind”, or what Charlie Munger elucidated as the “psychological wide-moat” advantage. 80% of sales are generated customers looking for home improvement and renovation ideas and solutions. Growth is supported by the management’s proven ability to identify and cater to dynamic changes in customer preferences. The firm’s comprehensive pre and aftersales service creates brand loyalty and sustains long-term sales. The merchandizing management is tailored to the peculiarities of customer preferences in each area to drive same store sales growth with creative customization by store, location, season and events. Its key strategy to expand its profit margin is to increase its higher-margin house brands and product-mix management. Its EBITDA/sqm of $400/sqm was higher than Home Depot until Home Depot experienced a rebound last year to $500/sqm. The firm’s resilient sales are supported by its unrivalled network of diverse locations throughout the country. Its bold vision and successful “Blue Ocean” execution in the highly fragmented second-tier markets has created a powerful wide-moat advantage that will last for many years to come. In short, the management have proven their ability to execute in difficult market and industry conditions especially in the past 5 to 7 years during the 2007/09 global financial crisis with the firm emerging much stronger. The Illinois Institute of Technology engineering graduate and quiet billionaire owner behind the home retailer is one of the few Asian business tycoons who has the thirst to scale up the business in a sustainable way, as opposed to opportunistic ventures, having been largely influenced by his early years experience observing the success of American wide-moat firms. If we can adjust the EV/EBITDA valuation metric to reflect the CCC, the company’s EV/EBITDA of 18.5x will be lower at 10-11x, while Home Depot’s EV/EBITDA 11x will be higher at 13x. Noteworthy is that Home Depot has a negative free cashflow throughout FY1989-2001 (13 consecutive years!) and yet market cap has climbed from $1.5bn to $103bn. Home Depot compounded despite the ugly valuations during the capex ramp-up. This once again highlights that the power of wide-moat is often underappreciated, misunderstood and overlooked. When Home Depot generated $180m in operating cashflow in FY1992, quite similar to this Asian firm now, Home Depot is valued at $5bn (vs $3bn). Store network is expected to double in the next 4-5 years, representing a potential doubling in market value.

Our past monthly issues examine:

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our subscribers.Questions range from:

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps.

|

|

| Professional Development Workshops for Executives and Lifelong Learners | |

|

Our 7th run of the series of workshop From the Fund Management Jungles: Value Investing Exposed and Explored – (Part 1) Moat Analysis, (Part 2) Tipping Point Analysis and (Part 3) Detecting Accounting Fraud – on 8 Mar 2014 has been well-received with serious value investors, professionals, and serious lifelong learners attending.

Our 8th workshop on Tipping Point Analysis will be held in June 14; we are taking a short break as our business partner Linda is delivering her new baby!

Thank you for your support all this while!

|

|

|

Thank you so much for reading as always.

Warm regards, KB Kee Managing Editor The Moat Report Asia |