IEX, Dark-Pool Operator Featured in ‘Flash Boys’ Book on High-Speed Trading, Seeks Funds to Become an Exchange

May 27, 2014 Leave a comment

IEX, a Maverick Trade Venue, Is in Cash Talks

Dark-Pool Operator Featured in ‘Flash Boys’ Book on High-Speed Trading Seeks Funds to Become an Exchange

SCOTT PATTERSON, BRADLEY HOPE and TELIS DEMOS

Updated May 23, 2014 10:53 p.m. ET

IEX Group Inc., an upstart trading venue that aspires to be a haven from high-frequency trading, wants to become the only stock exchange that isn’t dominated by speedy dealers.

The firm is in talks with potential investors to raise millions of dollars to expand its operations and pay for the increased regulatory costs of becoming a full-fledged exchange, according to people familiar with the talks. At present, IEX is a “dark pool,” a lightly regulated, private trading venue.

IEX could fetch a valuation of $200 million to $300 million, although the numbers could change because the discussions are continuing, the people say. That valuation is high for a company that has only been fully operational since October and controls just a tiny percentage of stock trading the U.S.

The firm’s ambitions reflect the swift and seismic shift in stock-market trading over the past few years. But the leap for IEX, which employs 35 people, to become an exchange would be a big one that would also bring questions about its business to the fore.

IEX today operates a dark pool, where buy and sell orders are matched but information is published only after trades are executed. The lack of trade information is designed to help investors place orders without alerting other traders about their intentions. Stock exchanges are more transparent, publishing reams of information about traders’ orders. But they have become dependent on high-frequency traders, which account for about half their volume.

IEX has become well-known since the publication earlier this year of Michael Lewis’s best-selling book “Flash Boys,” which features its chief executive, Brad Katsuyama, as the protagonist. The book also ratcheted up the debate over high-speed trading.

Defenders of such activity, in which fleet-footed traders move into and out of markets in fractions of a second, say it helps make trading cheaper, because the firms can consistently post orders, giving investors who want to buy or sell a party to trade with.

Critics say the hair-trigger traders have advantages other investors don’t, such as the ability to react to market shifts in fractions of a second.

IEX has capitalized on those fears by claiming to have leveled the playing field. Although IEX allows high-frequency firms to trade on its platform, it houses clients’ computers in a building that is separate from its computer system and has introduced a delay—or “speed bump”—of 350 millionths of a second between the time a client sends an order and when it reaches IEX’s computers.

Stock exchanges, on the other hand, place client computers in the same building as their own, cutting delays to less than 10 millionths of a second at times. That lets high-speed traders react to market shifts faster than firms that don’t house their computers in the same building.

There are currently about a dozen U.S. stock exchanges, which are mostly operated by the NYSE Group, part of IntercontinentalExchange Group Inc.; Nasdaq OMX Group Inc.; and BATS Global Markets Inc. The exchanges declined to comment.

IEX has previously gained the backing of a number of big investment firms, such as Los Angeles-based Capital Group Cos., which manages American Funds, and has shunned investments from Wall Street banks.

The latest fundraising talks, held at IEX’s New York headquarters, have involved hedge funds, private-equity groups and asset managers, according to people familiar with the talks.

The question for IEX, experts say, is whether it can compete with other exchanges without catering to high-frequency firms. IEX is gambling that it can attract business from big asset managers who in recent years have grown wary of high-speed firms. Their chief concern is that the faster firms can detect their orders using powerful computer systems and trade ahead of them, making it harder and more costly to trade.

An exchange owned solely by investment firms would be a “game changer,” said Albert Kyle, a professor of finance at the University of Maryland who has advised the government on market issues. “The motives of the exchange would be different than what we have now, and that could have benefits for investors,” he said.

Becoming an exchange also would be more costly for IEX, since exchanges are subject to more regulatory scrutiny than dark pools, subjecting them to extensive legal expenses, among other costs.

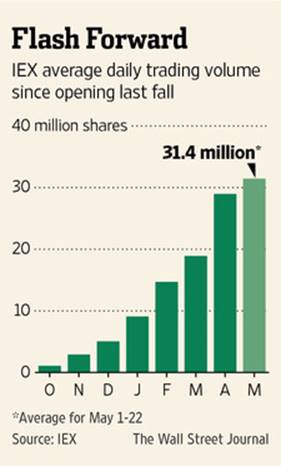

IEX’s trading activity has grown rapidly. Its daily volume averaged 29 million shares in April, up 53% from March and one of the fastest starts by a dark pool on record, according to Rosenblatt Securities Inc. Still, IEX processes only a tiny fraction of overall trading, about 0.5% of the market’s daily volume.

Some market participants have taken issue with IEX’s business. Critics such as Chicago hedge-fund giant Citadel LLC say IEX’s market is skewed in favor of brokers to the detriment of certain traders, such as individual or “retail” investors who buy and sell stocks through personal accounts. IEX lets orders from brokers jump ahead of private firms or investors trading from a personal account, if the broker can execute both sides of the trade, a method designed to encourage brokers to send orders to IEX.

That gives a leg up to big brokers, such as big Wall Street banks, at the expense of small traders, critics say. “Giving brokers a pass to the front of the line does not serve retail investors, period,” said Jamil Nazarali, head of Citadel’s market-making platform. IEX says such broker-to-broker trading represent about 3% of its volume.

Some brokers who run their own dark pools have tried to dissuade clients from routing orders to IEX, traders say. Citadel, which operates its own dark pool and engages in high-speed trading, has told some trading partners that IEX is unfair to small investors, according to people familiar with the conversations.

Law-enforcement officials and regulators have also ratcheted up scrutiny of high-speed-trading amid fears the firms are able to act on market-moving data before other investors.

The concerns spilled over into a congressional hearing in April. Rep. Scott Garrett (R., N.J.), who has probed stock-market issues in a series of hearings and public discussions, asked Securities and Exchange Commission Chairman Mary Jo White, “Are the markets rigged?”

Ms. White noted that the marketplace has “changed dramatically” in recent years and that it “continuously evolves.”

“The markets are not rigged,” she said. “The U.S. markets are the strongest and most reliable in the world.”