Malaysian property buyers may be affected by rate hike

May 27, 2014 Leave a comment

Updated: Saturday May 24, 2014 MYT 11:30:21 AM

Property buyers may be affected by rate hike

LIM Lian Hong, executive director of Raine & Horne International, defines “living dangerously” as when one overcommits and finds oneself in the red once too often. It also means not being able to meet a financial emergency.

Being a property professional, he explains “living dangerously” against a property sector backdrop. He says there is the tendency to commit oneself to a property, or a few properties, when prices are on an uptrend.

Since early 2009 and until last year, the interest in property investment has been tremendous. Young people aged 25 onwards had piled onto the property market.

Lim says there are two fundamentals about a property purchase. It provides the owner with a rental income. It offers capital appreciation. There two factors interplay against each other, says Lim.

In Malaysia, the pursuit for capital appreciation far outweighs that of rental return.

Over the past several years, Lim has overheard the comment time and again that property prices will “surely go up”. So everybody jumps on the bandwagon.

“Because of the high prices today, the rental income may not be that attractive. But they say, ‘never mind.’ This means capital appreciation is a more powerful incentive,” says Lim.

Property prices in the Kuala Lumpur City Centre (KLCC) was about RM1,000 per sq ft about 10 years ago. The question to him was: “Is it worth buying?”

His answer: “How much return do you want?”

If the unit is 2,000 sq ft, the price of the property will be RM2mil. In order to get 5% gross, you need to get a rental of slightly more than RM8,300 a month for the investment to be viable. At that time, KLCC did not offer that kind of yield.

If they were able to get 50% or more of what they had put in – their equity, so to speak – at the end of the investment, they do not mind the small return because the amount they expect at the end of the investment is expected to outweigh their “initial losses”.

The scenario today is different. Prices have spiked a lot.

“If it is to have a roof over one’s head, one will have to buy if one can afford it.

“But if one were to buy with the hope of further capital appreciation, one may think twice.

“If the property is RM500,000 and a RM200,000 down payment is made and RM300,000 is in the form of a loan, your commitment or responsibility is RM500,000, not RM300,000 because the total price of the unit is RM500,000, and also because the life span of the loan is X number of years,” says Lim.

Of late, there has been renderings that Bank Negara may increase the overnight policy rate (OPR) by 25 basis points (bp) in July. If this becomes a reality, the base lending rate (BLR) on which mortgage rates are based will go up.

VPC Realtors (KL) Sdn Bhd director James Wong is of the view that important though the interest rate and returns may be, it is demand and supply that determine prices.

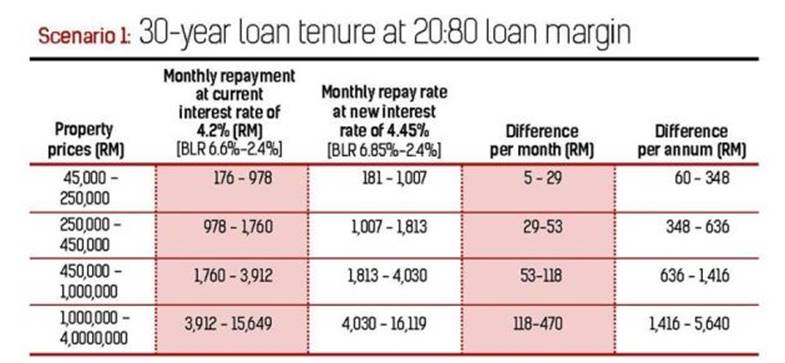

Wong says an increase of 0.25% in the BLR will not have a significant impact on borrowers for low cost and affordable housing priced between RM45,000 and RM450,000.

There will only be a marginal increase of RM5 to RM53 per month for loan repayment compared to the current interest rate for a 30-year loan tenure with a 20:80 loan margin, he says.

“As for high-end residential properties, most buyers are financially secure. They are either a cash buyer or they buy with minimum loan margin. Hence, an increase of 0.25% per annum will be insignificant,” says Wong.

As for the speculators, Wong says some would have unloaded their purchases after the introduction of anti-speculative measures in the last Budget 2014.

“Those who bought properties to flip, if they are unable to service the loan, they will be forced to sell. But it will not be as easy as before due to the real property gains tax,” says Wong.

While the anticipated increase in BLR may result in buyers taking a wait-and-see stand, it is the loan tenure and the subsequent rise in monthly repayments that will impact borrowers significantly, although thus far, the loan tenure is expected to be unchanged.

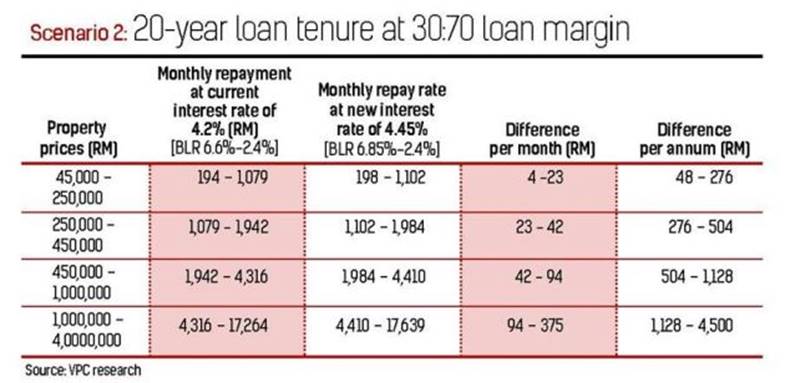

If the property is priced at RM400,000, the buyer will have to fork out at least RM120,000 as down payment at a 30:70 loan margin, excluding legal fees and stamp duty compared with a RM80,000 down payment if it were a 20:80 loan margin.

“Young professionals between 25 and 35 years may not be able to afford to buy a house even at RM400,000 if Bank Negara restricts the borrowing guidelines by reducing the loan margin,” says Wong.

The current monthly repayment for a RM450,000 property with loan margin of 20:80 is RM1,760 for 30 years (loan amount: RM360,000). If the loan tenure is reduced to 20 years, the new monthly repayment will be RM2,220.

Says Wong: “This is an increase of 26% of the lending cost”.

On the effect of the anticipated increase in interest rates on rent, Wong says there is no effect at all. Housing rental, he says, is mainly determined by supply and demand.