China’s Game of Real-Estate Chicken: Who Will Blink First: Buyers, Developers or the Government?

May 31, 2014 Leave a comment

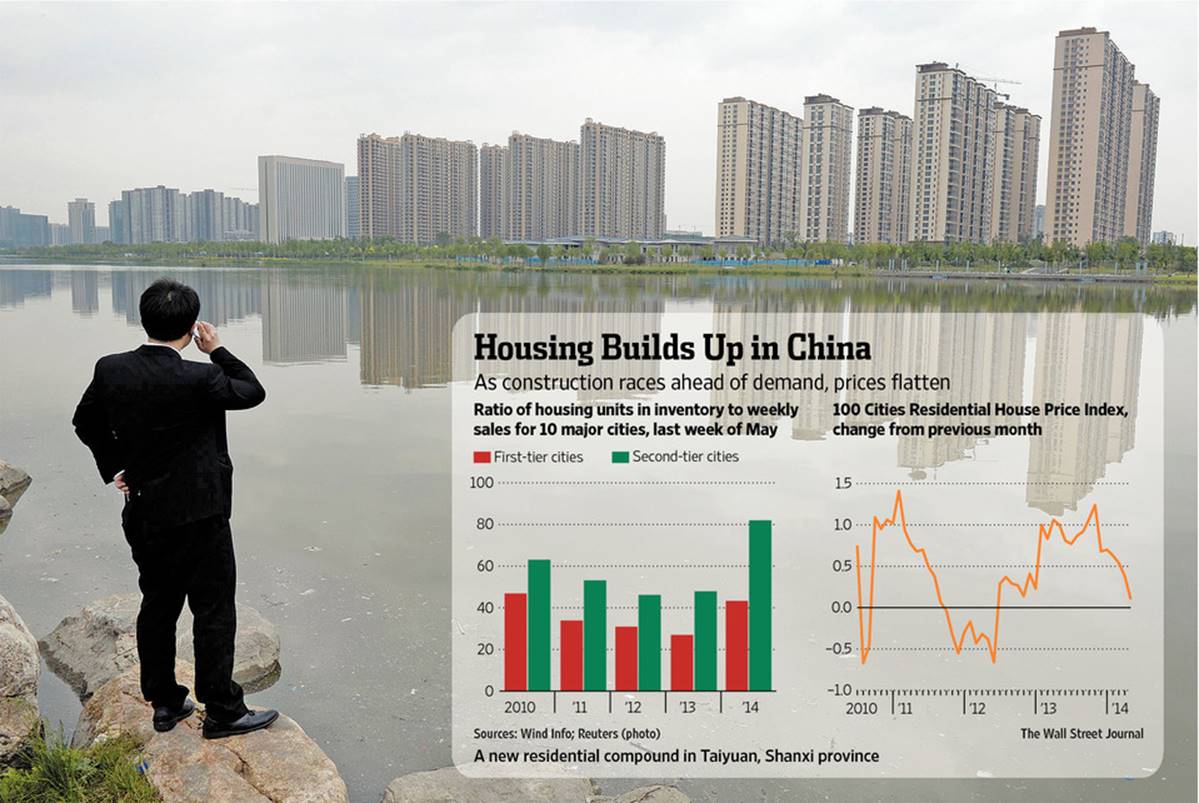

China’s Game of Real-Estate Chicken

Who Will Blink First: Buyers, Developers or the Government?

WEI GU

May 29, 2014 3:38 p.m. ET

The main question in China’s housing downturn: Who will blink first?

Whether buyers, developers or the government, it will say a lot about how China manages what is looking like a serious bust.

“Now there is a stalemate,” said David Hong, head of research at data provider China Real Estate Information Corp. “Developers are betting the market will bottom soon, once the government succumbs to growth pressure.”

Buyers seem least likely to give in. Property sales by value fell 10% in the first four months of the year as people took a wait-and-see approach, holding back for bargains.

Developers have been hanging tough, too, holding on to their bulging inventories rather than cut prices. But while many can survive a brief slowdown, they are counting on the government to goose demand by loosening liquidity.

That leaves policy makers. They look more determined than in the past not to step in. But real estate, including transactions and construction, accounted for 12.7% of gross domestic product last year, according to J.P. Morgan JPM +0.49%Chase, and for 15.1% of GDP growth. Any slowdown would put the government under great pressure for measures to keep the economy performing.

Ironically, the factors behind the slowdown include one major government initiative: the anticorruption drive. “Government officials and related people used to account for 30% of the buyers,” according to Shih Wing-ching, founder of Centaline Group, a large property agency in Hong Kong and mainland China. “They don’t dare to buy properties now for fear of attracting attention.”

Another significant force is the disappearance of investors who trade for short-term gains, Mr. Shih added. They have moved on as the market slows.

And then there is the development of new options for investors outside of domestic real estate—including foreign real estate. Rich Chinese who already own multiple homes in China are now parking their money overseas, buying in new developments built by Chinese property companies in locations like London, California and Australia. Chinese outbound investment into residential development during the first quarter was up 80% from a year earlier, according to real-estate firm JLL.

With prices flat, the number to watch is inventories. Aggressive land buying in the boom years of 2012 and 2013 means more supply in 2014. Inventories in the first-tier and second-tier cities were equal to 14 months of sales volume at the end of April, approaching the high of 16 months hit in February 2012, according toMoody’s. MCO -1.01% This will lead to pressure on developers’ working capital.

The inventory problem is worse in smaller cities. “Shrinking volumes will be followed by price cuts,” Mr. Shih said. “There is so much oversupply in second- and third-tier cities.”

Some highly leveraged developers can’t afford to just sit on their inventory for much longer. Large developers have been able to roll over their debt, but even they have found it difficult to raise new funds, whether at home or abroad. Small developers are borrowing at exorbitant rates, banks having turned their backs on them.

Developers with large inventories, weak sales and limited access to funding are especially vulnerable to a market downturn and at risk of refinancing difficulties. A number of Chinese developers now don’t have enough cash to cover their short-term debt, according to Moody’s.

“Usually developers get a cash-flow problem about six months to a year after the downturn starts,” said Jerry Wang, CEO of overseas-focused property fund Chengming Capital Management Co. and former chief financial officer of developer Forte Group. “Starting in September, I expect to see widespread selloff.”

The big unknown is whether such a selloff would cause the government to change its stance. Real estate isn’t just a major driver of economic growth, but also the top source of revenue for local governments; land sales cover 60% of their budgets. Slow home sales mean developers won’t have much money to buy more land from local governments, which will leave those governments unable to increase public investment in hopes of boosting the economy. J.P. Morgan expects land-sale revenue to drop 5% to 20% this year.

Beijing is trying to wean local governments off their dependence on land revenues, but the shortfall will be hard to make up quickly. After inventory hit that 2012 high, the government stepped in by cutting interest rates and speeding up money supply.

“In the past 10 years, every time it was the government who gave in,” said the chief executive of a state-owned property developer. “The more they do this, the more an eventual crash looks inevitable.”