Finance: In search of a better bailout

By Robin Wigglesworth

Proposals to overhaul sovereign debt restructuring are raising fears of unintended consequences

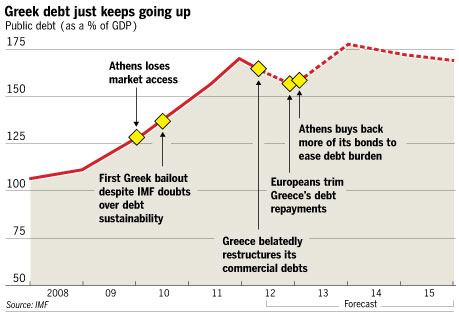

For two years Petros Christodoulou had one of the world’s toughest jobs. As head of Greece’s debt office his first task was convincing increasingly sceptical investors to lend to Athens. Then he had to orchestrate the biggest government debt restructuring in history amid a cacophony of protest from bankers, politicians, hedge funds and European leaders.

Mr Christodoulou, who had spent years as a trader at JPMorgan and Goldman Sachs, held his nerve but the pressure was too much for some of his staff, who quit. Once the restructuring was complete, he too left Greece’s debt management office. “It was a tremendously strenuous situation,” he admits. “When Armageddon hits you’re always less prepared than you think.”

Still, Mr Christodoulou feels there are valuable lessons to be learnt from Greece’s bruising experience with sovereign debt restructuring. “The system needs to be fixed,” he says. “We should have a predictable framework for restructurings that ensures that other countries do not have to go through what Greece did.”

He is not alone in thinking that the bankruptcy process for countries should be overhauled. The eurozone crisis has triggered a boisterous discussion among policy makers, investors, economists and academics about the merits and pitfalls of the framework for sovereign restructurings, or rather, the lack of one.

Even the Canadian and UK central banks have weighed in with opinions on how to improve the system.

The debate has grown more heated since Elliott Management, a US hedge fund known for extracting money from defaulting countries, scored a legal victory in 2012 over Argentina in a protracted courtroom battle. Although Elliott has yet to extract a peso from Buenos Aires, many experts fear that its initial success has handed a potent weapon to creditors that will further complicate future sovereign restructurings.

This is not merely an arcane discussion over what went wrong with Greece but a politically fraught debate that could still have a seismic impact on the global financial system. The eurozone crisis has abated but many fear that the fundamental problem it highlighted – high levels of government debt across much of the world – remains a danger.

Philip Wood of Allen & Overy, the law firm that advised Greece’s creditors, says: “I hope Greece was a one-off but I am not sure it was. If you look at all the debt out there it is hard to conclude that there isn’t a problem. State bankruptcies have not gone away. In fact they are likely to get worse.”

Last year, the fund decided to throw its weight behind those who felt the current system was riddled with problems. In a far-ranging paper released in April, it floated a series of proposals that thrilled many proponents of an overhaul and horrified opponents.

The IMF’s primary argument was that countries tend to restructure too late, and when they do the debt relief they obtain is too modest. That means that any bailout loans provided by the fund, or other official sector lenders such as development banks or neighbouring countries, in effect go to pay off private creditors and merely add to a daunting debt burden.

The IMF therefore plans to explore ways to get creditors to “voluntarily” reschedule a distressed country’s debt repayments when it cannot say for certain whether the government is facing a temporary downturn or a full-blown solvency crisis. Only after that stage would the fund step in with a rescue programme.

The IMF is also seeking ways to address the threat posed by the Argentine litigation. Stripping away the euphemisms it means the fund would require countries to default on their debts and creditors to swallow a loss – albeit mild – if a country is forced into its arms. Yet Hugh Bredenkamp, deputy director of the IMF’s policy department, argues this is necessary to avoid a repeat of cases such as the Greek crisis.

“Recent experience shows that debt restructurings have often been too little, too late, thereby impeding economic recovery, deterring investment and creating opportunities for private creditors to cash out in a run up to the restructuring, leaving the official creditors – that is the taxpayers – to bear the burden,” he says.

I hope Greece was a one-off but I am not sure it was. If you look at all the debt out there it is hard to conclude that there isn’t a problem

– Philip Wood of law firm Allen & Overy

The IMF is now engaged in a protracted consultation with economists, academics, investors, bankers and officials over its proposals. It hopes to present refined proposals to the fund board for approval in June.

Even after that the IMF expects more discussions will be necessary. “We are proceeding carefully, and without any urgent deadlines or imminent needs in mind,” Mr Bredenkamp stresses.

Some experts think the IMF is not going far enough. They want a comprehensive framework for state bankruptcies akin to a proposal it floated a decade ago. The initiative, known as the Sovereign Debt Restructuring Mechanism, mimics aspects of corporate bankruptcies, with the fund playing the pivotal role as judge. But the initiative foundered after the US withdrew its support.

The IMF is at pains to stress that it is not seeking a “statutory” solution to the problems it identified. It is primarily exploring changes to its lending policies and modest improvements in the restructuring process through bond contract tweaks.

These could include beefing up “collective action clauses”. They rose from the ashes of the mechanism and allow a supermajority of bondholders to vote on a restructuring that binds everyone. They are now common in bond markets, and limit the chances that minority creditors such as hedge funds such as Elliott can undermine a deal. But they are far from universal, or a panacea, which is why the fund wants to sharpen them.

“The fund is looking for something that will make the system work a little bit better,” says Anne Krueger, who was the leading champion of the SDRM as first deputy managing director of the IMF in 2001-06. “Obviously it would help to have a statutory mechanism in place but the question is whether it is feasible within the political constraints.”

. . .

Yet the Committee on International Economic Policy and Reform, an influential think-tank, has backed the IMF and urged it to go even further in some areas. In a paper called “Revisiting Sovereign Bankruptcy” published in October, the think-tank advocated a statutory system for the eurozone, sweeping bond contract reform and the creation of a “sovereign debt adjustment facility” under the aegis of the IMF. This would combine fund lending with debt restructuring under clearly defined ex ante criteria.

Lee Buchheit, a partner at Cleary Gottlieb, legal counsel of choice for distressed countries and co-author of the CIEPR paper, concedes that resistance to the proposals is fierce. Yet he is confident that the debate will bear fruit. “It’s just so hard to come up with good policy arguments against it,” he says.

Nonetheless, there are plenty of officials, lawyers, academics and investors who have lined up to criticise even the IMF’s more modest proposals. They warn that if implemented, the plan would have severe unintended consequences that could in extremis have systemic implications.

Mr Wood argues that despite concerns over the impact of the Argentine litigation, the current system “seems to work quite well”. He points out even Greece’s mammoth, politically fraught restructuring only took months. “There is a legal vacuum in sovereign restructuring but that doesn’t mean there is anarchy.”

While the fund reckons restructurings are often late and inadequate, investors worry that it will now veer too forcefully in the opposite direction, with action triggered by facile debt thresholds, for example. IMF officials stress it is seeking only judicious, gentle “rescheduling” when it cannot say for certain that the debts are sustainable, but many money managers are sceptical.

Some fund managers predict that this would raise the borrowing costs of countries and make crises more frequent and more painful. As soon as investors get a whiff of a possible IMF programme the country involved would be frozen out of debt markets. Money could even start gushing out of the domestic banking sector, swiftly escalating mild concerns into a full-blown financial crisis.

It is not only self-interested investors who are worried. Moody’s, the rating agency, has warned that the proposed IMF “policies may improve the resolution of sovereign debt crises but they will probably increase the likelihood, move forward the timing and increase the severity of debt restructurings”.

. . .

Some experts argue that the fund needs to stiffen its political backbone, not its policies. After all, the IMF initially endorsed the restructuring-free bailout of Greece following intense pressure from its European shareholders. If the fund is sceptical that a country’s debts are sustainable, it can in theory use its position as a lender of last resort to force a country to restructure its debts.

“There’s nothing missing in the IMF toolkit except political will,” says Anna Gelpern, a law professor at Georgetown and co-author of the CIEPR paper.

Most crucially, some of the IMF’s own shareholders seem to be harbouring doubts. The US Treasury is concerned by the emboldening impact that Elliott’s victories over Argentina could have on other hedge funds. But the Treasury favours a pragmatic, case-by-case approach rather than adopting what it feels will be a policy of presumptive restructurings. Even European governments that supported the SDRM initiative are concerned that the proposals could scare investors away and reignite the eurozone crisis.

Despite the opposition, some of the IMF’s proposals are likely to survive. For example, less contentious measures, such as beefing up Collective Action Clauses to allow restructuring votes across a country’s debts rather than just bond-by-bond, could be implemented. These will, in time, ameliorate the danger of Argentine-style litigation.

The very fact that the IMF is re-examining its lending policies could also have an impact. It is clearly trying to signal that creditors should not expect to emerge from all future IMF programmes unscathed.

Irrespective of what the fund board and government shareholders eventually decide, Mr Buchheit argues its staff will get one thing they want: “A message to markets that the assumptions of full bailouts in all cases are unfounded, and to troubled debtors of the future that they should expect to have to restructure.”

Even some old foes of IMF over-reach support that view. John Taylor, an economics professor at Stanford, was a leading opponent of the SDRM as US Treasury undersecretary for international affairs in 2001-05, but agrees the sovereign restructuring process now needs fixing.

He still favours a contractual approach but argues the fund should have a restructuring policy as automatic, clear and credible as possible. “We have to get away from this bailout mentality,” he adds.

——————————————-

An alternative fix for the faultlines

The International Monetary Fund is not the only powerful institution to support a reworking of the sovereign debt restructuring process.

In November the UK and Canadian central banks jointly presented their own solution to the “faultlines” in the present regime revealed by the eurozone crisis.

The jointly authored paper proposed that governments start issuing “contingent convertible” bonds, and bonds where the returns are linked to economic growth. So-called “sovereign cocos” would automatically extend repayment times when countries receive a bailout. Growth-linked bonds would pay out according to a country’s economic output, rather than a fixed amount, irrespective of the conditions of state finances.

These would help resolve future debt crises and reduce moral hazard and the demands on the public purse, the central banks argued.

There have been several similar proposals in the past but Mitu Gulati, a law professor at Duke University, points out that the two central banks enjoy some clout in policy making circles. “The Bank of England does not have a habit of wasting its time, and they’re really pushing this idea with the Bank of Canada,” he says.

The paper recognised that there could be resistance to its ideas and notes the dearth of sovereign cocos and gross domestic product-linked debt, despite the apparent economic logic. But the authors highlight how international backing ensured that “collective action clauses” – which allow a majority of creditors to vote on a restructuring that binds all – have become ubiquitous.

This experience suggests that it would be possible to implement the two types of state-contingent bonds proposed, the paper argues.

Crucially, the central banks’ proposals would be a “contractual” approach to tweaking the sovereign debt restructuring process, which the IMF now says it favours, as opposed to a more heavy-handed “statutory” fix.

However, that means that even if the ideas are championed by policy makers and countries begin issuing bonds with these provisions, it will take many years before most government bonds in circulation include the clauses.

{kind=link}