With Top 4 US Banks Holding $217 Trillion In Derivatives, Total Number Of US Banks Drops To Record Low

December 4, 2013 Leave a comment

With Top 4 US Banks Holding $217 Trillion In Derivatives, Total Number Of US Banks Drops To Record Low

Tyler Durden on 12/03/2013 09:49 -0500

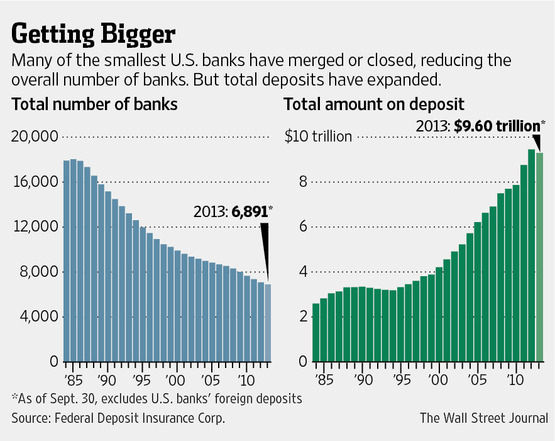

Overnight, the WSJ reported a financial factoid well-known to regular readers: namely that as a result of a broken system that ever since the LTCM bailout has encouraged banks to become take on so much risk they become systematically important (as in their failure would “end capitalism as we know it”), and thus Too Big To Fail, there has been an unprecedented roll-up of existing financial institutions especially among the top, while the smaller, less “relevant”, if far more prudent banks have been forced out of business. “The decline in bank numbers, from a peak of more than 18,000, has come almost entirely in the form of exits by banks with less than $100 million in assets, with the bulk occurring between 1984 and 2011. More than 10,000 banks left the industry during that period as a result of mergers, consolidations or failures, FDIC data show. About 17% of the banks collapsed.”The resulting elimination of over 10,000 banks in the past thee decades is shown in the WSJ chart below, which also shows total amounts of bank deposits.

The WSJ comments as follows:

The consolidation could help alleviate concerns that the abundance of U.S. banks leads to difficulties in oversight or a less-efficient financial system. Meanwhile, overall bank deposits and assets have grown, despite the drop in institutions.

Well, first of all, as David Kemper, chief executive of Commerce Bancshares Inc., a regional bank based in Missouri, said “Seven thousand is still an awful lot of banks,” particularly in an era where brick-and-mortar branches are becoming less profitable, said “There’s no reason why we need that many banks, especially if those smaller banks have a much lower return on capital. The small banks’ bread and butter is just not there anymore.”

But more important is the erroneous observation about deposits, which indicates a persistent lack of understanding about how QE works. As we won’t tire of explaining, the ~$2.2 trillion surge in deposits since Lehman is matched only by the ~$2.2 trillion surge in Fed created reserves. In other words, excess reserves appear on bank balance sheet as excess deposits, which are then used by banks to gamble away a la the London Whale, which used nearly half a trillion in fungible reserves (as manifested the liability side of its ledger) to fail in cornering the IG9 market. This transformation is shown on the chart below (discussed in depth here).

The point here is that the number of banks is largely irrelevant: it is obvious that the big will keep on getting bigger, and the Big 5 banks will do all in their power to either acquire their profitable competition or put everyone else out of business. However, the far bigger question is what happens to bank deposits once the Fed start to taper, ends QE or outright unwinds its balance sheet, which ultimately would soak up trillions from bank deposits. Because if there is one thing that is clear is that without the Fed, and without commercial bank loan creation (which has been non-existent in the past 5 years), bank balance sheet would be exactly where they were the day Lehman died.

Finally, one does not need to go any further than the following chart from the OCC showing total bank derivative holdings for all US banks and just the Top 4. The punchline: just the 4 biggest US banks hold $217.5 trillion, or 93% of the total $233.9 trillion in derivatives.

In light of the above, who cares how many other banks in the US exist?