An Expensive Play on China’s Bad Debts; Investors Shouldn’t Volunteer as Guinea Pigs in Beijing’s Cinda Experiment

December 5, 2013 Leave a comment

An Expensive Play on China’s Bad Debts

Investors Shouldn’t Volunteer as Guinea Pigs in Beijing’s Cinda Experiment

AARON BACK

Updated Dec. 3, 2013 2:21 a.m. ET

China Cinda Asset Management has essentially become a state-owned hedge fund that specializes in distressed assets. Now foreign investors are invited to bet on its success in a Hong Kong public offering. They should pass. Beijing created Cinda in 1999 to take nonperforming loans off the books of state-ownedChina Construction Bank.601939.SH -0.22% It never made money on this batch of loans, which it was forced to buy at face value and eventually had to fob off on the government. It later was able to buy more loans at deep discounts, and since 2010, take over debts that Chinese companies owe each other. These business lines have been profitable, according to pre-IPO documents.Now the asset manager, which is due to start trading on Dec. 12, is being pitched to the public as a countercyclical play: When China’s economy is slowing, there are more nonperforming loans for it to take up. But that’s only half the story. While tough economic conditions increase the supply of distressed assets, they also make it harder to turn them around.

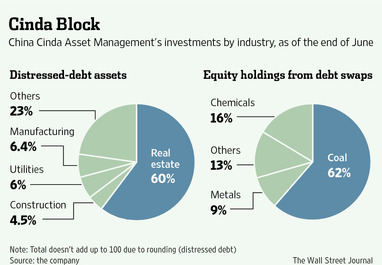

This is where Cinda faces substantial risks. At the end of June, a whopping 60% of its distressed debt assets were in real estate, already a tangled web of perils in China’s economy. As for its equity holdings from debt swaps, 62% are in the coal sector, which is plagued by overcapacity and state support. There is little prospect for IPOs or other ways to monetize Cinda’s coal investments.

To ride out the downturn that Cinda seems so eager to embrace, it would help to have long-term funding in place. Unfortunately, three-fourths of Cinda’s bank borrowing has a duration of less than two years. Funding mismatches could give rise to a liquidity shortage.

The hope is that Cinda’s status as a state-owned entity will help it secure loan rollovers from creditors even in tough times. Institutions such as UBS UBSN.VX -2.67% and Standard Chartered that have already taken stakes in Cinda could be comforted by Cinda’s majority owner, the Ministry of Finance, which has already shown considerable forbearance. In 2010, it took over responsibility for most of Cinda’s legacy debts and later let it delay payments to the Ministry itself for a tranche of heavily discounted loans.

Ordinary investors shouldn’t be so sanguine. Even if Cinda is too connected to fail, there is no guarantee its stock price will hold up. China’s big four banks enjoy state backing, but their shares have been poor performers over long stretches. All four are down over the past three years.

The IPO doesn’t look to be a bargain either. At the indicative price range, Cinda would be worth 1.1 to 1.3 times 2013 book value. China’s big four state-owned banks trade at an average of around 1.1 times book value, and their average return on equity over the past three years, from plain vanilla lending, is 20.9%, compared with 19.8% for Cinda.

The project of converting a “bad bank” bailout vehicle into a viable commercial enterprise is a novel experiment by Beijing. Investors shouldn’t volunteer as guinea pigs.