Loan Sharks Smell Blood in China Waters; Credit China Is Part of a New Breed of Shadow Lenders

December 30, 2013 Leave a comment

Loan Sharks Smell Blood in China Waters

Credit China Is Part of a New Breed of Shadow Lenders

JASON CHOW

Dec. 29, 2013 8:39 p.m. ET

Sitting in an empty Papa John’s PZZA -1.07% pizza restaurant, real-estate developer Yang Boqun said he would somehow catch up on loan payments for 150 million yuan ($24.7 million) he borrowed to finish a five-story shopping mall in the eastern Chinese city of Jinhua.But the mall’s only tenants are a Bentley car dealership, movie theater and the restaurant—and the loan’s interest rate is a steep 40%. The reason: When construction costs on the two billion-yuan project soared surprisingly high, traditional banks couldn’t lend more to Mr. Yang.

So he turned to Credit China Holdings Ltd. 8207.HK +3.17% , one of the thousands of so-called shadow lenders in China. Mr. Yang got the money—and now Credit China wants it back.

“I am a loan shark but a legal one,” said Raymond Ting, chairman and executive director of Credit China, in an interview about 750 miles away at a wine store he owns in Hong Kong. He made a fist and said he is “squeezing” Mr. Yang by threatening to seize a piece of the shopping mall.

The real-estate developer has repaid five million yuan and promised to hand over another 25 million soon.

Mr. Ting is an unusually aggressive example of the shadow bankers who have stepped in to lend to debt-hungry businesses and household as the Chinese government tries to rein in traditional banks. Many analysts and investors are worried that the country’s slowing economy could ignite a debt crisis, but shadow lending keeps growing.

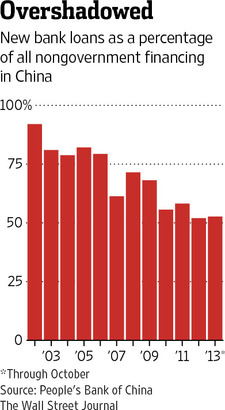

In the past five years, borrowing by businesses and households as a percentage of gross domestic product rose nearly 60% in China, according to Goldman Sachs Group Inc. From 2010 to 2012, shadow lending doubled to 36 trillion yuan, according to analysts at J.P. Morgan Chase & Co. Bank loans totaled just 53% of all lending in China in the first 10 months of 2013, down from 72% in 2010 and 92% in 2002, according to figures from the People’s Bank of China, the country’s central bank.

The shadow-banking industry includes trust companies, pawn shops, informal lenders, microfinance and a handful of publicly traded companies like Credit China that tap the capital markets to keep loans flowing. Such firms often use lending practices that aren’t permitted at traditional banks. Some economists say the sector’s rise has worsened China’s credit binge by increasing the number of risky loans and inflating real-estate prices.

Mr. Ting, 41 years old, says down-on-their-luck property developers like Mr. Yang who have been cut off by banks and need a bit more money to finish a project are typical customers of Credit China. As of June 30, the company had about 816.7 million yuan in loans on its books, up from 303.8 million yuan in 2010.

Mr. Ting charges the highest interest rate allowed by Chinese regulators—four times the prime lending rate, now 6%—and adds consulting fees that can boost the total borrowing cost to 50% per year.

“We don’t loan to friends,” the banker said while sitting in his wine store. Wearing loafers and no socks, Mr. Ting whirled a glass of 1985 Château Mouton Rothschild from his collection of more than 50,000 bottles.

“We have to assume that it’s always going to be bad debt,” he added. “At 3.3% a month, how can they be good people?”

Mr. Ting says he is trying to meet demand from borrowers who can’t get money in China’s traditional banking industry, where giant, state-owned banks make most of their loans to giant, state-owned companies.

“Getting a loan at a bank takes months, taking people out for dinner and karaoke, waiting for approvals, and still it’s no guarantee,” he says. Credit China’s turnaround time on loans is about two weeks. Its license as a pawnshop operator allows the company to accept real estate as collateral.

A son of a former Shanghai property developer, Mr. Ting studied economics at Beloit College in Wisconsin but left after two years. He previously ran a Chinese mobile-communications firm and joined Credit China after his family got a controlling stake in the lender. He runs Credit China from Hong Kong.

The company funds loans from proceeds of its initial public offering in 2010, three bond sales in the past two years and a one billion yuan ($164.8 million) investment from state-owned company Shanghai Xinhua Publishing Group Ltd. Xinhua couldn’t be reached for comment.

Mr. Ting isn’t shy about his loan-collection tactics. In 2010, Shanghai property-development company Yuhu Investment built a 26-building office complex on industrial land in the Shanghai suburb of Qingpu. The project has sat empty since 2011 and now the developer is trying to convert the buildings into retirement homes.

Yuhu borrowed 60 million yuan ($9.9 million) in 2011 from Credit China, putting up the empty office development as collateral. But Mr. Ting didn’t want empty office buildings more than 40 kilometers (or 25 miles) from Shanghai’s center.

When Yuhu had trouble repaying its loans earlier this year, Credit China threatened to sue, says Mr. Ting. In response, Yuhu agreed to sell a prized asset—a commercial property in Shanghai—to Credit China at a discount. Yuhu officials couldn’t be reached for comment.

“It’s a perfect time to increase profit,” he says of borrowers who fall behind on their payments. “It’s the pawnshop mind-set: ‘We hope you don’t come back for the Rolex.'”

Credit China has about 74.1 million yuan in past-due loans, or 9.1% of the company’s total loan portfolio. Mr. Ting says he doesn’t consider the loans bad because he could easily seize collateral that would cover them.

Investors aren’t so confident. Credit-quality concerns have dragged down Credit China shares. In Friday trading on the Hong Kong Stock Exchange, they closed at HK$0.65, down 57% from their May 2011 peak of HK$1.51.

As China’s real-estate market cools and competition for a shrinking number of property loans intensifies, Credit China is shifting more attention to another corner of shadow lending. Mr. Ting is expanding his microfinance business in the western Chinese metropolis of Chongqing, with loans of as much as 250,000 yuan—with no collateral required.

Such loans often are used for weddings, car purchases, small businesses and down payments on apartments.

Demand is “growing like crazy,” he says. Credit China’s microfinance loans usually must be repaid in a year and charge interest and fees of about 2.8% per month.

“A guy who makes 10,000 yuan a month deserves a loan, too,” he says. “The property sector eventually will be sucked dry. I don’t want to suck their blood.”