Activist Investors Often Leak Their Plans to a Favored Few

April 9, 2014 Leave a comment

Activist Investors Often Leak Their Plans to a Favored Few

Strategically Placed Tips Help Build Alliances for Campaigns at Target Companies

SUSAN PULLIAM, JULIET CHUNG, DAVID BENOIT and ROB BARRY

March 26, 2014 10:37 p.m. ET

Shares of Rino International Corp. RINO 0.00% sank 28% in the two days after investment firm Muddy Waters LLC put out a report attacking the Chinese company’s accounting.

Three investment firms were ready for the news.

The firms had been tipped beforehand by Muddy Waters about the scathing November 2010 report, according to a person close to the matter, who said one of them made a bet against Rino stock that produced a $1 million-plus profit.

“We sold advance copies of our report,” said Muddy Waters’s founder, Carson Block, adding that since then he has tried to limit advance knowledge of his firm’s research.

For a new breed of “activist” investors, tipping other investors is part of the playbook. Activists, who push for broad changes at companies or try to move prices with their arguments, sometimes provide word of their campaigns to a favored few fellow investors days or weeks before they announce a big trade, which typically jolts the stock higher or lower.

More

Methodology: Analyzing Stock Moves Before Activist Investor Events

In doing so, they build alliances for their planned campaigns at the target companies. Those tipped—now able to position their portfolios for price moves that often follow activist investors’ disclosures—benefit in a way that ordinary stockholders who are still in the dark don’t.

“Premarketing, that’s what they are doing. This is all part of the campaign. They are building a constituency,” said James Woolery, chairman-elect of corporate law firm Cadwalader, Wickersham & Taft LLP, who represents companies against activists. “Some are using, in effect, the pop in the stock price to help pay these people” for being on their side in a coming battle against the target company.

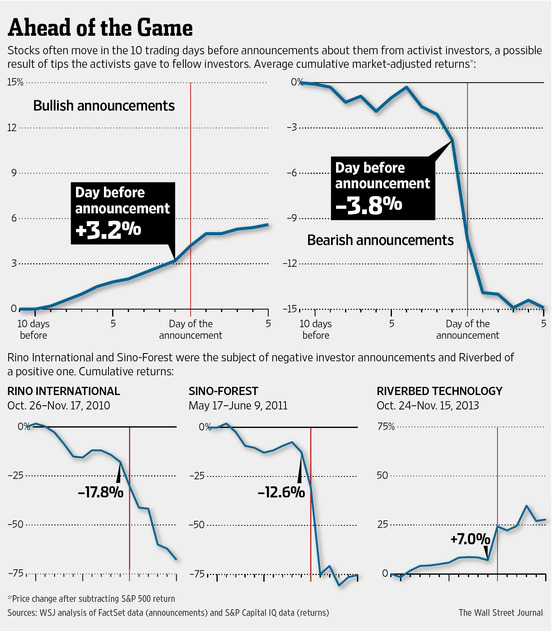

Stocks often move in the days just before activist investors tell the world what they are up to, a Wall Street Journal investigation shows.

In the 10 trading days before bullish activists revealed in regulatory filings that they had bought particular stocks, the stocks rose an average of 3.2% more than the overall market, according to a Journal analysis of 975 announcements by leading activist investors since 2007.

Similarly, an analysis of 43 announcements by bearish activists since 2007 found that in the preceding 10 trading days, shares of targeted companies fell by an average of 3.8% more than the market as a whole.

It is impossible to know how much of the price change is due to activists’ own trading or other factors.

Many lawyers believe that there are few insider-trading risks in one investor tipping another about his plans or actions because this typically doesn’t involve a breach of a duty to keep the information confidential. A spokesman for the Securities and Exchange Commission said he couldn’t recall the agency having brought a case in the area.

But potential legal issues lurk. The SEC requires disclosure in certain instances where investors act together on a particular stock. And the agency recently has been expanding boundaries in its pursuit of securities-fraud cases, some lawyers say.

At first glance, it might seem bizarre for an investment firm to tip others to its intentions. Many large investors do the opposite—striving to hide their moves, through techniques such as breaking up large stock purchases into many tiny ones.

But activists approach stocks differently from investors who simply take a stock position and wait for the market to justify it. Activists—some of whom might have been called corporate raiders in the past—don’t just wait but try to move the stock by disclosing their investment and often making a vigorous public argument about the target company, pro or con.

The role they play can be positive. Bullish activists often pressure management for changes some shareholders welcome, such as repurchasing shares, raising dividends, spinning off noncore business units or selling the company. Bearish activists can expose questionable accounting or other issues. On the downside, companies’ adoption of short-term strategies to avoid being targets can have “very serious adverse effects” on companies, attorney Martin Lipton of Wachtell, Lipton, Rosen & Katz LLP has written.

Activist investors’ clout is growing. They managed $93.1 billion last year, up 42% from 2012, according to a tally by research firm HFR that looked at 67 activist hedge funds.

Some activist investors say that speaking with other investors about their ideas helps them test and refine their investment theses. “I’m happy to give people my thoughts on things I own and I’m happy to learn about how other people think,” said Greg Taxin, who heads the activist strategy of hedge-fund firm Clinton Group Inc. “Putting earplugs in and blinders on isn’t the smart approach.” He said Clinton pursues only “conversations that are permissible under the rules.”

There also is a kind of buddy system among activist investors, some say. Many high-profile investors who know each other don’t want either to get blindsided by another’s investing—or to blindside others.

Lawyers often advise clients it is generally permissible to share information about their trades before announcing them. “In the U.S., information that an investor would have about its intentions is not material nonpublic information that can’t be used,” said David Rosewater, a lawyer who represents a number of activist investors.

Still, there are gray areas that haven’t been tested. Investors whose stake in a company reaches 5%—a level SEC rules require them to disclose—must inform the SEC if they are working as a part of an investor group or have an understanding or agreement with other investors about a stock. If one or more investors collectively own 5% of a stock and are operating as a group, they too are required to disclose that to the SEC, along with their holdings. Such disclosure rules don’t apply to bearish bets.

In recent months, the SEC has increased its focus on activist investors’ moves, including whether there is proper disclosure, a person close to the situation said. Last summer it began looking into whether some hedge funds were working together to try to profit ahead of public disclosure of an investment stake.

The probe relates to the tug of war over nutrition company Herbalife Ltd. HLF +1.61% , which William Ackman of Pershing Square Capital Management LP has bet against and publicly criticized. Last July 31, Herbalife’s stock rose sharply after reports that Soros Fund Management LLC had taken the opposite bet with a large stake in Herbalife.

A couple of days later, according to a person familiar with the situation, Mr. Ackman’s lawyers wrote to the SEC alleging that a Soros portfolio manager, Paul Sohn, had told people at other hedge funds that the Soros firm would soon disclose a 4.9% Herbalife interest, and had urged them to make the same bullish bet. On Aug. 14, the Soros firm disclosed the 4.9% stake.

In a previously unreported development, the SEC has since sent about 25 subpoenas to hedge funds asking for information about their trading in Herbalife, according to people familiar with the investigation. The SEC spokesman declined to comment. So did a spokesman for Soros Fund Management, which manages the assets of billionaire George Soros, his family and their foundations. Mr. Sohn didn’t return calls for comment.

Some leaks occur even when activist investors say they have kept their intentions quiet.

On Nov. 8, Riverbed Technology Inc.RVBD +0.23% shares leapt 16% after hedge-fund firm Elliott Management Corp. publicly disclosed that it held a stake in the company. Before Elliott’s disclosure, information leaked to traders who acted on it by taking a bullish position on the stock, according to a person who was apprised of Elliott’s intentions by a firm with close ties to Elliott.

In the 10 trading days before Elliott’s disclosure, Riverbed shares rose 7%. Elliott continued buying Riverbed shares during the 10 days, a regulatory filing showed.

Elliott sometimes buys a stake, usually 5% to 10%, in a company and then pushes for a sale of the whole company. Before such moves, Elliott at times speaks with officials of private-equity firms about their thoughts on the target company, people close to Elliott said.

Sometimes, Elliott has been on the receiving end of a tip.

Jana Partners LLC, another activist hedge fund, told Jesse Cohn, Elliott’s head of U.S. activist investing, that Jana had taken a stake in Juniper Networks Inc. JNPR +0.23%before news outlets reported this stake on Jan. 23, according to people familiar with the matter.

Though Jana’s investors had already been informed of the stake, and Juniper stock was rising, the stock gained 1.2% more in after-hours trading following the news reports. Elliott, which was already a Juniper stockholder, didn’t increase its Juniper position after the tip from Jana, according to a regulatory filing.

Jana disclosed a 2.7% holding in Juniper in a regulatory filing on Feb. 14. A Jana representative said there is nothing wrong with fellow shareholders talking, adding that the fund firm already had told its investors in advance of what he described as the “alleged conversation” with Elliott’s Mr. Cohn.

Critical research reports that Muddy Waters publishes on stocks often knock them for a loop.

The targeted stocks, however, typically don’t wait for the reports to begin their slide. Twelve companies Muddy Waters has targeted since it began publishing reports in 2010 tumbled an average of 13.1% below the overall stock market in the 10 trading days before its reports came out or the firm’s Mr. Block publicly said he had bet against the stocks.

Among such target companies was Rino International, which sank nearly 18% in the 10 trading days before a Nov. 10, 2010, Muddy Waters report on it.

Before that report on Rino—a Chinese maker of equipment for the steel industry—three investment firms, including hedge fund Oasis Management LLC, paid $20,000 to $25,000 apiece for an advance look at the report, a person familiar with the matter said. Oasis then placed a bet against Rino’s shares, the person said.

When Muddy Waters’s report came out, it alleged that Rino showed “clear signs of cooked books.” Soon after, Rino disclosed a letter from its auditor acknowledging some of the accounting problems raised.

Oasis closed out its bearish bet with a profit of more than $1 million, the person familiar with the events said.

In a statement, Oasis said it “purchases and subscribes to research reports, analysis, and opinions from investment banks and independent research firms,” and follows “rigorous compliance procedures at all times.”

Two and a half years after Muddy Waters’s report, the SEC alleged in a civil complaint that Rino and two of its executives had inflated revenue—allegations they settled without admitting or denying them. A lawyer for Rino declined to comment. A lawyer for the executives said they settled “to put the matter behind them.” Rino’s stock was delisted. It recently traded over the counter at two cents a share.

In another case, Muddy Waters received an idea for a report from a hedge fund and later asked questions that indicated a report could be on the way, the person close to the situation said.

A senior person at Tiger Global Management LLC called Muddy Waters’s Mr. Block in 2011 to congratulate him on an investment success, according to the person, and during the call said he wanted to “talk at” Mr. Block about a Chinese company called Sino-Forest Corp.

The Tiger Global person advised Mr. Block not to respond, saying that any response could make it impossible for Tiger Global to trade Sino-Forest stock because of regulatory compliance issues, the person added.

Some time later, Mr. Block called Tiger Global asking detailed questions about Sino-Forest, which showed he had researched it deeply, the person said. Soon after, Muddy Waters issued a report on Sino-Forest labeling it a “fraud.” Sino-Forest denied the allegation and filed a defamation suit against Muddy Waters and Mr. Block, which Mr. Block said at the time was “without merit.” The suit is pending.

In the 10 trading days before Muddy Waters made its negative report public, Sino-Forest’s share price sank 12.6%. When the report appeared, the stock fell a further 21%, then 64% more the day after that.

Mr. Block, speaking generally and not about Tiger Global, said, “It’s a balancing act for us, because we want to do research as thoroughly as possible without tipping someone off to what we are working on.” Tiger Global declined to comment.

John Courtade, a lawyer for Muddy Waters who is a former assistant chief litigation counsel at the SEC, said, “There’s nothing questionable about investors doing their own due diligence, writing a report, or choosing to speak about some aspect of their work with other investors.”

Sino-Forest faces a regulatory hearing this fall on fraud allegations by Canadian authorities alleging it inflated assets and revenue. Since the Muddy Waters report, Sino-Forest has gone through a court-ordered restructuring and now is a private entity. A lawyer for Sino-Forest declined to comment on the allegations.

After the report, Mr. Block called Tiger Global to thank the manager who provided the initial tip, the person familiar with the situation said, adding that the Tiger Global manager cut him off and refused to acknowledge the earlier conversation.