Investing in higher education; Student numbers are growing worldwide, but profiting is not easy

April 11, 2014 Leave a comment

March 28, 2014 6:18 pm

Intellectual property: investing in higher education

By Adam Palin

Benjamin Franklin once said that “an investment in knowledge pays the best interest”. The structural shifts in higher education in particular, which are seeing new ways of delivering tuition as well as accommodation and finance, present opportunities as well as potential pitfalls for investors.

After enjoying a decade-long boom in student numbers, both domestic and international, UK universities and associated subsectors now face the prospect of stagnating or potentially declining student numbers.

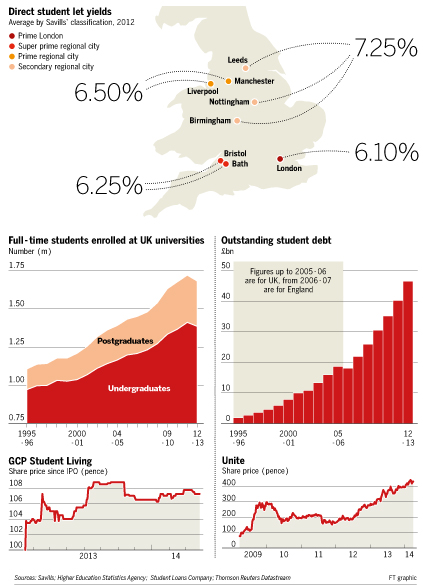

Full-time undergraduate numbers were down 1.9 per cent year-on-year in the 2012/13 academic year, according to the Higher Education Statistics Agency. Full-time postgraduate student numbers fell by 4.2 per cent in the year.

Future growth among domestic students looks set to be curbed by the significantly increased undergraduate tuition fees, which took effect in 2012. Changes to visa laws, placing restrictions on post-study work rights, appear to be restricting demand from non-EU students, especially for postgraduate study.

As well as affecting education providers, the potential effect on the student accommodation market – and any of its unwary investors – could be profound.

Change has already been afoot in the student funding market. Crowdfunding has potential to create competition to the traditional monopolies of lending, banks and the government.

——————————————-

Investing in students

Unlike undergraduate students, postgraduates in the UK are not eligible for low-interest loans from the government-backed Student Loans Company. Banks’ partial withdrawal from the postgraduate lending market during the economic downturn provided space for crowdfunding models, through which students can borrow from those willing to support their degree as an investment.

London-based Prodigy pioneered an alumni investment model that specifically sought to fill the funding gap for students enrolled on MBAs, postgraduate business degrees, which typically cost upwards of £40,000 at renowned business schools

The company’s model is essentially a community education bond, where backers invest in a class of students at one of eight top business schools. Students at partner institutions, which include London Business School and Insead in France, can borrow up to the value of tuition fees, subject to passing a predictive risk assessment.

Although Prodigy originally saw alumni as the main lenders, chief executive Cameron Stevens says that many individual investors have been attracted by yields that have averaged 5 per cent since 2009. Risks are low, he says, because of the high salaries and employment rates enjoyed by MBA graduates from the top schools.

The minimum investment is £10,000. Investors are paid returns every six months over the loan term of eight to nine years, starting six months after the grace study period. Although the bonds are listed and tradable on the Irish stock exchange, there is a limited secondary market.

Prodigy has lent €38m (£31.6m) to more than 1,200 students to date, with 99 per cent of borrowers repaying to schedule. Later this year, Prodigy is set to extend lending to postgraduate engineering students with a view to future lending to science, technology and maths students.

One peer-to-peer lending platform that already extends finance to students enrolled on a range of postgraduate courses is Gradurates. “With most UK banks only lending up to £10,000 [to students], they are not the answer to the postgraduate funding problem,” says chief executive Jothan Webb.

Gradurates, which was established in 2012, only lends to students with a guarantor, usually a parent. Mr Webb says that this provides enhanced security for lenders and upholds the platform’s integrity.

Loans of up to £25,000 are repaid monthly over five years, with only interest payable for the first two years. Individuals can invest anything from £100 upwards in a portfolio of students – currently numbering about 50. Investments are tied in for five years, with monthly repayments. Gradurates charges lenders a flat annual fee of 1 per cent on funds lent out.

In the US, platforms such as Pave and Upstart have gone one step further, allowing lenders to invest directly in borrowers’ own financial success. Borrowers can accept money from investors in return for a percentage of their income over the subsequent 10 years.

As yet, such “human capital contracts” have yet to catch on in the UK, where such models would not be covered by new rules on crowdfunding outlined recently by the Financial Conduct Authority. From April, loan-based crowdfunding platforms will be subject to greater scrutiny from the FCA to ensure transparency for investors, who will only be able to invest up to 10 per cent of their investible assets.

Dennis Hall, a chartered financial planner at Yellowtail Financial Planning, warns that although crowdfunding regulations are tightening up considerably, investment in students remains inherently risky.

Students usually have a very limited credit history and are “untried and untested” debtors, he says, noting that at the point of borrowing, students remain a distance from obtaining their qualification and realising their earnings potential. “You don’t even know whether they will pass their degree.”

——————————————-

Funded by the crowd

Unable to obtain a bank loan, Mario Gintili turned to an alternative means of funding a course that he hopes will launch a career in software development.

Having been accepted to the Makers Academy, a 12-week programme that he hopes will propel him towards a well-paid job in the technology industry, he needed to raise £7,200 for tuition fees.

As a Venezuelan citizen who had just moved to the EU, the 19-year-old did not qualify for a career development loan (these require the borrower to live in the UK for three years first). Following an introduction to the chief executive of Studentfunder, he became the first student to borrow via the crowdfunding platform.

Mr Gintili’s loan of £5,000 came from a pool of individual lenders and was conditional on raising £1,500 through donations. “Through their crowdfunding campaigns students demonstrate their commitment, provide social proof and build their networks,” says Juan Guerra, chief executive of Studentfunder.

Mr Gintili will repay his band of creditors monthly over three years at an interest rate of 6 per cent. As with Gradurates, Studentfunder lenders can invest in a portfolio of students.

——————————————-

Student debt

Undergraduate student debt is set to balloon following reforms that allowed universities in England and Wales to charge tuition fees of up to £9,000 per year.

Almost a million students in England received payment in the 2012/13 academic year from the Student Loans Company for either maintenance and tuition fee loans – 831,100 took both. The SLC lent £7.66bn, 26 per cent more than in 2011/12.

By April 2013, outstanding SLC loans totalled £46.5bn and in this year’s fiscal sustainability report, the Office for Budget Responsibility predicted that net debt from student loans will peak at 6.7 per cent of GDP in the 2030s.

Historically, the UK government has remained the creditor to those who borrowed to finance their tuition costs. But in November 2013, the government took the first step towards student debt privatisation when it announced the £160m sale of selected non-performing student loans.

The debt, which has a book value of £890m, represents the 17 per cent of loans taken out between 1990 and 1998 that remain outstanding. However, ordinary investors are unlikely to be able to access it as an asset class; the buyer, Erudio Student Loans, is backed by consumer debt management group Arrow Global and private equity firm CarVal Investors.

Despite widespread objections, the government intends to dispose of the entire book of student loans taken out before 2012. The first tranche of loans is expected to be sold by 2015/16, according to the Department of Business Innovation and Skills.

Any sale would, however, have to satisfy taxpayer demands for value and reassure students that private ownership will not affect their loan terms. Prospective buyers of the debt will factor in government estimates, revised in December, that 35-40 per cent of student loans will not be repaid.

Student debt levels in the UK are dwarfed by those in the US, where uncapped tuition fees have long been the norm and total debt stands at $1.1tn. The largest student lender SLM Corp, the former government entity better known as Sallie Mae, was privatised in 2004. Its shares trade on Nasdaq.

——————————————-

Accommodation: out with the old…

After being turfed out of university-owned halls of residence – which usually only first-year undergraduates enjoy – students tend to look to the private sector for a roof over their heads, and renting out grotty digs has long been the main way for UK investors to profit from education.

The UK full-time student population has increased by more than 50 per cent over the past 20 years, but there has not been a corresponding increase in the provision of dedicated housing. This demand growth, plus the security afforded by guarantors (usually parents) underwriting monthly rental payments, has attracted ambitious buy-to-let landlords.

Estate agents Knight Frank and Savills forecast average annual returns of 9.2 per cent and 9.3 per cent respectively across the student rental sector for the 2013/14 academic year.

Not all university towns offer equal prospects, however. Robust demand and limited supply ensures the perennial attractiveness of cities like Bristol and Cambridge, which Savills identified among others last year as hotspots for buy-to-let investors. “Risks can be minimised by [investing in] newer properties in central locations”, adds Graham Davidson, managing director of Sequre Property.

There is red tape aplenty; more than three tenants and a landlord needs a House in Multiple Occupation licence, and many councils have become stricter about extending licences.

In many cities, buy-to-let investors face increasing competition from developers of purpose-built residences. Investment in the student housing sector breached £2bn in both 2012 and 2013, according to CBRE.

Marcus Roberts, head of student investment at Savills, says the market is shifting towards purpose-build accommodation and away from older housing stock that is often outmoded and poorly located.

Unite Group is the UK’s largest student housing developer and operator, providing rooms for 41,000 students in 23 cities. Having focused on London during the downturn, Unite is now looking at the regions. Its shares and bonds trade on the London Stock Exchange.

Another company, GCP Student Living continues to focus on London and the Southeast. Tom Ward, a partner at GCP – the first student housing Real Estate Investment Trust – says that international students, who form the majority of tenants in GCP’s purpose-built sites, are keener to pay for high-spec rooms and for 12-month leases. GCP’s shares trade at a 9.8 per cent premium to its net assets.

Collective investing should reduce risk, but investors in two open-ended student housing funds, Brandeaux and Mansion, have not recovered their money since the funds were suspended last July and October respectively due to “liquidity problems”.

For Mick Gilligan, head of fund research at Killik & Co, this illustrates the perils of investing in property via open-ended funds which, he says, are “always going to end in tears.”

——————————————-

Education providers

In the UK, as in most parts of the world, education provision remains predominantly in public hands. Many of the limited number of private providers – including Ashridge Business School and the University of Buckingham in the UK – have charitable status, like the bulk of independent schools.

The UK’s only for-profit university, the University of Law, was created following the 2012 acquisition of the country’s largest provider of legal training for around £200m by Montagu Private Equity. Rival BPP was bought for £300m in 2009 by a consortium led by US-listed Apollo Education Group, the world’s largest provider of MBAs.

Like other major US for-profit companies, including DeVry and Graham Holdings, owner of Kaplan, Apollo has faced a difficult couple of years.

“For-profits have a role in the US education market, but they face pressure on many fronts,” says Carl Salas, senior credit officer at Moody’s Investors Service. Not only have enrolments declined as the US economy improves, he says, but regulatory changes targeting recruitment practices have also had a negative impact.

Enrolment rates in 2013 at Apollo’s flagship University of Phoenix were less than half of those in 2010. And not all those who complete their degrees pay up; according to federal data, three-year default rates among students who graduated from Phoenix in 2009 were 26.4 per cent.

Investing in education, then, is neither as easy or as risk-free as the worldwide growth in student numbers might imply. Or, as Franklin might have put it, the “blunders caused by ignorance…have no limitations.”