Japan’s consumption tax: The big squeeze; A tax goes up while recovery remains fragile

April 11, 2014 Leave a comment

Japan’s consumption tax: The big squeeze; A tax goes up while recovery remains fragile

Mar 29th 2014 | TOKYO | From the print edition

AS IN the rest of Japan, shopkeepers on Jizo-dori, the main street of Sugamo in north Tokyo, are nervously awaiting the effect of an imminent rise in the country’s consumption (ie, sales) tax, from 5% to 8% on April 1st. Keiji Kudo, the president of Maruji, a retail chain, has been devising ways to stave off a drop in sales of the shop’s most popular range, the red underwear which elderly customers buy for the colour’s supposedly health-boosting properties. Last week Mr Kudo began selling vouchers costing ¥2,700 ($26), which from April 1st may be exchanged for ¥3,000-worth of goods. It is the trick of a seasoned retailer, but Mr Kudo complains it will be harder to pull off next time. In October 2015 the tax is scheduled to go up again, to 10%. And Mr Kudo is under no illusion that will be the end of the rises.

Raising the tax is aimed at shoring up Japan’s hugely stretched public finances. Gross public debt stands at nearly 245% of GDP. Yet at a moment when the economy appears to have entered the early stages of a recovery, a contractionary fiscal policy risks stopping it in its tracks. The hope all along was that higher wages for workers could outweigh the tax’s depressing effect. During this spring’s wage negotiations, the prime minister, Shinzo Abe, has put heavy pressure on firms to boost pay. One tabloid newspaper compared his tactics to those of the yakuza, Japan’s gangsters. Even so, firms are lifting base wages by less than was hoped.

Politicians last dared to raise the consumption tax in 1997, when it went from 3% to 5%. The move is widely credited with tipping a fragile economy back into recession. The prime minister of the day, the late Ryutaro Hashimoto, was soon out of office. The lasting trauma for the Liberal Democratic Party (LDP), in government then as now, has left Mr Abe and his people jumpy about the coming rise. The decision to raise the tax was one that Mr Abe inherited from the Democratic Party of Japan under his predecessor as prime minister, Yoshihiko Noda. The government debated hard about whether to reverse course.

This time will be different, economists who support the rise argue. Hashimoto’s dreadful luck was that his tax rise was swiftly followed by a financial crisis in Asia together with a series of local banking collapses. Today, Mr Abe says that he is ready to dash to the economy’s rescue.

Already, the ¥6 trillion or so that the tax rise will take out of the economy is to be put back in the form of one-off supplementary spending of ¥5 trillion, plus tax cuts of ¥1 trillion. Another weapon close at hand is the Bank of Japan. Its governor, Haruhiko Kuroda, is ready to loose a second round of unorthodox monetary easing to reinforce the bank’s initial “shock and awe” campaign from last year to end persistent deflation. Further, the government says the 2015 tax rise will go ahead only if the economy recovers sharply from an expected dip in the second quarter of this year. Meanwhile, there are plans to lower the tax on business profits.

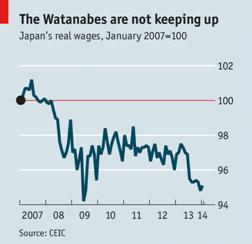

Yet Jizo-dori and shopping districts like it may still suffer. Inflation has been creeping up faster than wages, so spending power for working households continues to decline (see chart). Mr Abe’s monetary and other policies to boost the economy remain popular with voters—but most people have yet to benefit from them. Toshie Hashimoto, a Tokyo housewife, complains that only big companies are enjoying a rebound. After the tax rise she plans to trim her spending on travel, fripperies and even haircuts.

Certainly, employees at large companies have enjoyed most of the gains from Mr Abe’s strong-arm tactics over wages. Large carmakers and electronics manufacturers have announced rises in monthly base pay of ¥2,000-3,500. Yet even that amounts to less than the 2% pay rises Mr Abe was pushing for. What is more, part-timers at big companies and those without regular employment contracts are left out. The smaller firms where most people work, meanwhile, have not profited from a steep fall in the yen as have the big exporters; they are handing out far lower pay increases. Shinichi Fujikawa, an official at Japan’s machinery and manufacturing employees’ trade union, is still negotiating with the parts-manufacturing firms that employ his members. He wants them to get a ¥4,500-a-month rise on top of automatic rises because of seniority but so far he has won only ¥1,630. Ordinary Joes continue to count their coins.