Rich Start-Ups Go Back for Another Helping

April 24, 2014 Leave a comment

Rich Start-Ups Go Back for Another Helping

By DAVID GELLES and MICHAEL J. DE LA MERCED

April 13, 2014

Quora, a question-and-answer website, didn’t need to raise money. It had barely touched $60 million in venture capital that it accepted just two years ago.

Yet the California company, which has no revenue and just 70 employees, recently announced that it had raised an additional $80 million.

The eye-popping investment — for no obvious immediate purpose — was the latest example of a dynamic that is reshaping Silicon Valley: Start-ups, already flush with cash, are piling on the investment dollars.

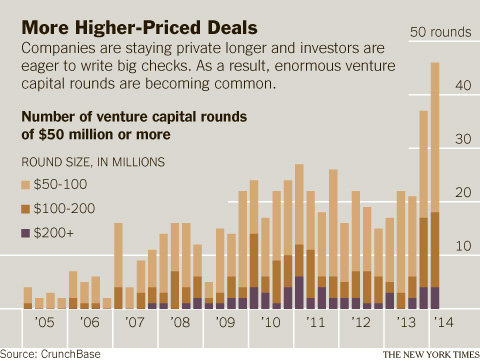

Of the 100 largest venture capital rounds on record, 88 were issued within the past five years, according to CrunchBase, which tracks venture funding. Each delivered more than $50 million to the companies.

“The more capital you have in the bank, the more comfortable and confident you can be,” said Marc Bodnick, a former venture capitalist who now runs Quora’s business operations. “It was really that simple.”

Several factors are driving the proliferation of big late-stage investments. Technology start-ups are staying private longer, venture capital firms are looking to put idle funds to work, and institutional investors are chasing returns in fast-growing private companies.

For technology companies eager to achieve the highest possible valuation on the road to a sale or an initial public offering, this means it is easier than ever to raise megarounds. Truly, it seems, there can never be too much money in the bank.

At the same time, the flood of money is inflating the valuations of early-stage companies and stoking fears of another dot-com bubble.

“There’s a Silicon Valley expression: Eat when the food is passed,” said Nirav Tolia, chief executive of Nextdoor, which last year accepted $60 million in additional venture funding despite having plenty of money in the bank.

Mr. Tolia said that while Nextdoor had no pressing need for the cash, taking the investment gave his company added security and decreased the likelihood that it would simply go up in smoke.

“It’s always good to extend your runway,” he said. “It’s always good to bet on the furthest-out point.”

Late-stage rounds have grown enormously over the past few years. The average size of such investments so far this year was $44.1 million, the highest level in the past five years and up 77 percent from last year, according to data from CB Insights.

This month, Airbnb, the home-sharing site, neared a deal to raise as much as a staggering $500 million from investors like TPG Growth, T. Rowe Price and Dragoneer Investment Group, according to people briefed on the matter. TPG Growth alone had been prepared to provide up to $150 million in the round, one of these people said.

And two weeks ago, Lyft raised $250 million from the likes of the Alibaba Group of China and Daniel S. Loeb’s investment firm, Third Point — despite being widely regarded as significantly behind the leader in the car service industry, Uber.

Some venture capitalists warn that the current rush of big late-stage funding could reduce entrepreneurs’ discipline. A number of investors have pointed to the troubles of Fab.com, an e-commerce start-up that raised $150 million last summer at the tender age of two years.

Facing widespread criticism that the round was too much money too soon, Fab’s chief executive, Jason Goldberg, defended the move as a way to open up new business opportunities. Yet an overambitious expansion plan and falling sales led to a wave of employee exits and a painful retrenchment.

“We had started to dream in billions when we should have been focused on making one day simply better than the one before it,” Mr. Goldberg wrote in a blog post in January.

And Alfred Lin, a partner at Sequoia Capital, conceded that investors were spending less and less time conducting due diligence.

“The speed at which term sheets are being issued is faster,” he said. “We’re playing by slightly different rules than what happened even five years ago.”

One thing that has changed in recent years is the sheer amount of capital available for investment in Silicon Valley start-ups.

Many big venture capital firms have recently raised big rounds, meaning the traditional backers of tech firms are well positioned to write big checks.

But venture capitalists are increasingly being joined by hedge funds and private equity firms chasing huge returns. Among the top investors in fund-raising rounds that collected over $100 million are Digital Sky Technologies and Tiger Global Management, which ranked alongside traditional venture capital firms like Andreessen Horowitz and Kleiner Perkins Caufield & Byers, according to CB Insights.

Also joining the fray are mutual funds like T. Rowe Price and Fidelity Investments. In many cases, such firms are given access to promising start-ups with the understanding that they would remain investors even after an I.P.O.

And some hedge funds are even transforming themselves into so-called growth capital firms that invest in older start-ups. Coatue Management, for example, is planning on raising a $500 million fund devoted to the kinds of investments that the firm has made in companies like Snapchat and the last-minute hotel booking site Hotel Tonight.

“This was impossible 10 years ago,” said Norm Fogelsong, a partner with Institutional Venture Partners, which has made big investments in companies including Dropbox and Snapchat. “There just wasn’t as much money in the venture business. It’s happening because it can.”

Instead of raising just enough money for the next 18 months or two years, companies are now raising all the money they could feasibly need as a private company in one fell swoop.

“In a prior generation, companies would raise just as much money as they needed as they approached the next milestone,” Mr. Fogelsong said. “Today, companies can raise money well ahead of any actual need.”

For the companies receiving the influxes of capital, having so much money in the bank allows them to control their own destiny, rather than be at the mercy of acquirers or the markets.

“If someone wants to buy them, they can turn it down and wait for a higher price,” said Peter C. Wendell, managing director of Sierra Ventures. “If the I.P.O. is looking shaky, they can say, ‘Look at my balance sheet,’ and wait.”

Box, the cloud storage company, has filed to go public at a time when, filings show, it needs to raise more capital. But its rival, Dropbox, recently raised $250 million and may put off its I.P.O., especially as appetite for technology stocks is faltering.

In 2008, HomeAway, the real estate website, was planning to go public. But as the financial crisis began, HomeAway executives decided to postpone the I.P.O.

Instead, in November of that year, HomeAway raised $250 million in additional venture capital and resolved not to think about going public for at least two years.

“It allowed us to reset the clock,” said Lynn Atchison, HomeAway’s chief financial officer. The company finally went public in 2011.

HomeAway is not alone. The average age of companies going public today is 10 years, in contrast to the average of just six years in 2000, according to Jay R. Ritter, a professor at the University of Florida.

“Rounds that would have otherwise gotten done in the public markets are getting done in the private markets,” said Scott Kupor, partner and chief operating officer of Andreessen Horowitz, a venture capital firm that is among the most active participants in big late-stage rounds.

These longer incubation periods mean many companies do need more capital for operating expenses. For example, companies that focus on on-demand services, like the car ride companies Uber and Lyft, require capital as they build out their dispatch networks in new cities and offer new products.

And on average, between a quarter and just under a third of the late-stage money is being used to buy shares from employees and early investors ahead of an I.P.O.

Mostly, however, companies are collecting the additional money simply because they can, taking advantage of an ocean of ready cash.

“We are not trying to generate return on that raised capital,” said Mr. Tolia of Nextdoor. Instead, he said, his company’s latest venture funds would be invested in money market accounts and left all but untouched.

For venture capitalists, allowing portfolio companies to take on more funding means their existing stakes can be diluted. But since these big rounds often lead to much higher valuations, many investors don’t mind.

In the case of Quora, the new round valued the company at a reported $900 million, more than double the previous valuation of $400 million. That means that while some early investors may have seen their ownership diluted by the new round, the value of their holdings nonetheless soared.

“When it goes off at a high price, the V.C. gets to change the price of the other stock on his books,” said Mr. Wendell of Sierra Ventures.

The result is that much of a company’s gain in value is happening before it even goes public.

“Appreciation that normally would have happened in the public market is happening in the private market,” said Mr. Kupor of Andreessen Horowitz. “This is why we see T. Rowe, Fidelity and JPMorgan investing. They’re saying, ‘There’s not a lot of growth for us in the public market.’ ”

And while this has made for a frenzied investment environment in Silicon Valley, it is also raising new questions about who benefits from the booming success of the technology industry.

“There’s a broader public policy question here,” Mr. Kupor said. “There is a wealth transfer happening, from public investors to private investors. And the benefits are accruing to the investors that can access the private markets.”