The Lok Sabha of dreams

April 24, 2014 Leave a comment

David Keohane | Apr 14 09:58 | 7 comments | Share

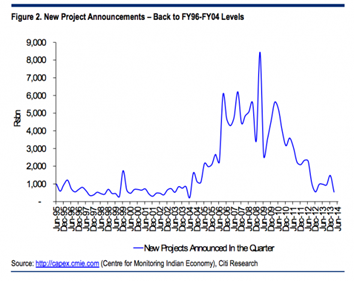

If we come, will they build it? Here’s the Indian economy charted, by Citi:

A slight exaggeration we grant you but there is so much focus on infrastructure and capex at the moment that it’s really not far off. The lack of decent infrastructure in India is a perennial problem and stalled infra projects lie behind a large number of bad loans clogging up the banking system.

The broad hope is that, as Goldman said a little while back, a positive cycle can be unleashed if projects get unclogged, increasing cash flow for infra companies (which account for 30 per cent of stressed loans), enabling loan repayments, and healing bank balance sheets, which can allow a fresh lending cycle to start.

While the specific hope is that a shiny new BJP-led coalition will kick-start that virtuous cycle as projects are unblocked and investments waved through a la Modi’s creation tale of Tata in Gujarat. The good news if you are of a Modi-persuasion is that the first part of that hope — the BJP led government bit — is looking very likely. *insert dodgy poll caveat here*

Sadly the second half — the bit where projects get unblocked with speed and ease — is not so likely a scenario, as the following chunk from JP Morgan details (with our emphasis) and which the BJP’s manifesto doesn’t really deal with:

The belief in certain quarters is that as long as the next government were to go all out at de-bottlenecking projects, sentiment would surge and this would spark an investment revival in the economy. However, this appears to be an overly-simplistic read on the situation for at least three reasons.

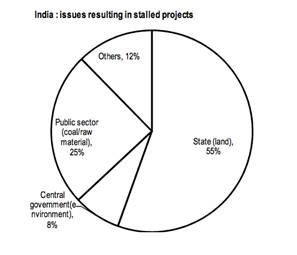

First, the vast majority of projects are currently stuck because of issues that are under the purview of state governments, over which the central government has little jurisdiction. Currently, the Center for Monitoring the India Economy (CMIE) lists 733 projects under implementation that are stalled. Of these, the top 50 projects in value terms account for 67% of the total value of stalled projects.

We undertook an analysis of what’s constraining execution of this sample of 50 projects to better understand how much leverage any new government would have in de-bottlenecking them. The results are not particularly encouraging. Almost 55% of the projects—in value terms—among this sample were stuck because of state-related issues. 46% of these projects were stalled on account of land acquisition—the single biggest constraint—which is a state subject. And the remaining 9% on account of contractual and legal issues relate to individual states. So these are constraints over which the central government has no jurisdiction.

In comparison, only 8% of project value was stuck on account of environmental clearances, which are directly under the purview of a central government and could, in theory, be immediately addressed by a new government. This smaller fraction likely reflects that high-value projects that were only stuck on account of environmental clearances have likely already been addressed by the CCI.

Another, 25% of projects were stuck on account of not being able to attain coal, gas, and other raw materials. In theory, central government policy could facilitate access to raw materials but, as we discuss in more detail below, the experience of the last year has shown that the problems in the power sector are more complex. Prodding Coal India Limited to accelerate production is not a trivial task. And if firms are allowed to import coal and pass on these higher costs, few state electricity boards (SEBs) seem to be buyers given their inability to further pass this on to the final consumer and accept any further losses on already-stressed balance sheets. With SEB pricing being a state issue, the central government’s ability to de-bottleneck projects in the power sector remains very limited, evident by declining plant load factors of SEBs.

But what about the projects the Competition Commission of India has already cleared, you say? Won’t those translate into execution on the ground, lift sentiment, and start said sorely hankered after virtuous cycle? Well… no, say JPM:

To be sure, the current government deserves credit for taking up approvals on a war footing and clearing 5% of GDP in projects. But an analysis of what’s been cleared reveals that a significant fraction is in the power sector, which is riddled with familiar issues. For example, many power projects that have been cleared in effect mean environmental clearance have been obtained and fuel supply agreements (FSA) have been signed, and, in some cases, higher imported coal prices have been allowed to be passed on.

But for this to matter economically, someone has to buy and use this power. While SEB plant load factors have ticked up in recent months, they have been declining over the last three years. Some of this is undoubtedly because economic growth has slowed over the last two years. But the sub-optimal plant-load-factors (PLFs) more generally reveal the inability of the SEBs to buy more expensive power and sell it below marginal cost, given their stressed balance sheets. Also, bank lending to the power sector has tailed off sharply, revealing the reluctance of banks to lend to financially-vulnerable SEBs. What’s needed both is sustained rationalization of state power-tariffs and an aggressive push to increase coal production by Coal India Limited (CIL). The former is a state specific issue, and while clear progress has been made across several states, SEBs are still running losses and power tariffs will have to rise further. Jumpstarting coal production will not be trivial barring a revamp of the Coal Nationalization Act, which would be a thorny legislative challenge for any new government.

Even more s0, lets pretend that all of that didn’t matter and everything was waved through, there is a still question as to how any new capex cycle would be financed. A last bit from JPM:

There has been an alarming increase in leverage ratios across all the key infrastructure areas, with debt-equity ratios at a ten-year high. Among the BSE- 200 NON- financials, 17% have operating incomes (before depreciation, interest and taxes) that are less than the perilous threshold of 1.5 times their debt service obligations. So a significant deleveraging would need to be undertaken before these infrastructure companies have the balance sheet strength to finance another investment cycle. If economic growth were to accelerate and capital markets become buoyant, the speed of deleveraging could accelerate as companies issue fresh equity and sell assets that will be higher-valued. But, at best, this is a multi-quarter process that would militate against sudden lift in capex cycle.

The corollary of this corporate stress is that banks are facing ever-rising impaired loans, which has constrained their capital. Public sector banks – which account for 70% of banking sector assets – are saddled with the overwhelming majority of impaired loans, and would need a significant quantum of capital injection by the government – far in excess of what has been budgeted – to finance any large pick-up in credit growth. The risk aversion on the part of banks is showing up in credit growth to infrastructure moderating, even as they continue to hold government securities (29% of deposits) significantly above (23%) that is mandated. Accelerated recognition of the NPA stress among public sector banks and a recapitilzation of the budget would go a long way in reducing risk aversion and financing any capex cycle, but fiscal constraints preclude any such decisive recapitalization for now.

All told, the fact that most implementation bottlenecks lie within the realm of state governments over which the Center has little leverage, and there is a significant debt overhang facing the infrastructure sector and public sector banks, suggests that expectations of a sharp and sustained pick-up appear optimistic at least in the coming quarters.