When is reform of a Chinese state-owned enterprise not reform at all? When it’s not going to create value

April 24, 2014 Leave a comment

SOE this is what passes for reform?

| Apr 14 14:29 | Comment | Share

When is reform of a Chinese state-owned enterprise not reform at all?

When it’s not going to create value.

Arguably, for example — when it’s really a reverse merger that allows a parent to tap international capital markets and bail out a struggling subsidiary that lost heavy in Australian iron ore mines. Arguably, we said.

Or — an oil major selling a third of its enormous marketing segment to state-backed pension funds, in order to access private capital and boost its already dominant position. Again, arguably.

Here’s that latter case — let’s call it the Sinopec conjecture — charted by Macquarie:

But we’ll come back to that. First it’s worth noting that belief in real SOE reform in China is rooted partly in Sinopec’s sale.

It’s true the Third Plenum last year did call for reform in typically generalised terms — for a “diversified ownership model”, for moves to categorise SOEs into “competitive” and “strategic” industries, for raising the efficiency of SOE management via incentives such as options (and firing for incompetence?), and for SOEs to pay higher dividends. But the overall message was muddled.

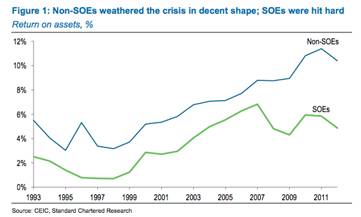

As Standard Chartered’s Stephen Green said, diversification of China’s SOEs has been going on for the past two decades. Even so, the Plenum went ahead and recognised them as the “main pillar” of the economy. Not exactly an excoriating cry for change in the face of this kind of performance:

So when Sinopec’s sale was announced a few months later, it was quickly taken as a signal of real reform backing up the Plenum’s generalities — a signal that allowed it to outperform its peers, presumably on the assumption that value was about to be unlocked by new retail investors as the company was rebalanced.

But, say Macquarie, that is all basically tosh:

We understand why the market liked the headlines but when it comes to longer-term fundamentals we viewed the sale announcement as supportive for our view that Sinopec is precariously poised; that its combination of ongoing negative free cash flow, dividend commitments and relatively high financial gearing left it with limited options outside of selling assets or raising funds in some other potentially minority-dilutive way…

We think more pragmatic explanations for the proposed sale include:

Delay real reform. The proposed sale ticks the politically-attractive ‘reform’ box whilst giving up no control and allowing no new competition.

It’s needed to finance the dividend. Without any asset sales Sinopec has negative free cash flow, high financial gearing and will struggle to meet its dividend payout commitment.

Allow upstream/downstream rebalancing. Indeed – but at the likely cost of destroying value, in our opinion.

Allows mega-scale industrial projects to proceed. For example, coal-to-gas in Xinjiang and an associated 8,000kms gas trunkline, which need c.US$30bn in capex.

Will likely give a large one-off gain on book value.

And it is hard to see how selling a core business that generates lots of quality free cash flow for Sinopec — 72 per cent of group cash flow and 40 per cent of group EPA per annum over the past three years — can create value. If anything it should be the non-core and upstream bits where hidden value is lurking. And it’s not as if those new 30 per cent owners (with no guarantee of expertise) are going to be allowed to shake things up.

More specifically, Macquarie argue that the scale of hidden value implied by the current share price is at least debatable, and could well be less than zero. Further, in the absence of any credible plan to sell a majority stake and give control to genuine new independent owners, they think there is every likelihood that equity markets will de-rate the remaining unsold 70 per cent of retail to something less bullish than the current 10x EV/EBITDA scenario, once the dust has settled.

Then there is the question of the sale proceeds. Most likely, say Macquarie, is that value effectively flows from the new marketing investors to Sinopec’s parent and sister E&C companies, with little remaining in listco. See the chart above and reflect on where that cash will end up. A last chunk from Macquarie:

The good – a special dividend. The one use of proceeds that arguably does create value is a special dividend – if a high market sale multiple is achieved then arguably investors could take that cash and redeploy it into other investments that will generate better returns (e.g. 6%+ if 10x EV/EBITDA sale price is achieved) for the same or less risk. However we think the chances of Sinopec giving anything more than a token special dividend (if any) are low – the other opportunities are likely to prove too hard to resist.

The likely not so value-accretive…

US$6.6bn – plug the hole in 2014e cash flow. We calculate the hole in 2014e at US$2.8bn of negative free cash flow and the US$3.8bn required to pay dividends. The point is investors already expected these dividends and no one (apart from us, apparently) thought the company would have start cannibalising itself to pay them.

Parent M&A – US$43bn of mixed quality assets are waiting with the parent. Sinopec’s oil production accounts for > 50% of its EBIT and is declining at an underlying rate of between 10-20%. Major gas projects (e.g. Puguang, Yuanba and Fuling) can alleviate, but not fully offset this headwind. The parent has US$43bn of E&P assets sitting on its balance sheet (see fig 14); an eclectic mix scattered around the world. Within that list we Brazil (ex-Repsol and Galp) assets seem potentially interesting; they are material, in an attractive hydrocarbon province and were bought for a fair price – but would require several years of heavy capex before any returns. Beyond that we mainly see assets that are too small, or in regimes too risky, or were bought at too high a price by the parent (we assume they can’t be sold to listco at less than book value).

US$11bn – Coal-to-gas: move forward with the US$11bn (initial estimate) proposed Zhundong 8bcm coal-to-gas project in Xinjiang (North West China). Wood Mackenzie calculates that Xinjiang CTG delivered into Guangdong needs $13/mscf city-gate gas prices to breakeven – i.e. around the current industrial Shenzhen price level, but well above average city-gate prices. Datang Power is reported to be looking at a project IRR of merely 6% on its US$4.2bn Keqi CTG project in Inner Mongolia.

US25bn – an 8000km gas pipe: An 8000km Xinjiang-Guangdong-Zhejiang 30bcm gas pipeline, required to help the Xinjiang CTG project breakeven.

Coal to liquids – with US$20bn+ available to spend, we think Sinopec will find it hard to not consider ramping up coal-to-olefins efforts, which so far have been only at experimental volumes.

The next wave of refinery fuel quality upgrades. By end of 2017 diesel and gasoline is scheduled to meet ‘China V’ standards (the main change being sulphur content falling from 50ppm to 10ppm). This requires more hydro-desulphurisation units and/or hydrocrackers, at capital costs up to $10k per flowing bbl. It is unclear to us how much more desulphurisation capacity Sinopec needs to add on top of what its already done (we’ve asked…), but if we assume 20% of the company’s capacity still needs to be upgraded then that equates to c.US$10bn in total – equivalent to about half of our forecast ongoing annual refinery capex budget from 2014-17. Such upgrades around the world have usually resulted in value destruction for the shareholders – the reality is that cleaner fuels have not in general generated the extra revenues required to justify the mandated investments and higher running costs.

So, as asked before, how does this ‘mixed-ownership monopoly model’ represent real progress rather than a way to get private capital into a behemoth of an SOE?

It looks like sideways reform rather than the real thing — which might be, say, dismantling Sinopec’s refining and marketing business and splitting them into several new, competing companies, splitting up the upstream business, or ceding real control via joint ownership or foreign participation.

The thing is, as Green at SC noted before, the incentives that SOE managers, SASAC bureaucrats and local government leaders all have to resist reform shouldn’t be forgotten. It’s their salaries on the line after all. And that is equally true for Sinopec. Like all Chinese companies it has been rewarded for adopting bigger and bigger monopoly positions — corporation creep in closed systems makes sense — and real reform would obviously involve reductions.

Potemkin reform, maybe, is the best way to describe what we’re getting so far even if it threatens to sometimes go further and, let’s face it, will eventually have to.