Comeback Kid and Reinventing the Family Business

October 4, 2014 Leave a comment

“Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | September 30, 2014 |

Bamboo Innovator Insight (Issue 52)

|

|

Can You Guess This Asian Wide-Moat Company? Comeback Kid and Reinventing the Family Business Our latest monthly Moat Report Asia for October investigates an Asian-listed company who is the#1 healthy niche snack king in its domestic market with a market share of >73%. The company has spent over 30 years to build up an extensive wide-moat nationwide distribution network penetrating 200,000 Point-of-Sales (POS), including both modern trade (MT) (supermarkets,hypermarkets, convenience stores, gas stations, wholesales stores) and traditional trade (TT) (sundry stores, traditional shops). The company cultivates long-term customer relationships with its strong direct sales team of 200 professionals regularly visiting the stores with over 400 vehicles, comprising of trucks and the innovative mobile cash vans.

We observed that super compounders Ecolab (ECL, MV $34.8bn) and Keyence (6861 JP, MV $26.7bn) have a strong solutions-sales specialist team and we think this Asian company has accumulated deep know-how infused in its direct salesforce team over the years to sustain resilient growth. The company distributes 5 product categories: (1) Snacks eg the Japanese snack brand Calbee; (2) Confectionery, (3) F&B, (4) Medicine, pastille, nutrition food, (5) Personal care and household products. 75% of its sales are domestic while the rest are exported, mainly to Japan (20% of sales).

The company empowers its salesforce, particularly those traveling on mobile sales vans, with the utilization of modern technology in receiving orders, data verification, issuance of sales documents, delivery of goods. The company has created a sophisticated product storage and inventory management system and a delivery system that is flexible, convenient and fast. In terms of inventory management and working capital efficiency, the company performs far better with inventory period at 23 days (comparable peer 73 days) and cash conversion cycle (CCC) of 33 days (comparable peer 89 days). These long-term competitive advantages have translated to a superior ROE of 27.7% and sustainable cashflow generation.

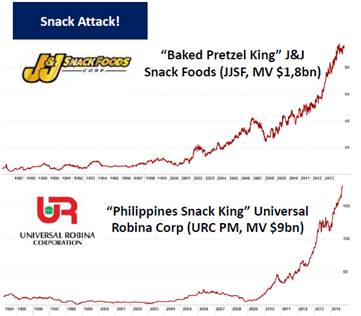

Even when compared to Asian MNC giants Universal Robina Corp (URC PM, MV $9bn) and Calbee(2229 JP, MV $4.3bn) who have scale advantages in cost efficiency and pricing power, the company has surprisingly better fundamental performance in ROE and profitability and is trading at a huge relative valuation discount at its current EV/EBIT 10.7x and EV/EBITDA 10.4x. Net cash at 9% of market value is a healthy reserve that can be productively allocated to capitalize on future growth opportunities without straining the balance sheet. Its attractive 5.6% dividend yield, the highest in the industry, also limits short-term downside risks.

Its unique low-fat high-protein healthy snack and wide-moat distribution network makes the company either an attractive takeover target or long-term strategic partner to the giant snack producers from URC to Mondelez and General Mills, thus providing long-term downside protection in its terminal value.

Organic food and healthy snack company Annie’s was acquired In Sep 2014 by General Mills for $820M at Price/Sales 4x (vs the company’s P/Sales 1.5x), following similar moves by General Mills, Kellogg, Campbell Soup, Hillshire Brands, Tyson Foods, JM Smucker, TreeHouse Goods, WhiteWave etc. The trend of forgoing meals in favor of healthy snacks is accelerating.

It is the flagship vehicle of a family business group whose storied history has been long forgotten following unusual succession challenges in the third generation. Led by the capable son-in-law to the daughter of the third-generation scion, the Group is the ‘comeback kid’ who has successfully resurrected from the 1997/98 Asian Financial Crisis and has listed 4 of its 6 major business assets to derisk the business group governance risk and instill a strong sense of accountability and transparency for long-term going-concern viability. As the flagship vehicle, this Asian listed company will be the most important vehicle in the Group to equitize the governance goodwill and long-term strategic partnerships seeking to leverage its wide-moat distribution network and global export potential. We are impressed by the company’s efforts over the years to develop its human capital in caring about their knowledge by providing them training opportunities and multiple opportunities to engage in company activities to foster sharing and commitment. This is rare in Asian firms and the company deserves credit and a long-term valuation premium.

Warm regards, KB Managing Editor The Moat Report Asia SMU: http://accountancy.smu.edu.sg/faculty/profile/108141/Kee%20Koon%20Boon

|

| The Moat Report Asia |

|

“In business, I look for economic castles protected by unbreachable ‘moats’.” – Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia. Together with our European partners BeyondProxy andThe Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produce The Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times. Our Members from North America, the Nordic, Europe, the Oceania and Asia include professional value investors with over $20 billion in asset under management in equities, secretive global hedge fund giants, and savvy private individual investors who are lifelong learners in the art of value investing.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our subscribers. Questions range from:

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps.

|

| Professional Development Workshops for Executives and Lifelong Learners |

|

Our 8th run of the series of workshop From the Fund Management Jungles: Value Investing Exposed and Explored – (Part 1) Moat Analysis, (Part 2) Tipping Point Analysis and (Part 3) Detecting Accounting Fraud – on 14 June 2014 has been well-received with serious value investors, professionals, and serious lifelong learners attending, with some who flew in from Jakarta and KL!..

Our 9th workshop will be sometime later in the year.

Thank you for your support all this while!

|

|

Thank you so much for reading as always.

Warm regards, KB Kee Managing Editor The Moat Report Asia Singapore Mobile: +65 9695 1860

A Service of BeyondProxy LLC 1608 S. Ashland Avenue #27878 Chicago, Illinois 60608-2013 Other offices: London, Singapore, Zurich

|

|

P.S.1 Here is a little more about my background: KB Kee has been rooted in the principles of value investing for over a decade as an analyst in Asian capital markets. He was head of research and fund manager at a Singapore-based value investment firm. As a member of the investment committee, he helped the firm’s Asia-focused equity funds significantly outperform the benchmark index. He was previously the portfolio manager for Asia-Pacific equities at Korea’s largest mutual fund company.

He holds a Masters in Finance and degrees in Accountancy and Business Management, summa cum laude, from Singapore Management University (SMU) and had also published articles on governance and investing in the media, as well as published an empirical research paper Why ‘Democracy’ and ‘Drifter’ Firms Can Have Abnormal Returns: The Joint Importance of Corporate Governance and Abnormal Accruals in Separating Winners from Losers in the Special Issue of Istanbul Stock Exchange 25th Year Anniversary Best Paper Competition, Boğaziçi Journal, Review of Social, Economic and Administrative Studies, Vol. 25(1): 3-55. KB has also presented his thought leadership as a keynote speaker in global investing conferences. KB has trained CEOs, entrepreneurs, CFOs, management executives in business strategy, value investing, macroeconomic, industry trends, and detecting accounting frauds in Singapore, HK and China, and had taught accounting at the SMU where he is currently an adjunct lecturer.

P.S.2 Why do I care so much about doing The Moat Report Asia for you? My personal motivation in embarking on this lifelong journey has been driven by disappointment from observing up close and personal the hard-earned assets of many investors, including friends and their families, burnt badly by the popular mantra: “Ride the Asian Growth Story!” I witnessed firsthand the emotional upheavals that they go through when they invest their hard-earned money – and their family’s – in these “Ride The Asian Growth Story” stocks either by themselves or through money managers, and these stocks turned out to be the subject of some exciting “theme” but which are inherently sick and prey to economic vicissitudes. They may seem to grow faster initially but the sustainable harvest of their returns is far too uncertain to be the focus of a wise program in investment. Worse still, the companies turned out to be involved in accounting frauds. Their financial numbers were “propped up” artificially to lure in funds from investors and the studiously-assessed asset value has already been “tunnelled out” or expropriated. And western-based fraud detection tools and techniques have not been adapted to the Asian context to avoid these traps.

After a decade-plus journey in the Asian capital jungles, it has been somewhat disheartening as I observe many fraud perpetrators go away scot-free and live a life of super luxury on minority investors’ hard-earned money. And these perpetrators make tempting offers to various parties in the financial community to go along with their schemes. When investors have knowledge in their hands, we have a choice to stay away from these people and away from temptations and do the things that we think are right. With knowledge, we have a choice to invest in the hardworking Asian entrepreneurs and capital allocators who are serious in building a wide-moat business.

|

| CONNECT WITH US |

| MOAT REPORT ASIA OUR TEAM SUBSCRIBE MEMBERS CONTACT US

The Moat Report Asia Other offices: London, Singapore, Zurich |