Being Strong and Resilient in a World Where Things Go Wrong: The Case of Mahindra & Mahindra, a Different Sort of “India’s Berkshire Hathaway” – Bamboo Innovator Weekly Insight

July 27, 2015 Leave a comment

| “Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | July 27, 2015 |

Bamboo Innovator Insight (Issue 93)

|

| Dear Friends,

Being Strong and Resilient in a World Where Things Go Wrong: The Case of Mahindra & Mahindra, a Different Sort of “India’s Berkshire Hathaway” “Deere John, I have found someone new.”

Would Buffett’s decision to invest in Deere change if he had known about the story of the Asian wide-moat innovator behind this ad? Buffett had disclosed in March 2015 that he had built up in 2014 a 5% ownership in Deere, which has paid steady or increasing dividends since 1987, giving it a streak of 28 consecutive years without a dividend reduction. Since this 2007 ad and losing the #1 title, Deere is up around 10%, underperforming the 40% rise in the S&P 500 index. Mahindra & Mahindra (NSI: M&M) – Stock Price Performance 1994-2015 Vs Nifty index and Deere

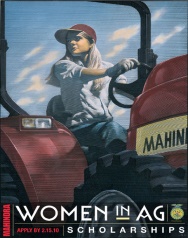

This Asian innovator is Mahindra & Mahindra (NSE: M&M, MV $12.9bn) who recently acquired a 33% stake in Mitsubishi Agricultural Machinery, a subsidiary of Mitsubishi Heavy Industries (TSE: 7011 JP, MV $19bn), for about $25m in May 2015. The popularity of M&M’s tractors stemmed from producing sturdy low-powered tractors (under-70 horsepower) suited for fragmented landholdings in India and China. M&M realized that there is an underserved market in the United States to which its low-powered tractor is well-suited: hobby farming. Baby boomers are retiring from stressful urban lives in California to places like Arizona where for the price of a luxury condo in San Francisco, they can buy over 15 acres of land, ideally suited to tilting by hobby farmers and suburban lawn masters who don’t need a monster tractor and like M&M’s reliability. Many of M&M’s customers in the United States are women, hence the “Deere John” ad. Flying under the radar of Deere when it first entered US, M&M built close relationships with small dealerships, particularly family-run operations. Rather than saddle dealers with expensive inventory, M&M allowed them to run on a just-in-time basis, offering to deliver a tractor within 24 to 48 hours of receiving the order. M&M also facilitated financing. In return, Mahindra benefited from the trust the dealers enjoyed in their communities. M&M also built close relationships with customers. Some 10 to 15% of M&M tractor buyers got phone calls from the company’s president, who asked whether they were pleased with the buying experience and their new tractors. M&M also offered special incentives such as horticultural scholarships to neglected market segments such as female hobby farmers. Following the example of Hyundai Motor (KOSPI: 005380), which used especially long product warranties to gain acceptance in the American auto market, Mahindra offers a five-year warranty on its tractors in the US, compared with the standard two years offered by Deere. M&M has also rolled out a military appreciation program providing U.S. and Canadian veterans and their families with $250 rebates, with its website stating: “We appreciate your service and commitment to our country and would like to show our support.”

M&M was founded as a steel trading company in 1945 by K.C. Mahindra, J.C. Mahindra and Ghulam Mohammed, under the name Mahindra & Mohammed. Mohammed in 1947 migrated to Pakistan to become its first finance minister. M&M entered automotive manufacturing in 1947 to bring the iconic Willys Jeep on to Indian roads. Besides holding the #1 title for tractors, M&M is also the #1 SUV maker in India. Now, M&M is present across the entire automotive spectrum – two-wheelers, commercial vehicles, SUVs and sedans. Whether it is tractor or SUV or two-wheelers, the M&M brand is defined not by horsepower or engines, but instead by the fact that it stands for ruggedness, few frills, no-nonsense performance and an honest price tag. “M&M psychographically is about safe, strong, powerful, rugged vehicles, irrespective of the segments.” Today, M&M is a diversified conglomerate who employs over 180,000 people around the world and operates in industries such as automobiles, defence, aerospace, information technology and BPOs, financial services, hospitality and retail; the automotive & tractors business continues to be the largest contributor at two-third of group revenue. “We don’t call it a conglomerate, we call it a federation,” Anand Mahindra says. “If you look at a spectrum between General Electric and Berkshire Hathaway, GE is a conglomerate, one single monolithic company with divisions, Berkshire Hathaway has multiple investments. M&M is more Berkshire Hathaway than GE.” Anand focused on having independent presidents who would focus on their line of business, segmented in six areas: auto, technology, hospitality, retail, defence and aerospace, and steel. “These six new sub-entrepreneurs have made significant gains in their own wealth because they share the business,” Anand says. Anand looks for niches. It’s a contrast to the business strategies followed by some leading business houses in India. Anand cites the example of Reliance Industries – the company wants to dominate competition with its size. This is not M&M’s strategy. Also, there is a central pool of money that can be used in different businesses. In the M&M Group, each company has its own balance sheet and its own cash flow to fund growth. Anand’s mantra is not about winning all the time, but to ensure that failure does not cripple. Anand has the vision to build a live, growing organisation—one that can evaluate, incubate, build and scale up businesses continuously that can escape gravity and transcend boom-bust business cycles, even while the flops fall by the wayside. Each company is ring-fenced from the damage failure elsewhere can do, even while being free to finance its own growth and make its own mistakes, to grow and find its own capital without betting the whole ranch. M&M, the flagship, is the major shareholder and the spine of the structure – the lever that makes things work. Mahindra sees his role as group head to assess risk with a team. “Measured risk-taking is at the heart of entrepreneurship,” Anand says. M&M’s approach is “segmented strategy”. M&M’s annual War Rooms are where crucial go-or-no-go decisions are discussed and decided. These are high-powered forums meant for interaction with individual companies that form the Mahindra federation. Anand Mahindra is J.C. Mahindra’s grandson. Anand Mahindra joined the group’s Mahindra Ugine in 1981 after finishing his MBA from Harvard. Businesses in India were governed by the licence raj, where the government would select five to six companies to make or sell in any segment. Mahindra Ugine, headed by Anand’s father Harsh, was one of the six players which had licence to make specialised steel products for electric arc furnaces. As Anand recalls, “It was a cosy market, and nobody cared that I had joined”. But suddenly, in 1981, the government gave licences to 36 players to make electric arcs. As a result there was excess competition, something which Indian business houses were not used to. Prices plunged and there was surplus capacity in the sector. Ugine did not cut price and sales plummeted and the company posted its first loss. “When all hell broke loose, it was an opportunity for somebody new,” Anand Mahindra says, who turned around the company gradually by selling inventory and squeezing the supply chain. Anand went on to take over as head of the group’s flagship vehicle business in 1991, even though his uncle and K.C. Mahindra’s son, Keshub Mahindra, was still the chairman. When India liberalized in 1991 Mahindra was sprawling and flabby like many of its peers—making everything from jeeps to lifts. After liberalisation, there were rumours of M&M businesses winding up. No one thought that Indian automakers would survive with companies like Ford, Daewoo and General Motors coming to India. What Anand found at M&M’s vehicle manufacturing business shocked him: an almost complete lack of integration among the departments and the needs of the customer were completely ignored. In short, everything has gone wrong for M&M during that turbulent period.

Anand was attempting to turn around the business… <ARTICLE SNIPPED> ******** Interestingly, Anand has his own unique view about innovation as the engine to drive the M&M federation. Anand believed that low-cost innovation is essential for solving many problems facing India. Yet, he believed that the famous concept of “jugaad” should not be confused with frugal innovation: “India desperately needs big innovations to address large-scale problems and make use of opportunities in the country and not just stick to the now famous concept of `jugaad’. It really bothers me that we have become so smug about `look, how good we are’. `Jugaad’ means you use whatever little resources you have and make something happen. Jugaad does imply a positive ‘can-do’ attitude, but unfortunately, also involves a ‘make-do’ approach. It can, hence, lead to compromises on quality and rarely involves cutting edge or breakthrough technology. ‘Constraint-led Innovation’ is a better approach. It targets the most advanced technology but with a philosophy of ‘more for less’. The time has come for India to move from ‘jugaad’ (somehow) to ‘jhakkas’ (superb).” Thus, with the “constraint-led innovation” embedded by Anand Mahindra into the company’s culture that propelled M&M forward over the years since the turbulent period of India’s liberalization, this different form of “India’s Berkshire Hathaway” has been able to recover from shocks and stresses and to adapt and grow from disruptive experiences, creating and taking advantage of new opportunities in good times and bad. Just like the values of the Bamboo Innovator, bend not break even in the wildest of storm, staying strong and resilient in a world where things go wrong. Read more about the story of “India’s Berkshire Hathaway” at the Moat Report Asia: http://www.moatreport.com/updates/ Warm regards, KB The Moat Report Asia A new monthly issue of The Moat Report Asia is now available! Access the in-depth idea presentation: http://www.moatreport.com/members/ This month of July, we highlight Asia ex-Japan’s largest maker of a mission-critical automotive electronics part that is dubbed the “nervous system” in cars whose electronic content is rising due to the Green, Connected, and Autonomous automotive trends. Without this “nervous system”, the various auto parts cannot start and work. While it is considered a Tier-2 auto parts supplier, [Company’s name] directly participates in the design process of Tier-1 suppliers for most of its [Flagship product’s name] to be “designed-in” and as a result, enjoys sole supplier rights during the first 2-3 years following a new model launch. In addition, [Company’s name] has changed its sales model in China from a distributor model to direct selling, forging Tier-1 relationship with the major Chinese automakers, including accounting for over 50% of [Flagship product’s name] used in emerging electric vehicle maker BYD (1211 HK). Its top ten customers account for around 44-50% of sales. [Company’s name] has pursued the strategy of a diversified customer base to lower operating risk so that “no one “no one customer can seal the life and death of [Company’s name]”, and the rest of sales are contributed by hundreds of customers. In the ruthless cut-throat automotive industry, the fact that [Company’s name]’s EBITDA margin at 33% is twice that of world-class Bosch India (BOS IN), arguably the best auto parts company listed in Asia, and [Company’s name]’s ROE of 20.5% is also higher than Bosch’s 14.5% speaks volume about [Company’s name]’s wide-moat advantage in securing long-term pricing power and earnings sustainability with the major OEM carmakers by winning their trust to strike long-term partnership. Bosch India trades at an expensive valuation premium of EV/EBITDA 42.9x compared to 12.2x for [Company’s name]. [Company’s name], with its technical superiority in developing low-cost innovative solutions and in generating higher profitability and growth, deserves to command comparable a higher valuation. Short-term downside is protected by a decent cash dividend yield of 4% and supported by a healthy net-cash balance sheet generated from internal free cashflow as opposed to external equity or debt funding. Led by the highly inspiring Mr. C, [Company’s name] has toiled for more than 10 years since it entered China before bearing some of the fruits. [Company name]’s sales has climbed nearly 31% since FY11 while EBITDA growth is stronger at 78% with the impressive improvement in gross margin from 34.2% to 42.1% due to greater sales weight of higher value-add products that include [Flagship product’s name] for electric vehicles (EVs). Now the growth momentum has hit the tipping point for [Company’s name] to accelerate its profitability significantly in its visible long runway to supply the mission-critical automotive electronics part that is dubbed the “nervous system” in cars whose electronic content is rising due to the Green, Connected, Autonomous automotive trends. Net profit and EBITDA could potentially double in the next 5 years by FY2020, pointing towards a doubling in market value. |