August 31, 1837: Emerson’s Superb Speech on the Life of the Mind, the Art of Creative Reading, and the Building Blocks of Genius – Bamboo Innovator Daily: 31 Aug (Mon)

August 31, 2015 Leave a comment

Life

R.E.S.-ilience in Value Creation 《竹经:经商经世离不得立根创新》

August 31, 2015 Leave a comment

Life

August 30, 2015 Leave a comment

Life

Books

August 29, 2015 Leave a comment

Life

August 28, 2015 Leave a comment

Life

August 27, 2015 Leave a comment

Life

Books

August 26, 2015 Leave a comment

Life

August 25, 2015 Leave a comment

Life

Books

August 24, 2015 Leave a comment

Life

August 24, 2015 Leave a comment

| “Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” | ||||||||||||||||||||||||

| BAMBOO LETTER UPDATE | August 24, 2015 | ||||||||||||||||||||||||

Bamboo Innovator Insight (Issue 97)

|

||||||||||||||||||||||||

| Dear Friends,

What to Do When Earnings Torpedo Sink Your Portfolio and When You Are Misunderstood? From Bezos and Jobs to “Asia’s Overlooked Amazon”, A Guide for Value Investors Don’t let an earnings torpedo sink your portfolio! This is the metaphor coined by accounting researchers Douglas Skinner and Richard Sloan in their controversial paper describing their evidence that the market overreacts sharply and suddenly to announced earnings that fell just short of the analysts’ consensus earnings forecast (i.e. a torpedo effect), and that the effect is more pronounced for “growth stocks”. Hence, while “growth stocks” outperform during “boom periods” with relatively low frequency of negative earnings surprises, they underperform on average relative to “value stocks”. Fears of the torpedo effect also explained why managers tend to play the earnings game to meet or beat the threshold numbers. This practical metaphor comes alive for many investors with the recent heightened volatility in the emerging markets reminiscent of the 1997/98 Asian financial crisis. Even Buffett-invested Deere & Co (NYSE: DE) got hit after it announced last Friday on 21 Aug that third quarter earnings tumbled 40% and its net income for the fiscal year through October will be about $1.8bn, less than the $1.9bn that Deere forecast in May and the $1.92bn average of 11 analysts’ estimates, as lower crop prices weakened the farm economy and the energy industry bought less of the company’s construction machinery. Interestingly, its EPS of $1.53 had beaten the $1.44 average estimate. It is also worth noting that since the beginning of its 2012 fiscal year, Deere has beaten the analyst consensus on 12 out of 14 occasions and the last 10 in a row. Yet its shares have actually fallen following 11 of those 14 results. So the bar has been raised from a simple EPS estimate to a composite measure of forward-looking forecasts in revenue, earnings and outlook. This time round, with the lowered full year forecast, Deere was punished – its shares fell the most intraday in six years, plunging 7.9%. What can value investors do to overcome such painful and frightening earnings torpedo?

The answer perhaps lies in what the researchers left unanswered: Why did they miss the forecast? How will, and how do, the managers and entrepreneurs react after they announce bad news? A key word to unlock the practical investment puzzle is “misunderstood”. Is the company misunderstood in the eyes of the majority consensus? For instance, is the company missing its revenue and earnings forecast because it is making long-term investments that incur costs to impact short-term earnings or in new project initiatives that do not contribute meaningfully to the bottom-line yet? Or is the miss due to a restructuring in sales and product mix? Let us consider the cases of Amazon.com, Steve Jobs and “Asia’s Overlooked Amazon” as a general guide for value investors to think deeper about and respond to the frightening earnings torpedo. Amazon.com (NASDAQ: AMZN) has endured and outlasted critics. The online retail giant has also sunk in multiple earnings torpedo incidents, missing Wall Street forecasts as shown in the table below, and went on to outperform in the longer-term.

Misunderstood could be the word that plagued Amazon and Bezos throughout its history. Amazon recently came under fire after a New York Times article Inside Amazon: Wrestling Big Ideas in a Bruising Workplace on 15 Aug 2015 slammed its “thrilling, bruising” workplace environment, describing Amazon as “a soulless, dystopian workplace where no fun is had and no laughter heard” in which people are encouraged to belittle their colleagues, and where leaving work to recover from cancer earns you a demerit. The NYT writers also described Bezo’s penchant for data-driven management with a story that Bezos himself shared in speech to Princeton grads: “Jeff Bezos turned to data-driven management very early. He wanted his grandmother to stop smoking, he recalled in a 2010 graduation speech at Princeton. He didn’t beg or appeal to sentiment. He just did the math, calculating that every puff cost her a few minutes. ‘You’ve taken nine years off your life!’ he told her. She burst into tears.” The NYT ends the story there, drawing a broad conclusion from 10-year-old Bezos’s behavior: “Decades later, he created a technological and retail giant by relying on some of the same impulses: eagerness to tell others how to behave; an instinct for bluntness bordering on confrontation; and an overarching confidence in the power of metrics.” What the NYT writers fail to mention is that Bezos was using the story to illustrate an important and inspiring humane lesson. Bezos expected to be praised for his math in the offending comment “at two minutes per puff, you’ve taken nine years off your life!” When Bezos’s grandmother “burst into tears,” his grandfather stopped the car on the shoulder of the highway and delivered a line that stayed with Bezos 46 years later. “Jeff, one day you’ll understand that it’s harder to be kind than clever,” his grandfather said. Bezos went on to say that students should not be “seduced” by their gift of intelligence: “Cleverness is a gift, kindness is a choice”. Bezos drew contrasts between choosing “a life of ease” and “a life of service,” and he asked students to consider whether they would “wilt under criticism” or “follow [their] convictions”. Critics of Amazon abound early on since it was established in 1994. When Amazon was still relatively small, Bezos build five $60M automated fulfilment centres in 1999 against the advice of experts: “for a company that only had $1bn in sales, spending $300m on fulfilment centers is a very big investment.” In 2000, its estimated warehouse capacity was three to five times more than it needed. In 2001, sales had fallen short of expectations, two of its distribution facilities were closing, and Amazon had to lay off 1,300, or 15%, of its employees. Pundits and critics predict the death of Amazon. A breakthrough came in 2002 when Amazon embarked on a strategy of broad discounting and free shipping (for purchases >$25) rather than spending money on marketing ads as advised by experts, dramatically increasing sales, decreasing the operating leverage and risk associated with Amazon’s fixed costs while more fully utilizing its newly-developed distribution network. Following his convictions led to many people to misunderstand Bezos and also nearly led to the demise of Amazon. Bezos summed up the “willingness to be misunderstood” as the acid test to overcome ongoing volatility and critics: “Our willingness to be misunderstood, our long-term orientation and our willingness to repeatedly fail are the three parts of our culture that make doing this kind of thing possible”. We also shared with various Asian entrepreneurs over the years about the story of Amazon and Bezos, including a forgotten tale about the “humane” side of Bezos. In 2004, Bezos was visiting an Amazon fulfillment center with his leadership team. During the visit, he heard about a safety incident when an associate had seriously damaged his finger on a conveyor belt. When Bezos learned of the incident, he walked to the white-board and began to ask five whys to get at the problem’s root cause: Q1: Why did the associate damage his thumb? A: Because his thumb got caught in the conveyor. Q2: Why did his thumb get caught in the conveyor? A: Because he was chasing his bag, which was on a running conveyor. Q3: Why was his bag on the conveyor and why was he chasing it? A: Because he placed his bag on the conveyor, but it then turned on by surprise. Q4: Why was his bag on the conveyor? A: Because he used the conveyor as a table for his bag. Q5: Why did he use the conveyor as a table for his bag? A: Because there wasn’t any place near his workstation to put his bag or other personal items. Bezos and his team determined that the likely root cause of the associate’s damaged thumb was needing a place to put his bag but not having one around he used the conveyor as a table. To eliminate further safety incidences, the team provided a portable, lightweight table at the appropriate stations and additional safety training to alert associates about the dangers of conveyor belt work. While this innovation was minor, Amazon member Pete Abilla said it was a transforming experience “that I carry with me to this day.” The incident showed that:

Bezos wanted Amazon to be a place where people are committed to their work like a vocation and are willing to embrace risk and strengthen ideas by stress test., with leadership principles like “never settle” and “no task is beneath them.” Even relatively junior employees can make major contributions. The new delivery-by-drone project announced in 2013, for example, was co-invented by a low-level engineer named Daniel Buchmueller. In essence, Amazon has provided a platform for those who are fanatics in wanting to build meaningful things as part of a bigger purpose. Consider another misunderstood case: Steve Jobs and Apple. Like Amazon, Apple had also had its fair share of earnings torpedo over the years and went on to compound over the long-term. However, a qualifier is that we noticed that Apple had missed earnings on 17 Oct 2011 after having beaten forecasts in every quarter since 2004. This was after Steve Jobs passed away on 5 Oct 2011. Since the earnings torpedo and Jobs’ death in Oct 2011, Apple is up around 80%, roughly in line to around 70% for the NASDAQ index. The story below will give us further insights on why people like Steve Jobs are likely to be misunderstood for their actions. On a late-October morning in 2010 in the restaurant of the Four Seasons hotel in San Francisco, Steve Jobs and two of his friends were approached by a waitress who asked what they wanted for breakfast. Jobs said he wanted freshly squeezed orange juice. The waitress returned with a large glass of juice after a few minutes. Jobs took a tiny sip and told her tersely that the drink was not freshly squeezed. He sent the beverage back, demanding another. A few minutes later, the waitress returned with another large glass of juice, this time freshly squeezed. When he took a sip he told her in an aggressive tone that the drink had pulp along the top. He sent that one back, too. Jobs’ friend asked him, “Steve, why are you being such a jerk?” This story, told in a New York Times article “What Steve Jobs Taught Me About Being a Son and a Father” by Nick Bilton, who commented that his initial impression was that Jobs is indeed a callous jerk, but added that Jobs had planted an idea in his head that he could shake off after hearing Jobs’ reply. Jobs replied that if the woman had chosen waitressing as her “Vocation”, “then she should be the best.” The idea that Jobs believe strongly in is that: No matter what you do for a living, should you do the best work possible? Bilton went on to share a touching tale of how his mother had later contracted terminal cancer with only two weeks to live. That was when the writer learnt that “even if a job is just a job, you can still have a profound impact on someone else’s life. You just may not know it “. On her final day, Bilton’s mother was craving for shrimps. But they did not have any in the kitchen and the nearest place to get them was a tiny nondescript Thai restaurant a few miles away. While Bilton stood waiting for his mother’s shrimp, he watched the restaurant staff toiling away and he thought about what Jobs had said about the waitress from a few years earlier: the idea that we should do our best at whatever job we take on. Bilton concluded: “This should be the case, not because someone else expects it. Rather, as I want to teach my son, we should do it because our jobs, no matter how seemingly small, can have a profound effect on someone else’s life; we just don’t often get to see how we’re touching them. Certainly, the men and women who worked at that little Thai restaurant didn’t know that when they went into work that evening, they would have the privilege of cooking someone’s last meal… It was a meal that would end with my mother smiling for the last time before slipping away from consciousness.” We can detect the dedication and intensity and sense of urgency that Bezos and Jobs bring towards integrating every aspect of their values into their work and life – and why they are easily and always misunderstood. A key task of the value investor in an earnings torpedo situation is to differentiate the authentic innovators and leaders, from the pretenders who use complex financial engineering schemes to generate short-term results that would eventually unwind in impairment losses. Thus, the case of Bezos and Jobs highlighted that in order to overcome the earnings torpedo, value investors must assess the element of misunderstanding that creates volatility in results and must ultimately be able to pierce through this misunderstanding with an acid test: Are the entrepreneurs committed to building an idea larger than themselves to serve others? Only if the value investor is able to sense and measure this commitment to a Purpose and assess that the economic moat remains intact, then would the earnings torpedo present an opportunity to buy more. This brings us to the final case of “Asia’s Overlooked Amazon”… <ARTICLE SNIPPED> Read more at the Moat Report Asia: http://www.moatreport.com/updates/ ******** In her thought-provoking book “No One Understands You and What To Do About It”, author Heidi Grant Halvorson explains why we are often misunderstood and how we can fix that. Halvorson emphasized that this is not about making good impression, but about coming across as you intend to: “It’s about the authenticity we all strive for”. Two particular “solutions” caught our attention as relevant for value investors to assess the entrepreneurs building the economic moat to last for the long-term but got hit by a short-term earnings torpedo or some other challenges. One of them is “Demonstrate your strong willpower.” Do they internalize the obstacles and challenges, maintain discipline, exercise self-control and demonstrate willpower in overcoming the problems instead of blaming external environmental factors or people? Another is “Emphasize what you can do with some concrete specific details, not what you have done.” This allows the value investor to assess the long-term orientation of the entrepreneurs by combining the Elon Musk strategy discussed earlier on delving into details to assess consistency and depth of thoughts in order to sieve out the pretenders. We can observe this in the concrete details provided by “Asia’s Overlooked Amazon” in their long-term investments in the new businesses. There is a sense that they want to get things going, to get things done. Another common example: Consider the statement that companies involved in alleged accounting irregularities often make, that their accounts comply with the financial reporting standards and Big Four auditors have issued them unqualified opinions, but not addressing the specific allegations in providing more transparency and disclosures behind the “audited” numbers: “No, you can’t hide behind GAAP. GAAP accounting rules are the ones that we all live by and they are very strict. We had both KPMG and Ernst & Young restate that they are ok with our numbers.” This was what Computer Associates’ Chairman and CEO Sanjay Kumar said before he was later sentenced to 12 years in prison for his role in the $2.2 billion accounting fraud. Such broad proclamations, that hide under “compliance” or “track record” or “reputation” but do not address the specific issues that people wish to know more to understand the long-term orientation and integrity of the entrepreneurs in generating the numbers, are essentially a signal of defensiveness, impression-management and evasiveness. To sum up, with Halvorson’s solutions to better understand the context of messages emitted by people in situations of misunderstanding and how the authentic leaders go about fixing them, earnings torpedo present an opportunity to buy more only if the value investor is able to

Read more at the Moat Report Asia: http://www.moatreport.com/updates/ PS1: We have some updates on “Behind the Scene Conversations on Value Investing in Asia” in the Forum: http://www.moatreport.com/forums/topic/behind-the-scene-conversations-on-value-investing-in-asia/. We had a thought-provoking discussion with our existing Institutional Members about stocks that include Singapore-listed Petra Foods; HK-listed Sa Sa International, Great Wall Motor, Sun Art Retail; Taiwan’s Poya, Shin Zu Shing, King Slide, Eclat, Paiho; Indonesia’s AKR, India’s Mayur Uniquoters, Kitex Garments, Page Industries, Mahindra & Mahindra and its listed affiliates, Swiss-listed DKSH vs Li & Fung and its listed affiliates Global Brands Group and Trinity. We believe that for value investing to be productive, there has to be a candid dialogue with a group of people who genuinely care for one another.. Our recent weekly insight article on Mahindra & Mahindra (NSI: M&M, MV $12.6bn) was read by the capable management team at the entrepreneurial company. The Mahindra leaders passed the article to the Mr. Ananda Mahindra himself, who commented that it was “well-written” and “bridges the gap between the investors and the ground realities of managing a business in Asia”, according to the management team whom we had a teleconference with two weeks ago: PS2: We also like to share with you an article “Scouring Accounting Footnotes to Prevent Tunneling” which we penned for our local newspaper Business Times Singapore that was published last week: https://www.smu.edu.sg/BT_20150819_1.pdf Warm regards, KB The Moat Report Asia A new monthly issue of The Moat Report Asia is now available! Access the in-depth idea presentation: http://www.moatreport.com/members/ This month of August, we highlight a listed Asian company who is the #1 functional beverage drinks company in its country with around 40% domestic market share by value and the leading functional coffee powder brand in terms of volume (#2 by value). The company is one of few Southeast Asian consumer firms who enjoy success outside of their domestic market, with overseas exports to over 60 countries contributing over 60% of total sales. The company is still in the early growth stage of deepening its channels in the overseas markets with functional beverage as the fastest growing category driving the growth of the global $200 billion nutraceuticals industry. Nutraceuticals is expected to play a central role in the frontline of the battle for consumer health with the rise in lifestyle diseases and consumers are increasingly making health-conscious choices from cutting down on carbonated soft drinks to switching to natural, organic diet. Gross margin has expanded from 30.3% in 2012 to 39.5% in 2014 with improving production efficiencies and rising higher-margin export sales. EBITDA and EBIT margins stand at 19.8% and 16.6% to generate ROE of 22.8%. The company’s high-capex era has stabilized and will enter into a bigger free cashflow and net cash position going forward. Interest-bearing debt-to-equity has dropped from 1-1.2x in 2012-13 to zero debt and net cash in 2014, with the latest net cash to book equity position at 21.7% in 1Q15, giving it a stronger position to make bolt-on acquisitions of niche nutraceutical companies, including expanding into the functional food category to strengthen its robust portfolio of functional beverage brands. The company trades at historical EV/EBIT 15.9x and EV/EBITDA 13.3x. |

August 23, 2015 Leave a comment

Life

Books

August 22, 2015 Leave a comment

Life

Books

August 21, 2015 Leave a comment

Life

Books

August 20, 2015 Leave a comment

Life

Books

August 19, 2015 Leave a comment

Life

August 19, 2015 Leave a comment

Life

Books

August 17, 2015 Leave a comment

| “Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | August 17, 2015 |

Bamboo Innovator Insight (Issue 96)

|

| Dear Friends,

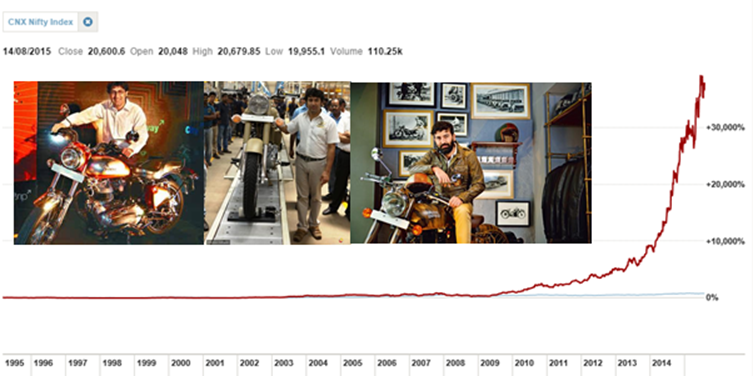

Swadeshi Innovators in Asia (Part 2): Who Is The “Precision Castparts” of Asia? “Brothers and Sisters, I would like to pose a question to my youngsters as to why.. we are forced to import even the smallest of things? My country`s youth can resolve it, they should conduct research, try to find out as to what type of items are imported by India and then each one should resolve that, through may be micro or small industries only, he would manufacture at least one such item so that we need not import the same in future. We should even advance to a situation wherein we are able to export such items. If each one of our millions of youngsters resolves to manufacture at least one such item, India can become a net exporter of goods. I, therefore, urge upon the youth, in particular our small entrepreneurs that they would never compromise.. on.. zero defect. We should manufacture goods in such a way that they carry zero defect, that our exported goods are never returned to us. If we march ahead with the dream of zero defect in the manufacturing sector then, my brothers and sisters, I am confident that we would be able to achieve our goals.” – Indian PM Modi’s at the country’s 69th Independence Day on Aug 15 “My Swadeshi chiefly centres around the handspun khaddar and extends to everything that can and is produced in India.” – M. Gandhi “Swadeshi innovators” was a term inspired by Indian PM Modi and coined by us during the last Independence Day speech in which Modi forged the “Made in India” industrial vision. The word Swadeshi derives from Sanskrit and is a sandhi or conjunction of two Sanskrit words. Swa means “self” or “own” and desh means country. Swadeshi, as a strategy, embodies the principles of self-reliance that stems from a certain deep intangible knowledge, as we have written in our Part 1 article “Swadeshi Innovators in Asia: Fluid, Fast and Nonlinear to Compound Value” on 18 Aug 2014. We commented on the rise of modern facilities in and around Pune in western India – with companies including Germany’s Volkswagen, Indian carmaker Mahindra & Mahindra (MM IN, MV $13.3bn), and autoparts maker Bharat Forge (BHFC IN, MV $2.9bn) helping turn India into a car exporting hub – suggests the industrial success is possible in parts of India. In Gurgaon and Manesar (New Gurgaon), southwest of New Delhi, this industrialization effort is led by Maruti Suzuki (MSIL IN, MV $13.2bn) and wiring harness and auto parts maker Motherson Sumi Systems (MSS IN, MV $5.1bn). Investing in listed emerging markets affiliates of MNCs has proven to be a winning strategy for shrewd long-term institutional investors such as Aberdeen. Unilever, for example, has listed affiliates in India, Indonesia and Pakistan in which it owns stakes of 37%, 85% and 75% respectively. There were 92 such companies across the emerging world, 24 of them in Asia, 46 in Emea and 22 in Latin America. Aberdeen also supported a research paper “Emerging Market Outperformance: Public-traded Affiliates of Multinational Corporations”. Yale’s finance professor Martijn Cremers found the share price performance of listed affiliates was vastly better than that of both emerging and developed markets broadly, as well as their own local markets, over the 13 years from June 1998 to June 2011. An equally weighted index of the 92 listed affiliates returned 2,229%. This compared with total returns of parents, local markets and parents’ markets of 407%, 1,157% and 147% respectively. The pattern of outperformance was consistent across regions too. Affiliates in Latin America, Emea and Asia outperformed their local indices by 41, 134 and 50 percentage points respectively. Adjusted for volatility the affiliates’ performance was even better, as many of them demonstrated defensive qualities during the 2008-09 financial crisis. In recent years since the study, there is increasing backlash against MNCs in emerging markets: from Nestle India’s poisoned Maggi noodles incident; Chinese regulators clamping down on MNCs for overcharging in price-collusion; to Korea forcing MNCs to report their detailed governance structure, business transactions and M&A deals to Korean tax authorities annually from 2017. With the backlash and the “Made In India” drive, we see the increasing localization of content driving Swadeshi Innovators in India and Asia. In Stage 1, Swadeshi Innovators have to forge tie-ups with MNCs to access technology – Maruti has rolled out India’s People’s Car in 1983 after a JV with Japan’s Suzuki Motor (TSE: 7269, MV $20.1bn). With around 40-44% market share supported by a dominant dealer service network, Maruti Suzuki today produces one passenger car every 12 seconds or 1.5 million vehicles a year. Suzuki’s 5.5% royalty stream on all Maruti sales was equivalent to a $500m annual cash dividend and is the recent target of activist investor Dan Loeb. As they grow dominant, they become more powerful than their “masters”, as evident from the split of Hero Motocorp and Honda in Dec 2010 after a 26-year JV partnership that dates back to 1984. However, it could be noted that while Hero Motorcorp survived the crisis and went on to rise around 30% after the split with its MNC partner, it underperformed the Nifty’s 75% climb over the same period. In Stage 2, Swadeshi Innovators attempt the M&A path or in-house R&D strategy to acquire technology for themselves. These include the success of Eicher Motors (NSE: EICHERMOT, MV $8.6bn) whose iconic Royal Enfield premium motorcycles contribute 40% of turnover and 80% of operating profit. Despite a five-fold increase in capacity in the last four years, the waiting period for a Royal Enfield averages between two and four months, as its distinctively-styled bikes fulfil the customer’s key aspiration of owning differentiated products at a reasonable price. Yet, Eicher group wanted to sell or shut down Royal Enfield back in 2000 due to losses and it was second-generation leader Siddhartha Lal who asked his father Vikram Lal for two years to effect a turnaround. We believe the valuation premium from the Aberdeen-style of investing in listed emerging markets affiliates of MNCs will increasing shift towards the Swadeshi Innovators and their listed affiliates. Eicher Motors (NSE: EICHERMOT) – Stock Price Performance vs Nifty index, 1995-2015

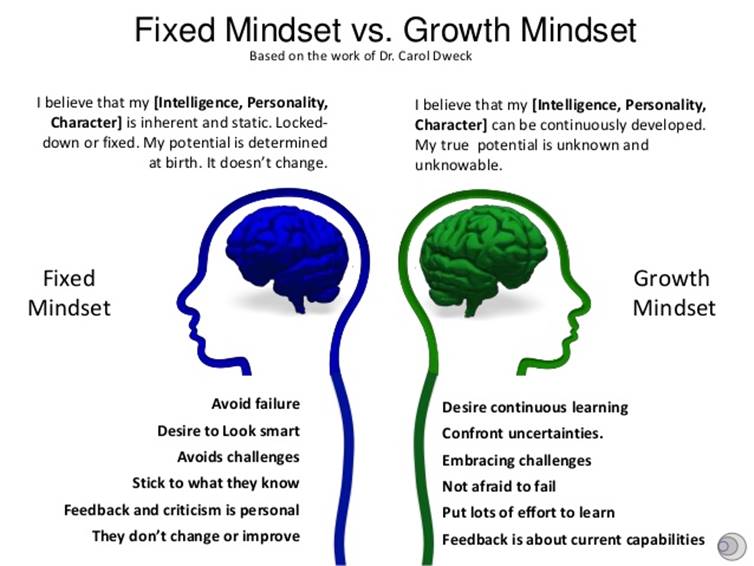

However, analyzing these innovators before they become successful is a huge problem for many value investors. Why? Consider the wisdom of Buffett’s candor who admitted in a recent CNBC interview that he had never heard of the Precision Castparts (PCP), Berkshire Hathaway’s biggest-ever acquisition deal(!), until around 3 years ago when his portfolio manager Todd Combs, who manages $9bn, invested in the company: “Three or so years ago, he added Precision to his portfolio. I had never really heard of the company before that.” Yet, PCP had been founded in 1949 and remains one of the best compounders in American capital history, up over 1,700x in three decades plus, growing from a small metal casting workshop to a global giant in aerospace and oil-and-gas components with a market cap of over $30 bn. In other words, an initial investment of $100,000 compounds to over $170 million, as highlighted in our weekly “Can Asia Produce a Precision Castparts (PCP), a 1,000X Compounder?” on Oct 2013. And Buffett has never heard of PCP until it was up over 1,700-folds. What are the important lessons does Buffett’s candor and the rise of Swadeshi Innovators in Stage 2 hold for value investors? Let’s understand a little more about why Buffett and most value investors tend to miss the PCPs, before we investigate the “PCP of Asia” and why analyzing their rise has proved more difficult unlike the Aberdeen-style of investing in listed emerging market affiliates of MNCs. <ARTICLE SNIPPED> Read more at the Moat Report Asia: http://www.moatreport.com/updates/ ******** Inspired by the work of Carol Dweck in her book “Mindsets: The New Psychology of Success” and based on our decade-plus experience of interacting with Asian entrepreneurs, we see parallels in Swadeshi Innovators as having the “growth mindset” as opposed to the “fixed mindset” of the Sexy Pretenders. A growth mindset is the awareness that painful challenges are inevitable in the journey and approaching them as a process with purposeful engagement to get better in developing one’s ability and character, rather than avoiding challenges and failure to maintain the sense of being smart or skilled. Entrepreneurs with a growth mindset understand the success is not an event-based victory based on a peak point, a punctuated moment in time, like concluding a M&A deal. Success is not merely a commitment to a goal, but to a curved-line, constant pursuit. Value investors will do well to understand the story of how entrepreneurs approach and overcome challenges that come from acquisitions or growing in-house its technological know-how. For instance, when MSS made its breakthrough acquisition in Visiocorp, the world’s largest mirror-making company with its manufacturing facilities largely in Germany, for $21m at the height of the financial crisis, turning around the firm appeared to be an impossible task and the firm was bleeding cash with sales falling off the cliff. It is to be noted that in Germany, if a business runs out of cash, the chief executive is held liable and can even be jailed. At that rather tumultuous stage, Sehgal took a decision that shocked many within the company. He decided to name the then 27-year-old son Vaaman as chief executive. “Of course we would never have allowed him to go to jail but that was the best training I could give him,” says Sehgal. “We saw things going from bad to worse,” recalls Vaaman. “First the lunch stopped, then the tea stopped and then the toilets stopped being cleaned.” For the next four years, Vaaman was put through the fire. He toured Visiocorp’s (since renamed Samvardhana Motherson Reflectec) facilities relentlessly and worked on making processes more efficient. He learnt German. He also made personal calls to his customers – Volkswagen, Audi and Porsche among others- so that orders started flowing in once automobile sales resumed. Within a year, Visiocorp was making a profit and today, it accounts for $1.3nn in sales for MSS. More importantly, with this acquisition, MSS had gained global scale, global customers and global ambition. Overall, between 2002 and 2015, MSS has made 15 acquisitions and compounded market value by over 300X to nearly $7bn. At the heart of what makes the “growth mindset” so winsome, Dweck found, is that it creates a passion for learning rather than a hunger for approval. Its hallmark is the conviction that human qualities like intelligence and creativity, and even relational capacities like love and friendship, can be cultivated through effort and deliberate practice. Not only are people with this mindset not discouraged by failure, but they don’t actually see themselves as failing in those situations — they see themselves as learning. The growth mindset leads people to more deeply engage with the limits of their skills and emotions at a particular time. We thrive, in part, when we have Purpose, when we still have more to do. Value investors will do well to sense that forward thrust, a reason and Purpose to continue making work, in order to distinguish between the Sexy Pretender opportunistically engaging in short-term financial engineering schemes that usually unwind into eventual impairment losses and the authentic Swadeshi Innovator.

Read more at the Moat Report Asia: http://www.moatreport.com/updates/ Warm regards, KB The Moat Report Asia A new monthly issue of The Moat Report Asia is now available! Access the in-depth idea presentation: http://www.moatreport.com/members/ This month of August, we highlight a listed Asian company who is the #1 functional beverage drinks company in its country with around 40% domestic market share by value and the leading functional coffee powder brand in terms of volume (#2 by value). The company is one of few Southeast Asian consumer firms who enjoy success outside of their domestic market, with overseas exports to over 60 countries contributing over 60% of total sales. The company is still in the early growth stage of deepening its channels in the overseas markets with functional beverage as the fastest growing category driving the growth of the global $200 billion nutraceuticals industry. Nutraceuticals is expected to play a central role in the frontline of the battle for consumer health with the rise in lifestyle diseases and consumers are increasingly making health-conscious choices from cutting down on carbonated soft drinks to switching to natural, organic diet. Gross margin has expanded from 30.3% in 2012 to 39.5% in 2014 with improving production efficiencies and rising higher-margin export sales. EBITDA and EBIT margins stand at 19.8% and 16.6% to generate ROE of 22.8%. The company’s high-capex era has stabilized and will enter into a bigger free cashflow and net cash position going forward. Interest-bearing debt-to-equity has dropped from 1-1.2x in 2012-13 to zero debt and net cash in 2014, with the latest net cash to book equity position at 21.7% in 1Q15, giving it a stronger position to make bolt-on acquisitions of niche nutraceutical companies, including expanding into the functional food category to strengthen its robust portfolio of functional beverage brands. The company trades at historical EV/EBIT 15.9x and EV/EBITDA 13.3x. |

August 17, 2015 Leave a comment

Life

August 16, 2015 Leave a comment

Life

August 15, 2015 Leave a comment

Life

August 14, 2015 Leave a comment

Life

August 13, 2015 Leave a comment

Life

Books

August 12, 2015 Leave a comment

Life

August 11, 2015 Leave a comment

Life

Books

August 10, 2015 Leave a comment

| “Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | August 10, 2015 |

Bamboo Innovator Insight (Issue 95)

|

| Dear Friends,

Warren Buffett, “The Value Investing Carpenter” and the Adapting the Greatest Investing Strategies of All in Asia Would you use cheap wood for the back of a cabinet, since nobody is going to see it? A great carpenter won’t. Steve Jobs and Warren Buffett won’t. Steve Jobs shared the story of how he was inspired by his dad who taught the young Jobs that it was important to craft the back of cabinets and fences properly, even though they were hidden. “He loved doing things right. He even cared about the look of the parts you couldn’t see,” Jobs explained, a motto that has guided him to build Apple with a craftsmanship drive and “process” to make “insanely great” creations that customers love to use and that will “put a dent in the universe”. In his inspiring book “The Carpenter: A Story About the Greatest Success Strategies of All”, Jon Gordon explained that a carpenter builds things; a great carpenter creates a work of art like a craftsman. While most people approach their work with the mindset that they just want to get it done, craftsmen are more concerned with who they are becoming and what they are creating rather than how fast they finish it. After all, it’s no use finishing something if it’s not a work of art. Craftsmen would pour their hearts and souls and Love into everything they build, knowing that all that they create is a reflection of themselves. When they create art, they feel energized, and they energize all those who experience their work. And with each creation, they become more of the person they were meant to be. Warren Buffett’s greatest investing strategy of all is having an eye for these “great carpenters”. These great carpenters take the form of outstanding entrepreneurs who put their Love into the work they do. Love isn’t just a feeling. It is a commitment and ongoing action. Choosing to love meant you were choosing to make a commitment that you will love regardless of how you feel and you will put love into action regardless of your circumstances. Like Nebraska Furniture Mart’s Mrs. B, whose work ethics was phenomenal: “I come home to eat and sleep, and that’s about it. I can’t wait until it gets daylight so I can get back to the business.” She was on the floor until retiring at 103, and died the following year in 1998. She was committed in serving her customers with dedication. Because we Love, we Serve. And when we serve others, we fill up their cup with love and our own as well. As Buffett explained, “One question I always ask myself in appraising a business is… [to identify the] business built upon delivering exceptional value to the customer that in turn translates into exceptional economies for its owners”. Buffett elaborated further that everyone should study Mrs. B: “They would learn the essence of business. They would learn that taking care of customers is what it is all about. Taking care of them… She did and working like crazy she was there day after day. She had a passion for it.” Buffett summed up his value investing philosophy: “When we buy businesses, we are looking for people that will not lose an ounce of passion for the business even after their business is sold.” In essence, Buffett goes beyond the numbers to identify wide-moat innovators by also sensing that an entrepreneur takes care of his or her customers in a deep way and keep delivering exceptional value to them. Even if it means pains and sacrifices. Even if it takes a long time, working crazy day-in-day-out. Even if they grow rich. All possible only because they are committed to an idea larger than themselves to serve others. When you love and serve, you care about the work you do and show people you care about them, you stand out in a world where most don’t care. The world will flock to people who care and buy products that were made with care and support businesses that care. We can tell whether the person making the products or services cared enough to make it great. When we care, we build things that others care about. When we care, we are craftsmen and craftswomen who are always looking to get better, work harder, and care more. Who are the businesses that understood the power of caring? Some of these include:

When you don’t care – whether it is using cheap wood for the back of a cabinet, taking shortcuts, or focusing on opportunistic short-term financial engineering schemes or accounting tunneling manipulations that usually unwind into eventual impairment losses – people can tell. Un-caring can be manifested in “smaller” simple ways, such as BreadTalk (BREAD SP, MV $271m), Singapore’s largest 46-outlet bakery chain who was under fire by being recently discovered last week for using Yeo’s pre-packaged soya bean milk, labeling the third-party vendor’s soya bean milk as their own branded bottle of “freshly-prepared” soya milk for a number of years. BreadTalk sold the 350ml bottles for a special promotional price of S$1.80 each (its normal selling price is S$3) while Yeo’s soya bean milk is sold at S$1.50 for a one-litre carton. Usually, when a company engages in financial engineering deals, it could easily forget or be distracted from its original Purpose in Serving and Caring at the day-to-day ground level. Before the recent scandal, Breadtalk had made a joint venture investment to develop Beijing plots in Apr 2013, following up from an investment in various property projects managed by a Singapore retail property trust in Jan 2014, Nov 2011 and Jan 2010. Interestingly, if the sum of capital is allocated to strategic investments in bakery-related wide moat companies since Jan 2010, Breadtalk would have gained handsomely in not only capital gains but more importantly, an opportunity to seek long-term cooperation leveraging off its core competencies. These “could-have” capital allocation include: bakery-café compounder Panera Bread (PNRA) which tripled in value; Japan’s Yamazaki Baking (2212 JP), up over 90%; Taiwan’s bakery equipment specialist Sinmag Equipment (1580 TT), up over 230%; Indonesia’s Nippon Indosari (ROTI IJ), up over 320%; Korea’s Samlip General Food (005610 KS), the listed company supplying to its Paris Baguette bakery chains, up over a staggering 3,800%. Or un-caring can take the form of bigger complex schemes, such as a Chinese healthcare services firm doing a financial engineering job in soliciting a $966m non-binding bid on 6 Aug 2015 from a Chinese departmental store whose book equity is $219m (tangible book equity is a negative $593m!) and is pummeled by recently reported interim losses while carrying over $950m in interest-bearing debt (excluding undisclosed off-balance sheet debt and a sudden suspicious jump in “other current liabilities” from $40m in FY04 to $207.5m in 1Q15) – and the market value of the Chinese healthcare services firm is around $460m before the “bid”. Share price spiked up after the non-binding bid announcement, saving the day for the insiders who have likely pledged their shares and thus escaping margin calls on the pledged shares. Much of the Chinese healthcare services firm’s supposed cash & cash equivalents held in the balance sheet are raised from $243m in external funds; its cash outflow on “investing activities”, including related-party transactions, amount to $130m, corresponding to the increase in “unearned revenue”, raising the reasonable doubt on the possibility of the cash outflow re-routed back to the firm as “cash equivalents” while generating artificial sales. It is to be noted that the sum of external funds raised and the cash outflow in investments approximates the total cash and cash equivalents. The Chinese healthcare services firm also has inconsistent patterns between its non-financial measure and financial measures, an empirical tool to detect firms with high fraud risk. In the course of highlighting our monthly Moat Report Asia ideas over the past two years, we have focused on a two-step process to identify wide-moat compounders in the Asian capital jungles:

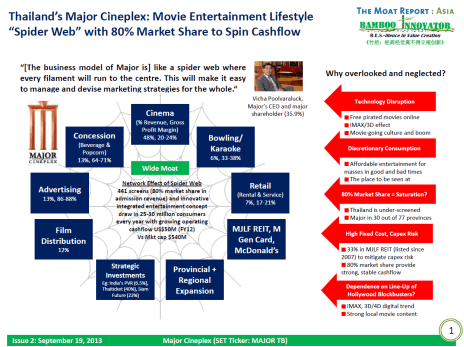

We realize that the wide-moat companies in which we have thought deeper about a Step 3 – the story and validated committed actions of how they Love, Serve, and Care with a Purpose larger than themselves – tend to perform better. Who are the Asian businesses that undertake the committed action to illuminate the power of caring? We highlight some of them below: Consider Major Cineplex (SET: MAJOR) that we highlight in Sep 2013 and is up about 80% while the SET index is flat over the same period; Major was also down >15% along with the SET index in 4Q13. Major is Thailand’s dominant cinema chain operator with a 80% domestic market share, a “spider-web” lifestyle entertainment business model attracting 25-30m Thai consumers to its “destination to be”. Major’s CEO Vicha Poolvaraluck shared how he cares deeply about the consumer experience, using creativity to fight foreign competition which dominated the local cinema industry. Vicha elaborated that he made “all theatres different, more colourful and invested in interior decoration. Thais are people who are eager to see and experience something new and exciting all the time. In the West, many theatres may use the same style of carpet for three or more years without any renovation. But I cannot do that with my cinema here. If people get bored with the atmosphere of the place, they can instead stay at home and watch a DVD. We have to always make everything fresh [design and concept of the cinema] to draw them go out of home.” Vicha demonstrated his love and care to serve his customers in the committed action to take photos of nice places during his travel trips and send them to his marketing and engineering team to see the possibility of adapting the décor, carpet, toilet, unique objects, welcome drinks, and the services in the cinema.

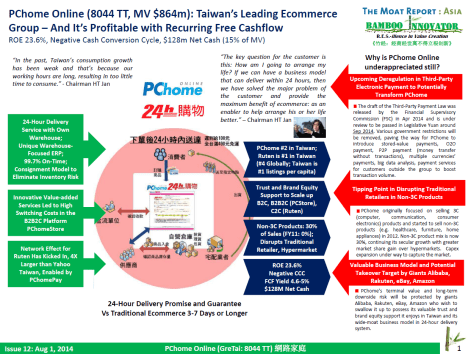

Consider PChome Online (GreTai: 8044 TT) that we highlight in Aug 2014 and is up around 51% while the TWSE index is down 8% over the same period. PChome is the largest ecommerce group in Taiwan and has complete platform coverage in the Amazon-type of B2C ecommerce of selling directly to end consumers (PChome), Rakuten-type of B2B2C platform (PChomeStore) to support the online SME merchants who in turn sell to the end consumers, and the eBay-type of C2C auction site (Ruten) where individuals buy and sell to one another. PChome’s founder and chairman Jan Hung-tse shared how he describes the obstacles to ecommerce transactions as ‘friction’, and how he care deeply to commit to building a business model that can deliver within 24 hours. Jan showed great foresight in understanding the needs of the consumer in forging the Purpose, the Why: “First, the why. We can have an asset-light business model and it’s about managing information flow more efficiently and more complete. A body as light as a swallow. I can have online orders from the customers. Then I will go to the suppliers to purchase the goods to deliver to the customers. However, I am now a customer myself and I am dependent on the efficiency of the suppliers. The goods that I ordered from the suppliers may come one day later, two days, three days, maybe not at all. Once I received the goods, I will deliver them to the customer. Another one day, two days, or three days. The key question for the customer is this: How am I going to arrange my life? If I am flying off to Shanghai the day after, and I want to buy one more memory storage card for my digital camera. Do I spend time to go out to buy or do I make the purchase online? If I know that the purchased goods will come the next day, it will be just in time for my flight to Shanghai and I can utilize my time better. The biggest problem is that there is uncertainty in the delivery time. It can arrive tomorrow, the day after, or even longer. If we can have a business model that can deliver within 24 hours, then we have solved the major problem of the customer and provide the maximum benefit of ecommerce: as an enabler to help arrange his or her life better.” Jan elaborated: “I resolve to take on the Life’s Task to reduce this ‘friction’. I decided to build our own warehouse inventory management and logistics system. Taking on this challenge to sharpen the sword to reduce the friction has taken nearly 10 years. We have reduced the time to delivery from three days to 24 hours.” PChome reap the returns from serving the consumer with love and care: “Through 24-hours delivery, 7 days no-conditions returns policy and various other measures, including the cost of goods returned is borne by PChome and a penalty fee of TWD 100 shopping voucher for late deliveries and free delivery for purchases above TWD 490 ($16.3), we erase the doubts and concerns of consumers. As a result, during the initial launch of the 24h, the average daily transaction value of each customer is around TWD 500 per customer. One year later, it jumped nearly 10-fold to TWD 4,900.”

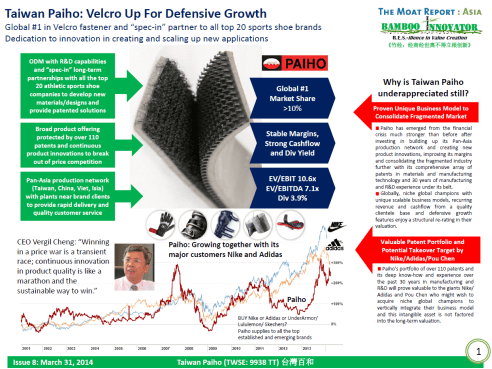

Consider Paiho (TSE: 9938 TT) that we highlight in Mar 2014 and is up 75% while the TWSE index is flat during the same period. Paiho is the world’s largest touch fastener tape maker (1.3m km/yr, >10% market share) with applications in apparel, shoes, diapers, car seats etc. All top 20 global athletic shoe brands, inc Nike, Adidas, Reebok, Sketchers, UnderArmor are customers and Paiho has forged long-term “spec-in” partnerships with them. Paiho’s founder and chairman Vergil Cheng shared the insight how he care about the customer and fostering innovation among his employees: “Paiho is one of the rare few Taiwan and even Asian shoe materials company with proven R&D capabilities and is involved in the design stage with the client before the new product is launched. Our “spec-in” long-term partnerships with all the top 20 athletic sports shoe companies develop new materials/designs and provide better and patented solutions to avoid price competition and maintain stable margin. We send 8,000 pieces of sample products to our clients for them to do their trial tests. Only by doing co-R&D work with the world’s best brands and growing together with them can we provide the best customer service and solution, to master and even lead the industry trend. Our comprehensive product range is also protected by over 110 patents. Some of these patented innovations include our water-resistant tape fastener which can maintain its ‘stickiness’ in the water and is designed for water sports activities. The importance of R&D cannot be emphasized enough; it’s akin to helping the engineers and developers to‘carry books’. At Paiho, all business unit managers and supervisors and above are automatically listed as a R&D personnel and can present their idea proposal.”

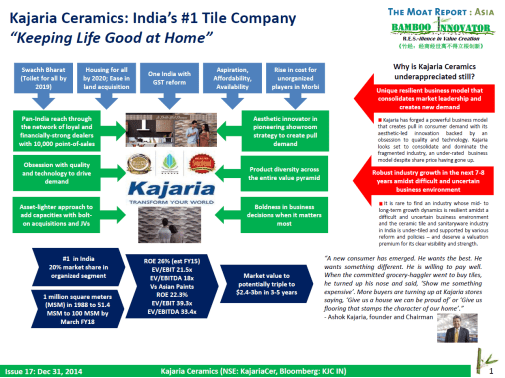

Consider Kajaria Ceramics (NSE: KARARIACER) that we highlight in Dec 2014 and is up around 28% while the Nifty index is up around 3% during the same period. Kajaria is the #1 ceramic tiles company in India with a 20% market share in the organized segment of the tiles industry. The company has been able to successfully create a ‘pull’ for its products and currently enjoys the highest brand equity in the industry in quality, innovation, availability. Kajaria is backed by sound management credibility, comprehensive product range, superior design capability, high brand recall, loyal and widespread dealer network, strong marketing capabilities, business policies, giving it a distinct competitive edge over its peers. It has been conferred the ‘Superbrand’ status for consecutive years since 2004, giving Kajaria a price premium and pricing power advantage. Kajaria’s founder Ashok Kajaria pioneered large-format wall tile segment when everyone is selling cheap small-format tiles as he believed in delivering “Tiles that touch your soul” at a value-for-money price point, rather than compete on price and giving consumers a quality they do not deserve. Kajaria care deeply about delivering Aspiration, Affordability, Availability to the Indian consumer, giving them “a house we can be proud of’ and giving them flooring that stamps the character of our home”. As a result, Kajaria “created a brand that would trigger a consumer pull. Over the last 25 years, the biggest transformation at Kajaria is that what started out as a tile manufacturing company is now an aesthetics-led organization.”

To summarize, we realize that we sometimes commit the mistake in trying to fit what we see and learn about the competitiveness of the firm into the “model” of wide-moat characteristics such as “high switching cost”, “network effect”, “low cost advantage”, “efficient scale”, “intangible assets”. This descriptive approach into fitting observations into the model is categorization through analogy – and its #1 flaw is stocks are categorized into moats AFTER they are obvious. Until we go the distance and extra mile in Step 3, the story and validated committed actions of how they Love, Serve, and Care with a Purpose larger than themselves, we could fall into the dangerous trap of overpaying for the moat even if the valuation metrics appear cheaper with seemingly lower downside risks. The table below sums up the need for value investors to delve deeper into the DNA of a Carpenter-Craftsman to understand the origin and source of the wide-moat before it becomes obvious.

******** Sacrifice is needed for not using cheap wood for the back of the cabinet: The wood was more expensive; the work required more energy, focus, and effort; the process was filled with more sweat and failure; and the years and tears it took to master the craft were greater. Everyone can be a craftsman but not everyone is willing to become one. Too many people want five minutes of fame but they don’t want to spend the thousands of hours it takes to master their craft. You show up every day. You do the work. You see yourself as an artist dedicated to your craft with a desire to get better every day. You put your heart and soul into your work as you strive for excellence. You desire to create perfection, knowing you’ll never truly achieve it but hoping to get closer to it. You try new things. You fail. You improve. You grow. You face countless challenges and tons of rejection that makes you doubt yourself and cause you to want to quit. But you don’t. You keep working hard, stay positive, and preserver though it all with resilience, determination, and a lot of hope and faith. Then you make it! Everyone wants to work with you. And the world says, ‘Where have you been?’ And you say, ‘I’ve been here all along, and hopefully getting better day by day.’ To the world, you are an overnight success. To you, the journey continues. You’re a craftsman who wants to make your next work of art your best work no matter what you have been accomplished in the past. You cannot be a craftsman unless you are putting your love into the work you do. After all, if aren’t building it with love it won’t be worth building. As an artist you must be driven by love. Only then will you create something special, magnificent, and compelling. Only through love will you create a masterpiece. It is also essential to have the right attitude and approach to your life and work. Think of the craftsman beginning a new work. The craftsman is not thinking about failure. The craftsman is only thinking about building his work with love. Because he loves his work so much and creates with love, fear loses its power over the craftsman. And this allows him to do his best work and create with all the love in the universe. In every moment will you choose fear or love? Choose love and: Love the struggles because it makes you appreciate your accomplishments. Love challenges because they make you stronger. Love those who have hurt you because they teach you forgiveness. Love fear because it makes you more courageous. Failure serves as a defining moment, a crossroads on the journey of your life. It gives you a test designed to measure your courage, your perseverance, commitment and dedication. Are you a pretender who gives up after adversity or a contender who keeps getting up after getting knocked down? Failure provides you with a great opportunity to decide how much you really want something. Will you give up? Or will you dig deeper, commit more, work harder, learn and get better? Yes, we will have moments when the last thing you want to do is to love, serve, and care. Loving others is the last thing on our mind when we are stressed. There will be days you don’t want to get out of bed. It is during these times that you need to remember your purpose. The love of what you are building has to be greater than the challenges you face. When you know your why, you will know the how, and you’ll find a way. Your purpose will inspire you to love those you find hard to love, serve when you don’t feel like serving, and care more when you don’t feel very caring. Do everything with gratitude and love. It’s much more powerful this way. And the more you are thankful, the more you will have things to be thankful for. We have, and will, never forget our original motivation and Purpose to do up the Moat Report Asia in highlighting the overlooked, neglected, misunderstood, underappreciated and undervalued wide-moat Bamboo Innovators in the Asian capital jungle to serve value investors and the public, “to explain, exhort, encourage, inform, educate, advise”, in the spirit of the timeless wise words of the late Dr Goh Keng Swee, one of the founders and chief economic architect of modern Singapore. Every year on August 9, Singapore celebrates our National Day commemorating our independence in 1965. This year is a special one as Singapore crosses the mark of 50th year. Singapore had the winning founding team of Lee Kuan Yew as the indomitable political visionary, Goh Keng Swee as the economic and financial architect, and Hon Sui Sen as the builder and administrator par excellence. National Day is a time to remind ourselves to remember how our founders and forefathers Serve and Care in crafting Singapore to be a special Home filled with Love and the right values. Five years ago, we wrote a trilogy series about Berkshire Hathaway and Singapore. We like to share them with you in this Singapore’s National Day special. Happy National Day to all!.. Part 1: The power of vision The success of Berkshire Hathaway and Singapore can be traced to their visionary leaders who work with winning teams Part 2: Lion Infrastructure and value investing Both of them are an ongoing team process that demands sacrifice, hard work and soberness to scale new heights http://www.businesstimes.com.sg/?dlink=/sub/views/story/0,4574,389848,00.html Part 3: Lion Infrastructure is the way to go To reach a US$2 trillion GDP in 2065, Singapore must create and build commercial assets with a special quality The Trilogy in One Document: Read more at the Moat Report Asia: http://www.moatreport.com/updates/ Warm regards, KB The Moat Report Asia A new monthly issue of The Moat Report Asia is now available! Access the in-depth idea presentation: http://www.moatreport.com/members/ This month of August, we highlight a listed Asian company who is the #1 functional beverage drinks company in its country with around 40% domestic market share by value and the leading functional coffee powder brand in terms of volume (#2 by value). The company is one of few Southeast Asian consumer firms who enjoy success outside of their domestic market, with overseas exports to over 60 countries contributing over 60% of total sales. The company is still in the early growth stage of deepening its channels in the overseas markets with functional beverage as the fastest growing category driving the growth of the global $200 billion nutraceuticals industry. Nutraceuticals is expected to play a central role in the frontline of the battle for consumer health with the rise in lifestyle diseases and consumers are increasingly making health-conscious choices from cutting down on carbonated soft drinks to switching to natural, organic diet. Gross margin has expanded from 30.3% in 2012 to 39.5% in 2014 with improving production efficiencies and rising higher-margin export sales. EBITDA and EBIT margins stand at 19.8% and 16.6% to generate ROE of 22.8%. The company’s high-capex era has stabilized and will enter into a bigger free cashflow and net cash position going forward. Interest-bearing debt-to-equity has dropped from 1-1.2x in 2012-13 to zero debt and net cash in 2014, with the latest net cash to book equity position at 21.7% in 1Q15, giving it a stronger position to make bolt-on acquisitions of niche nutraceutical companies, including expanding into the functional food category to strengthen its robust portfolio of functional beverage brands. The company trades at historical EV/EBIT 15.9x and EV/EBITDA 13.3x. |

August 10, 2015 Leave a comment

Life

August 9, 2015 Leave a comment

Life

August 8, 2015 Leave a comment

Life

August 8, 2015 Leave a comment

Life

August 6, 2015 Leave a comment

Life

Books

咬定青山不放松,立根原在破岩中。 千磨万击还坚劲,任尔东西南北风。