Where the Chinese credit is going…

Kate Mackenzie | May 01 10:51 | 3 comments | Share

Part of the CHINA’S CREDIT CONUNDRUM SERIES

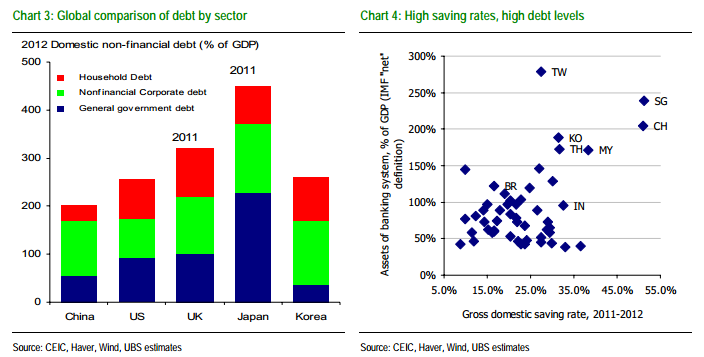

After Chinese first quarter GDP missed expectations, there was some hope that the relatively strong manufacturing PMIs in March would point to a better second quarter. Now that we know China’s April PMIs are definitely not supporting that notion, it is worth revisiting, again, the whole question of the country’s recent surging credit growth. The significance of the debt-to-GDP ratio can be argued over, and it’s impossible to say at what level it might become a big problem. But here are a couple of ideas to consider. First, UBS’ China economist Wang Tao has taken a look at the debt/GDP question. Her estimate is that government debt was about 55 per cent of GDP at the end of 2012, and total debt is about 210 per cent of GDP. (China’s official government debt to GDP ratio is only about 15 per cent, going purely on government bonds, but that ignores many government corporations, local debt, and the asset management companies that took on bad debt in the early 2000s financial crisis.) Anyway, 210 per cent is broadly in line with other credible estimates. Wang argues this absolute level in itself is not cause for dismay. In comparison to developed economies it may seem high, but it’s less dramatic measured against other emerging and Asian economies, which she points out typically have high savings rates which in turn provide some of that credit: There are a couple of other reasons not to worry. The growth might simply be lagging the credit surge, and some credit might have been double-counted: To be fair, we think credit growth has a delayed effect on economic growth, and expect construction an investment to pick up in Q2 and Q3 this year on the back of strong credit growth so far. Also, the TSF may overstate (or double count) the leverage increase in the real economy – corporates that engage in interest arbitrage by borrowing cheaply in the interbank credit market and lend to other corporate and/or local governments have both legs of their transaction included in TSF. While Wang doesn’t think a debt crisis is imminent, she does believe there are certainly reasons to worry. One is the recent rapid increase in the debt-to-GDP ratio. This is a very good point which we mentioned in February and forgot to point out in our ruminations of the past couple of weeks. To recap: Morgan Stanley’s Ruchir Sharma sums up some of these reasons in a WSJ op-ed, citing a BIS paper by Mathias Drehmann and Mikael Juselius which finds that if the private debt-to-GDP ratio increases by 6 per cent or more above its 15-year average, that is a “very strong indication that a crisis may be imminent”.

Wang believes there’s another reason for worry:

However, there is also plenty of evidence to suggest that financial distress is another reason why credit expansion has not worked well. Some local governments and companies do not have sufficient cash flow to pay interest on their existing debt, and have to borrow new debt to help service older debt. This is not hard to imagine for local governments – even if they have invested in sound projects in the last stimulus program, most of the projects do not yet have a cash return. In a downturn where local governments face weak tax revenue, dropping land sales, and more demand for pushing up investment and GDP from higher levels of government, the logical solution would be to incur more debt to keep the ball rolling. Read more of this post