Investors Turn Choosy on Chinese Debt after a deluge of offerings

May 21, 2013 Leave a comment

Updated May 20, 2013, 12:22 p.m. ET

Investors Turn Choosy on Chinese Debt

By FIONA LAW

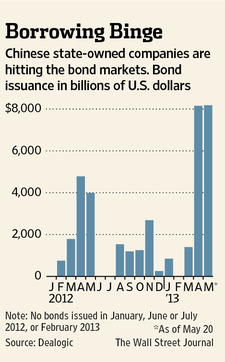

State-owned China International Marine Containers 000039.SZ +0.72% (Group) Co., the world’s largest producer of shipping containers, has postponed a bond sale after global fund managers balked at the interest rate, according to two people with direct knowledge of the matter. The delay may signal that investors are getting picky after a deluge of offerings. Investors had gorged on a record $18.6 billion in dollar-denominated bonds issued this year by Chinese state-owned companies, which typically offer higher returns than investment-grade companies in developed markets. “There’s been a lot of supply, and the beauty of that is, I can choose not to buy some of them,” said Bryan Collins, Hong Kong-based fixed-income portfolio manager at Fidelity Worldwide Investment, referring to the state-owned enterprises’ rising debt. He declined to comment on specific bonds.

Separately, China Cosco Holdings Ltd.601919.SH +0.90% said Monday that its port unit will sell its entire 21.8% stake in China International Marine in a deal valued at US$1.22 billion.

China Cosco’s 43%-owned Cosco Pacific Ltd.1199.HK +3.65% said it would sell the stake to state-controlled parent China Ocean Shipping (Group) Co. and expects to post a pretax gain of US$470.2 million from the sale.

The deal is China Cosco’s second move this year to sell assets back to its parent company, as it struggles to improve profitability after reporting two straight years of net losses. China Cosco is forecast to report a net loss of 1.86 billion yuan ($303 million) for 2013, according to the average estimate of 12 analysts polled by Thomson Reuters. Some forecasts put the net loss at as much as five billion yuan.

Unlike China’s thriving oil industry, whose three biggest companies have issued $9.5 billion in bonds since the start of April, the shipping industry is feeling the weight of a downturn that is curbing demand for container boxes. China International Marine has struggled to boost sales and posted a first-quarter net profit down 42% from a year earlier.

China International Marine had planned to sell up to $300 million in five-year bonds last week and to set the yield at about 3.51%, the two people said. One portfolio manager at a Chinese asset-management firm said that was too low, given how the shipping industry is struggling.

Another person involved in the deal cited technical hiccups in the sales process that led to the delay.

Another concern is the rising debt loads of Chinese state-owned companies. With bank lending relatively tight and interest rates at record lows, they had been rushing to issue debt. This month, Morgan Stanley, MS +0.52% saying their leverage has reached all-time highs, recommended investors scale back their holdings to neutral from overweight.

“The deterioration in fundamentals and the potential supply overhang create a challenging mix,” said Viktor Hjort, Hong Kong-based Asia head of fixed-income research at Morgan Stanley.

The U.S. broker said state-owned companies’ debt tops that of other frequent borrowers like property developers and privately owned industrial companies that usually sell bonds with lower credit ratings or even without ratings at all.

Manulife Asset Management fixed-income manager Ronald Chan said he is also choosy about bonds issued by Chinese state-run companies.

“In the short term, companies in the sectors of power generation will have troubles of overcapacity, although these problems will be ultimately absorbed in the long run,” said Mr. Chan. “One shouldn’t blindly buy into [state-owned enterprises] purely because they are owned by the state and take a government bailout as granted.”