Cash levels in Brokerage accounts approach lowest levels in history! This is America, Now: The Dow Hits a Record High With Household Income at a Decade Low

March 7, 2013 Leave a comment

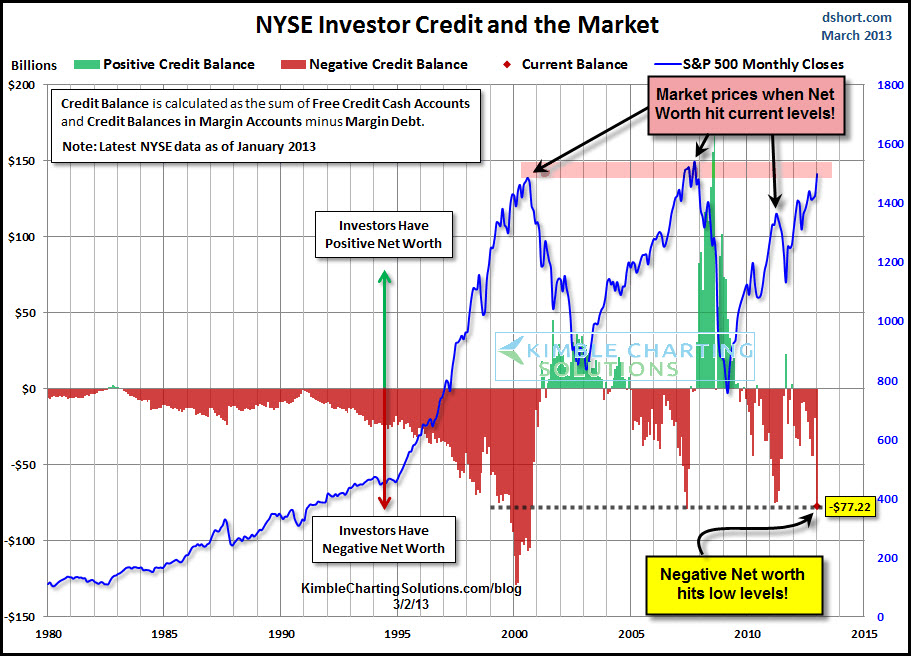

Cash levels in Brokerage accounts approach lowest levels in history!

Posted by Chris Kimble on 03/02/2013 at 7:01 am; This entry is filed under Negative Net worth, S&P 500.

The awesome chart below was created by Doug Short, reflecting that a “ton of cash has disappeared in investors pockets this past month!”

Negative Net Worth = “Free Credit Cash accounts (cash available to spend/invest quickly) minus Margin Debt.” The chart Doug put together reflects a rapid decline in available cash/net worth this past month.

As you can see very few times has “Negative Net Worth” reached the current level over the past 13 years and each time it did, the S&P 500 was closer to a high than a low.

Will it be different this time?

This is America, Now: The Dow Hits a Record High With Household Income at a Decade Low

By Matt Phillips

Stocks surpassed the nominal record set in 2007, while the last recorded real median US household income was 8% lower than its 2007 peak.

Since the bleakest hours of early 2009, the stock market has clawed, scampered and inched higher — with some notable slips. Now that venerable equity market metric — the Dow Jones Industrial Average — has summited 14,164.53, its all-time highest close, in nominal terms, and last seen way back on Oct. 9, 2007.

Terrific! A rising stock market helps Americans rebuild the wealth destroyed by a banking crisis, market meltdown and recession that clobbered their retirement accounts and gutted home values. Ascending stocks also bode well for consumer spending, as there is the well-documented “wealth effect” that helps people feel better about opening their wallets. (Of course, no-one knows whether stocks are setting up base camp for a fresh ascent, or are going to reach a ledge and then jump off the cliff. Also, it’s worth noting that the S&P 500 stock index, a broader gauge of US equities, still has a little ways to go before matching its all-time high close of 1565.15, also set on Oct. 9, 2007.)

Even so, let’s just put the snark on hold for a second and appreciate the view from the peak. (This is a snapshot from not long after the open.)

OK, but here’s the thing. The stock market alone hasn’t repaired the damage done to American household finances in recent years. In many ways Americans are still sucking wind after the gut punch they suffered in 2008. Here’s a look.

HOUSEHOLD INCOMES ARE LOW

These haven’t gone anywhere but down since the recession hit. Real median US household income — that’s “real,” as in “adjusted for inflation” — was $50,054 in 2011, the most recent data available from the US Census Bureau. That’s 8% lower than the 2007 peak of $54,489.

… AND AMERICANS AREN’T OPTIMISTIC THAT THEY’LL GROW

Yes, it’s true that those 2011 data are pretty old. But if consumer expectations are any reflection on income levels, it doesn’t look like the pay has gotten anywhere back to normal pre-crisis levels.

HOUSING PRICES ARE LOW TOO

House prices have been perking up lately. But they’re still about 25% below their 2007 peak, when the median price for an existing home in the US hit $230,300.

AND LABOR’S SHARE OF THE ECONOMY IS AT A 50-YEAR LOW

And while the US economy has gotten back on track, workers’ pay has been a progressively shrinking piece of total GDP since the recession hit. That’s what this chart shows. What’s more, what now feels like the peak of 2007 was actually rather a low hillock, if you look back over the previous few decades.

ON THE OTHER HAND … HOUSEHOLD WEALTH IS RISING

Now, things aren’t completely terrible. The rebound in stocks has helped American households repair their balance sheets (non-profit organizations are included in these numbers) since they were at their lowest during the worst of the recession in the first quarter of 2009. At that point, some $16 trillion in American household wealth had been vaporized. Continued increases in housing prices will help Americans improve their finances.

AND DEBT HAS FALLEN

And there are some areas where Americans are better off than they were before the crisis. For example, their debt payments as a share of disposable income have come way down from unsustainable peaks. (We went a bit farther back with this chart, to give you some perspective.) It’s important to note that this hasn’t been a painless process either. A lot of the reduction comes from traumatic and damaging mortgage defaults. But some of it is also folks taking advantage of the Federal Reserve’s low interest rate policy to refinance existing debt loads.

At any rate, we just thought it was worth pointing out that while the stock market may be back on top, the American people still have a long climb ahead of them.